Credit Reference Bureau (CRB) integration in SACCO lending: Lessons from Uganda

by Lois Eva Adongo

by Lois Eva Adongo Jun 29, 2026

Jun 29, 2026 6 min

6 min

This blog examines how Uganda’s increased use of Credit Reference Bureau (CRB) data reshapes lending. It explains why effective integration, stronger governance, and better credit decision-making matter more than access to borrower information alone.

Uganda enters a new phase of formalization of its credit market. Recent data from the Bank of Uganda shows that the number of borrowers captured in the Credit Reference Bureau (CRB) systems increased from 2.9 million to 4.1 million between 2024 and 2025. During the same period, the credit inquiries rose by 28.4%, from 653,400 to 838,700. These trends reflect the growing use of credit data and risk-based lending across banks, savings and credit cooperative organizations (SACCOs), microfinance institutions (MFIs), and digital lenders.

At face value, this is a success story. Greater access to credit information should support better lending decisions and stronger repayment performance. However, emerging evidence suggests a more nuanced reality. While CRB use is associated with better performance, it does not guarantee stronger repayment outcomes.

It is vital to examine how lenders use CRBs in loan screening and how that shapes borrower behavior over time to understand the outcomes.

As the monitoring, evaluation, and learning (MEL) partner, MSC (MicroSave) Consulting examined this issue through a risk-based pricing pilot implemented under the wider MasterCard Foundation’s Micro and Small Enterprise Recovery Facility (MSERF). The Financial Sector Deepening (FSD) Uganda implemented the facility, while one selected SACCO participated in the pilot. MSC complemented these insights with borrower- and portfolio-level data from the gnuGrid CRB platform.

