From just-in-time to smart payments: A case for innovations in Centrally Sponsored Schemes in India

by Anant Jayant Natu and Mitul Thapliyal

by Anant Jayant Natu and Mitul Thapliyal May 14, 2024

May 14, 2024 6 min

6 min

This blog highlights the journey, challenges, and innovations in Centrally Sponsored Schemes (CSS) funding. It focuses mainly on the SNA-SPARSH model and its implications for efficient fund release and payment processing.

Context

The efficacy of transfers from higher to the lower tiers of any government depends on the underlying fund disbursement system. Sample this—the Government of India, as per the budget estimates of 2024-25, plans to transfer funds worth USD 266 billion or ~7% of India’s GDP, to states. This includes devolution of states’ share, grants or loans, and releases under Centrally Sponsored Schemes (CSS). The level of sophistication of these systems have a huge bearing on the nation’s ability to spend and spend well.

On 13th July 2023, the Department of Expenditure (DoE) issued a memorandum to implement the SNA-SPARSH mechanism to ensure the “just-in-time” (JIT) release of funds allocated to the CSS through the RBI’s e-Kuber platform. It builds upon the significant gains of the Scheme Nodal Agency (SNA) system’s implementation in July 2021. This blog post highlights the journey, challenges, and innovations in CSS funding. It focuses mainly on the SNA-SPARSH model and its implications for efficient fund release and payment processing.

SNA-SPARSH’s implementation in India represents a significant milestone in the government payments ecosystem, where the holy grail is to achieve JIT payments. As the name suggests, JIT payments would eliminate the gap between the actual physical event, that is, the work for which the payment is due, and the fiscal event. In this context, the fiscal event is the outward movement of money from the consolidated funds to the end beneficiary—a citizen, a business, or other government bodies.

An implicit assumption in the government fund flow is that money will be pushed from one level to another, but SNA SPARSH inverts this assumption. It allows an agency that makes expenditures to pull funds up to the sanctioned limit when needed. With this, SNA SPARSH pushes the envelope toward smart payments, not just JIT. Operationally, the smart payment system will have two core attributes:

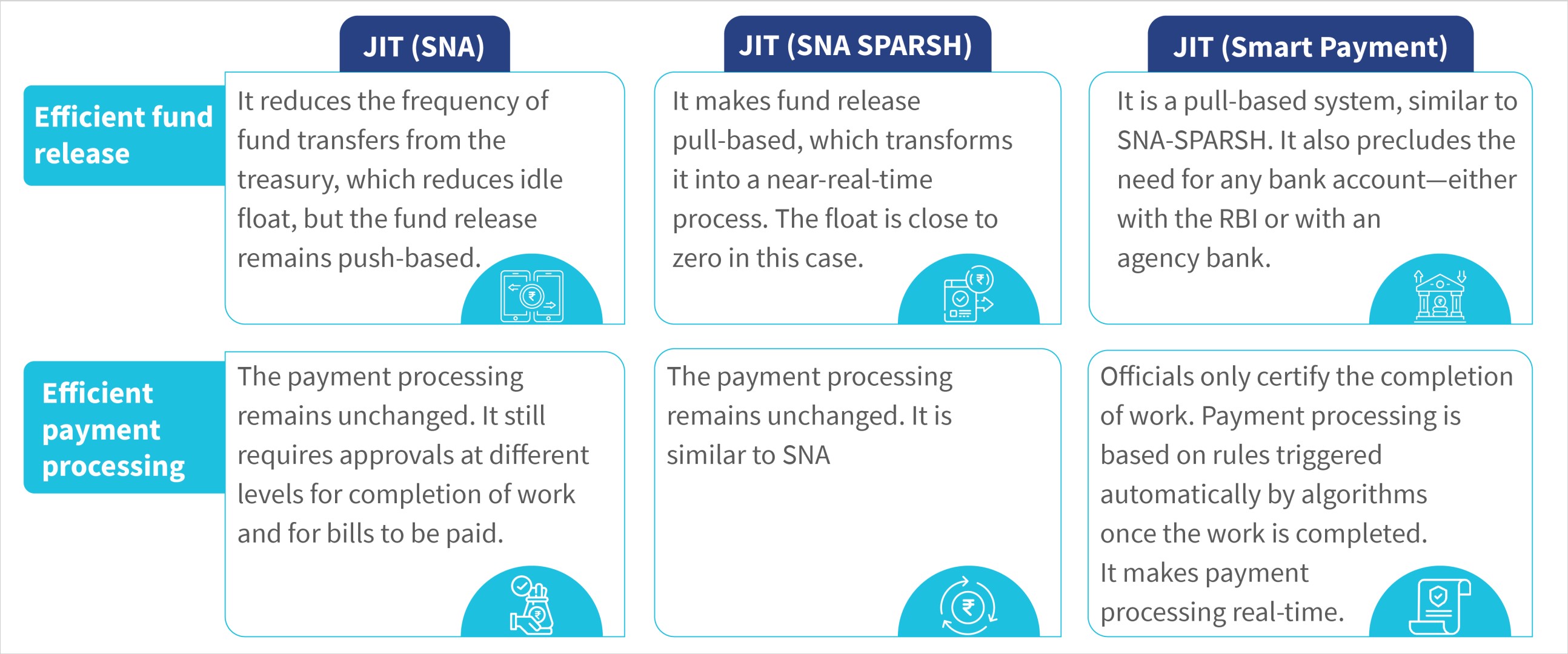

- Efficient fund release: “pulling” funds from the treasury and passing them on directly to the beneficiary’s bank account;