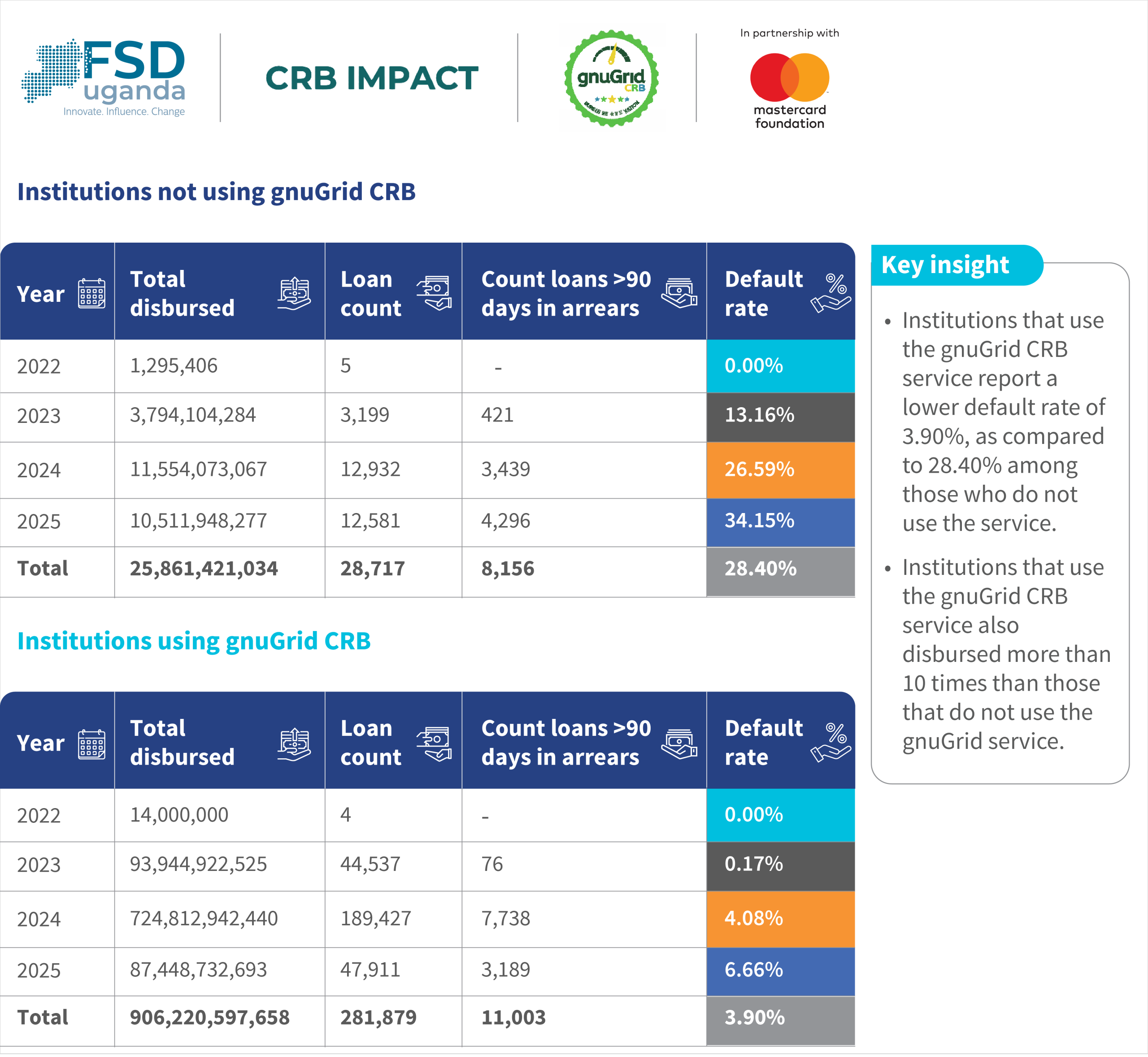

Data from Uganda’s credit market indicates higher performance among institutions that use CRB systems. Evidence from portfolios supported under the MSERF reinforces these findings. Institutions that use CRB systems report significantly lower default rates of around 3.9% compared to 28.4% among non-users.

Figure 1. Source: gnuGrid CRB

However, the relationship between CRB use and portfolio performance is more complex than it first appears. Between 2022 and 2025, MSERF disbursed UGX 99.34 billion (~USD 26.7 million) to 22 participating financial institutions. The facility reached more than 334,000 borrowers and generated a loan volume of UGX 381.24 billion (~USD 102.5 million). Despite this scale and widespread CRB access, portfolio performance remains uneven. Default rates among CRB users have increased over time, and outcomes vary significantly across institutions, even among those using the same CRB systems. The difference is not access to data, but how institutions use it.

The primary role of CRB data is to improve borrower selection. CRBs enable more informed credit decisions by providing visibility into repayment history, outstanding obligations, and exposure levels.

Figure 2. How loan officers evaluate credit reports

However, in many institutions, CRB reports remain a procedural step. Staff pulls and reviews the reports, but they do not incorporate them into structured decision frameworks. Lending decisions continue to rely on personal judgment or informal criteria.

By contrast, high-performing institutions translate CRB signals into clear decision rules, such as score thresholds, rejection criteria, and risk-based loan structuring. These rules lead to more consistent borrower selection and better portfolio outcomes.

Evidence from the MSERF risk-based pricing (RBP) pilot illustrates how this transition plays out in practice. Analysis of matched loan portfolio data from the gnuGrid platform shows that, over time, structured SACCO scoring increasingly influenced pre-disbursement decisions, particularly between May and December 2025.

During this period, clearer differentiation appeared across risk bands. The CCC and DDD received the largest average loan sizes, approximately UGX 9.26 million (~USD 2,452.97) and UGX 11.45 million (~USD 3,033), respectively. Despite this higher exposure, these segments recorded the lowest levels of current delinquency by value. In contrast, weaker segments underperformed despite lower exposure. The EEE showed weaker repayment outcomes, and III exhibited the highest PAR30, PAR60, and PAR90 levels.

These patterns suggest that the scoring model effectively ranks borrower risk, and that value is realized when scores are actively used in pre-disbursement decisioning. When this occurs, scoring results in improved risk differentiation and more efficient credit allocation.

However, the effectiveness of such systems depends on use and on how scoring models are designed. Emerging evidence highlights several constraints that affect accuracy and fairness.

First, data source gaps can introduce structural bias. For example, when Mobile Network Operator (MNO) data is used only partially, borrowers on one network may receive an implicit advantage, while others are penalized despite similar behavior. In such cases, scores reflect data availability rather than true risk.

Second, static representations of risk, such as lifetime maximum arrears, can misrepresent borrower behavior. Borrowers who experienced temporary shocks, such as during COVID-19, may continue to be penalized even as their repayments improve. This weakens incentives for recovery and misaligns with the goals of programs, such as the MSERF, which aim to support resilience.

Third, the weighting of risk variables can unintentionally reinforce exclusion. For example, reliance on collateral as a primary risk determinant may disadvantage women, whose repayment performance is often strong, but asset ownership is limited. While SACCOs often mitigate this through guarantorship, these mechanisms are not always reflected in scoring models, creating a disconnect between actual risk mitigation and model outputs. These issues highlight that the value of CRB data is shaped by institutional use, model integrity, and contextual relevance.

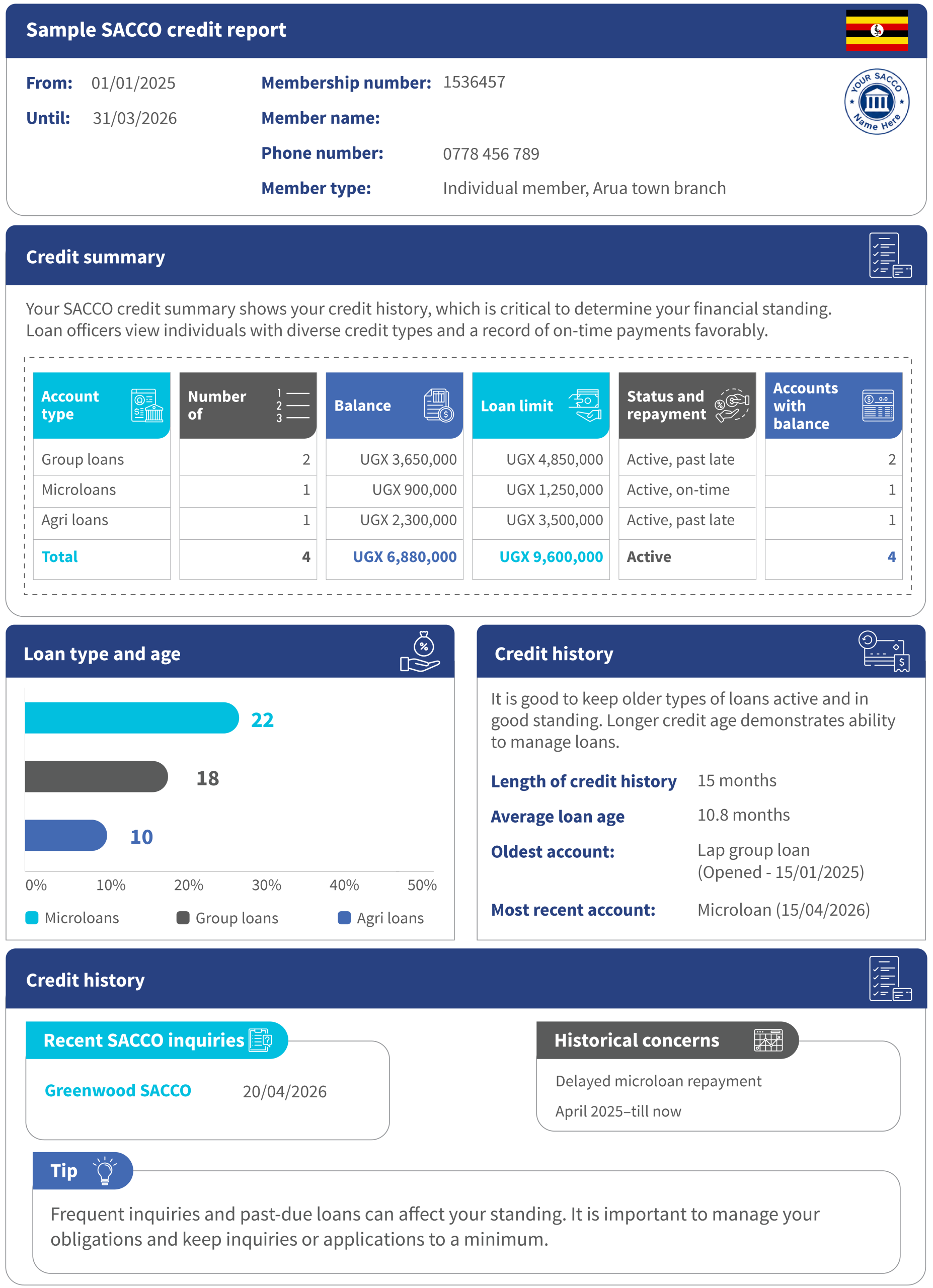

Figure 3: Sample SACCO credit report

The gap between CRB access and effective use is most visible among SACCOs. In practice, this gap lies not in data availability but in how CRB data is used within the lending process.