- Efficient payment processing: pulling funds in “real-time,” that is, just when payment for the work is due, based on rules triggered through algorithms.

The table below compares the three evolving versions of JIT on these two attributes.

At the root of this ambition for JIT payments is to enhance the state’s capacity to make expenditures effective and efficient. While the budgetary allocations to social sectors by the governments have slowly increased, available evidence suggests budgets remain unspent. Even with spent budgets, the achievement of outcomes remains low.

CSS accounts for a substantial portion of the central government’s budget, as per the interim budget for FY’25, at INR 5.02 lakh crores (~USD 60 billion), CSSs’ share is about 51% of the total transfers committed by the central government to the states. Thus, the deployment of JIT for CSS can potentially bring significant gains to optimize fund utilization and improve outcomes in the public sector.

A brief history of (just in) time

Over any given year, the CSS would be funded via a cascading fund transfer mechanism. Since the money moved from one agency to another, it led to funds in government bank accounts that sat idle for months or years before they needed to be spent.

The SNA was introduced to consolidate banking arrangements, reduce float, and enhance transparency in fund utilization. It has successfully integrated treasury systems across states and union territories, significantly reduced the number of government accounts, and provided real-time insights into fund releases and expenditures. It tackled challenges, such as unspent balances, cash shortages in some implementing agencies, and inefficient fund release strategies.

The quarterly release of funds and contingent additional releases based on utilization have helped reduce float and prevent the accumulation of unspent balances. India’s Finance Minister highlighted estimated annual savings of USD 1.2 billion from the SNA reforms. The SNA model successfully consolidated funds, improved transparency, and addressed various challenges in the fund release process.

SPARSH—the “pull” to complete the fund release

Under the SNA, the funds are still being “pushed,” albeit with fewer intermediate halts, in shorter bursts, and with a good view of where they are at any given time. The gap between the fiscal and physical events has also been reduced but not eliminated.

However, SPARSH marks a transition from a credit push (a-priori release of funds to various implementing agencies) to a debit pull-based fund transfer system in which a debit to the central pool is triggered only when implementing agencies issue payment instructions on the system. By design, SNA-SPARSH can “pull” funds in real time to the end beneficiary’s account, which takes it closer to a smart payment system. These design features are:

- Integrated framework of PFMS, the state’s treasury or financial management system and the RBI’s e-Kuber platform that enables seamless flow of information across three systems;

- Ability to onboard CSS, SNA, and implementing agencies on the platform—the last two via IFMS;

- Creation of CSS-wise sanction orders for each state at the beginning of a financial year.

Under SPARSH, the eventual release of funds into the beneficiary’s bank account is triggered once the SNA or implementing agency generates the payment files. However, clarity is absent in the time gap between the generation of payment files and the physical event—the moment the work or the payment milestone is achieved in the field. When we revisit the holy grail of just-in-time payments, we find pulling of funds is not in “real time.” This does not qualify it as a just-in-time system since challenges in payment processing persist at the program implementation level.