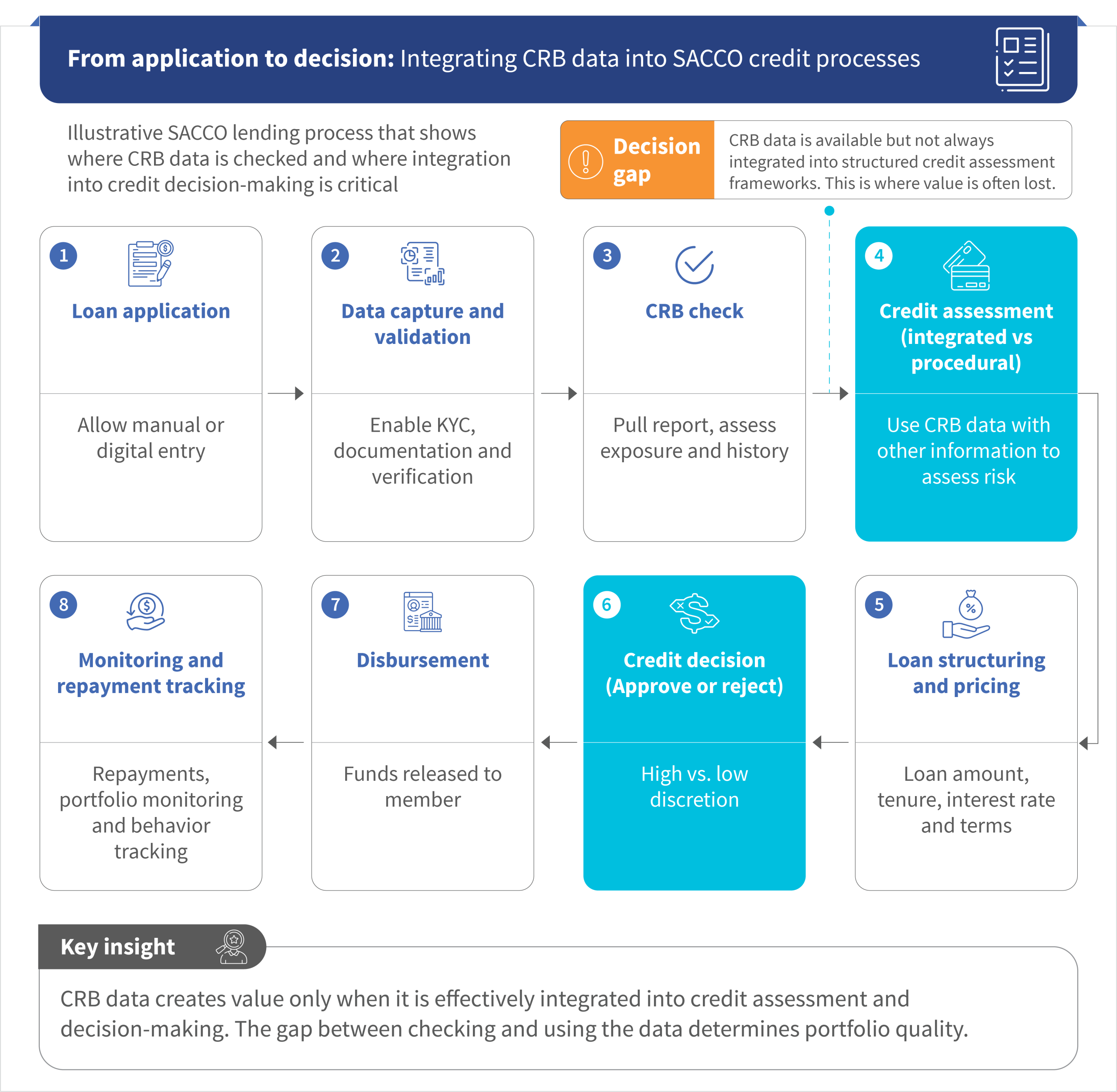

Figure 4: A typical SACCO lending process flow with CRB data

Despite their central role in financial inclusion, many SACCOs lack the systems and capacity needed to translate CRB data into consistent lending decisions. A primary constraint is limited digitization. Many SACCOs rely on manual processes and fragmented systems, which make it difficult to integrate CRB data into workflows or generate consistent assessments.

Governance and capacity challenges further weaken credit decision quality. Weak governance leads to inconsistent application of credit policies, while high override rates undermine discipline. Limited staff capacity to interpret CRB data reduces its effective use.

Data ecosystem gaps also persist. CRB data primarily captures formal credit histories, but many SACCO clients operate informally with limited documentation. Without complementary data, such as cash flow or behavioral indicators, risk assessment remains incomplete.

SACCOs also face a persistent tension between inclusion and risk management. Without strong systems and segmentation frameworks, this often results in either a rise in defaults or overly conservative lending.

In addition to these operational constraints, SACCOs face emerging challenges related to scoring model design. These models rely on incomplete data sources, static risk measures, and heavily weighted collateral variables; their outputs may not reflect borrower realities. This is particularly important in SACCO contexts, where informal income, guarantor-based lending, and recovery trajectories shape repayment behavior. Without continuous calibration, scoring models risk reinforcing bias instead of improving decision quality. CRB systems influence lender decisions and borrower behavior.