Cometh the hour, cometh the smart payments

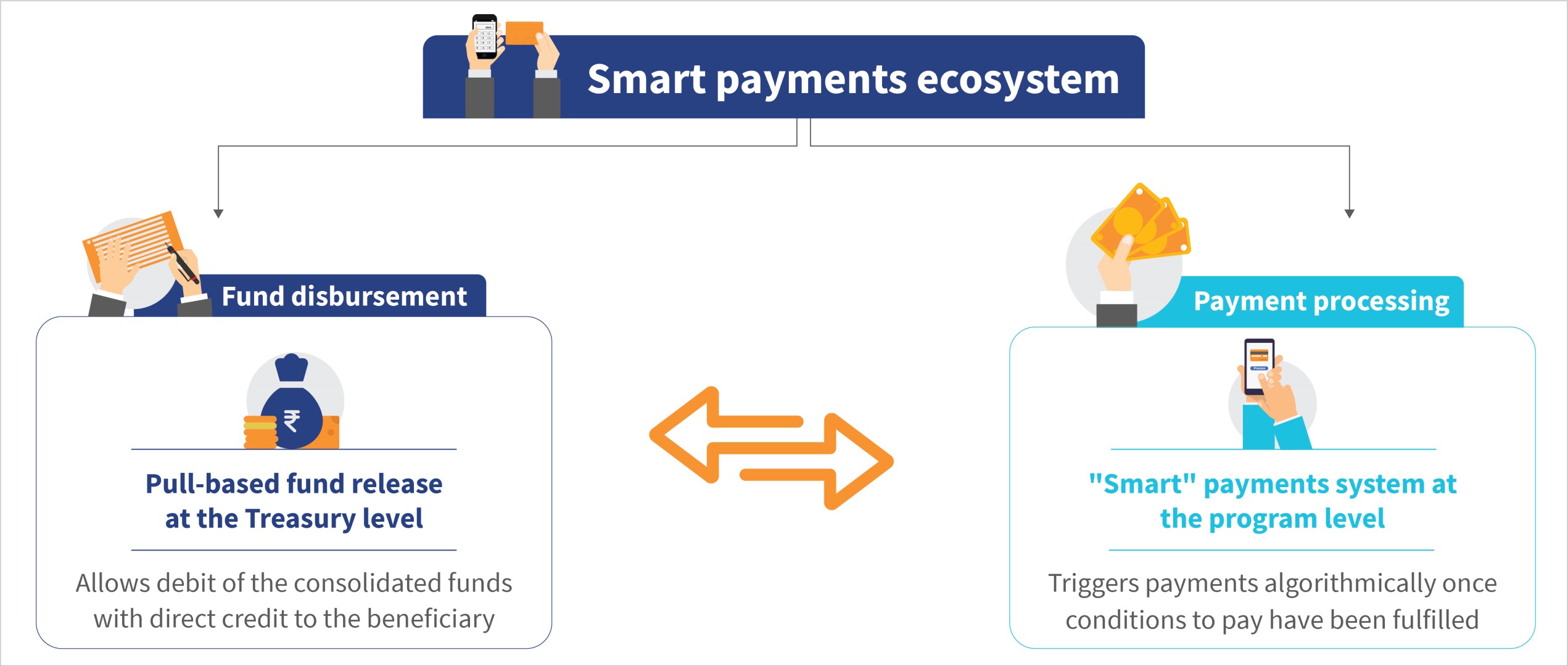

What is needed in this context is a payments processing system that can process payments, that is, generate payment orders automatically upon fulfillment of payment conditions for payees, such as vendors and citizens. Further, it should “talk” to the IFMS system to permit “straight-through processing” of invoices without manual intervention. In other words, we recommend a system that generates the payment files that SNA or implementing agencies can feed into the state IFMS.

When integrated with a pull-based fund transfer system like SPARSH, such a “smart” payments system creates a “smart payments ecosystem” that meets both the conditions of pull-based fund disbursement and the real-time processing of payments. The figure below shows this in detail. SPARSH’s pull-based fund transfer functionalities can be further improved by using a virtual treasury single account (VTSA), which would also eliminate the need to park funds it in any bank account—either with the RBI or an agency bank.

One such smart payments ecosystem is currently being implemented in Odisha. The Government of Odisha launched the MUKTA (MUkhyamantri Karma Tatpar Abhiyan) program to tackle job vulnerability that resulted from the COVID-19 pandemic. MUKTA encountered challenges, such as delays in claim settlement of wage-seekers and SHGs, idle parking of project funds, and ineffective project management.

MSC designed the “smart payments ecosystem” based on our work with the state’s Finance Department since early 2020. We designed a VTSA-based JIT funding system and a smart payments system, “MUKTASoft,” for the Housing & Urban Development Department.

The solution has enabled the transition from a “push-based” to a “pull-based” fund transfer system for beneficiaries, including wage-seekers, SHGs, and material vendors. Under it, the implementing agencies (urban local bodies in the case of MUKTA), pull funds from the state’s consolidated fund directly into the end beneficiary’s bank account in real time when a payment milestone is completed. The solution also incorporates autonomous rule-based processing of payments, which significantly streamlines the process and reduces the burden on officials.

The solution is being piloted in 23 of Odisha’s 149 Urban Local Bodies, and early results are encouraging. It has eliminated the float and reduced payment delays by 57% to the beneficiaries—wage seekers and SHGs. The smart payments system can potentially save the Exchequer as much as USD 50 million for a state like Odisha.

The way ahead

The journey toward an effective and efficient government payments ecosystem in India has seen significant progress with the SNA-SPARSH model. While challenges persist, ongoing experiments and successful pilots demonstrate the potential for transformative changes in how government funds are released and payments are processed. The Department of Expenditure can plan one more reform on SNA-SPARSH to make payment processing based on rules triggered automatically through algorithms upon completion of work certified by the executing agency. It would make payment processing real-time. The vision of JIT payments may soon become a reality to pave the way for improved governance and better outcomes.

Written by

Anant Jayant Natu

Partner

Leave comments