When repayment histories are recorded and shared, borrowers have stronger incentives to maintain discipline. Timely repayment becomes valuable, as it builds a credit history and improves future access to credit. This is reflected in stronger performance among institutions that actively use CRB data.

However, this effect depends on system credibility and visibility. Many SACCO borrowers remain partially outside the formal credit systems, which reduces the immediate consequences of default. As a result, incentives to maintain strong repayment behavior are weaker.

Rising default rates among CRB users, as depicted in Figure 1, reinforce this point. CRB data improves initial screening but does not guarantee sustained repayment performance as lending expands into new or higher-risk segments. Stronger outcomes occur where CRB data is embedded within broader systems that combine multiple data sources, continuously monitor borrower performance, and adapt lending decisions accordingly.

This is particularly important for underserved segments, such as youth borrowers, whose thin credit histories require complementary indicators to support both inclusion and repayment.

Uganda’s credit ecosystem is at an inflection point. Access to borrower data has expanded, but the next phase depends on how that data is used. The key shift is from data access to decision intelligence. This requires embedding CRB data into credit policies and decision frameworks, the combination of CRB data with internal and behavioral data, the strengthening of governance, the reduction of discretionary overrides, and investment in digitization to enable consistent, scalable decision-making. For funders, this means moving beyond capital toward capability-building. For financial institutions, it requires rethinking how credit decisions are structured and executed.

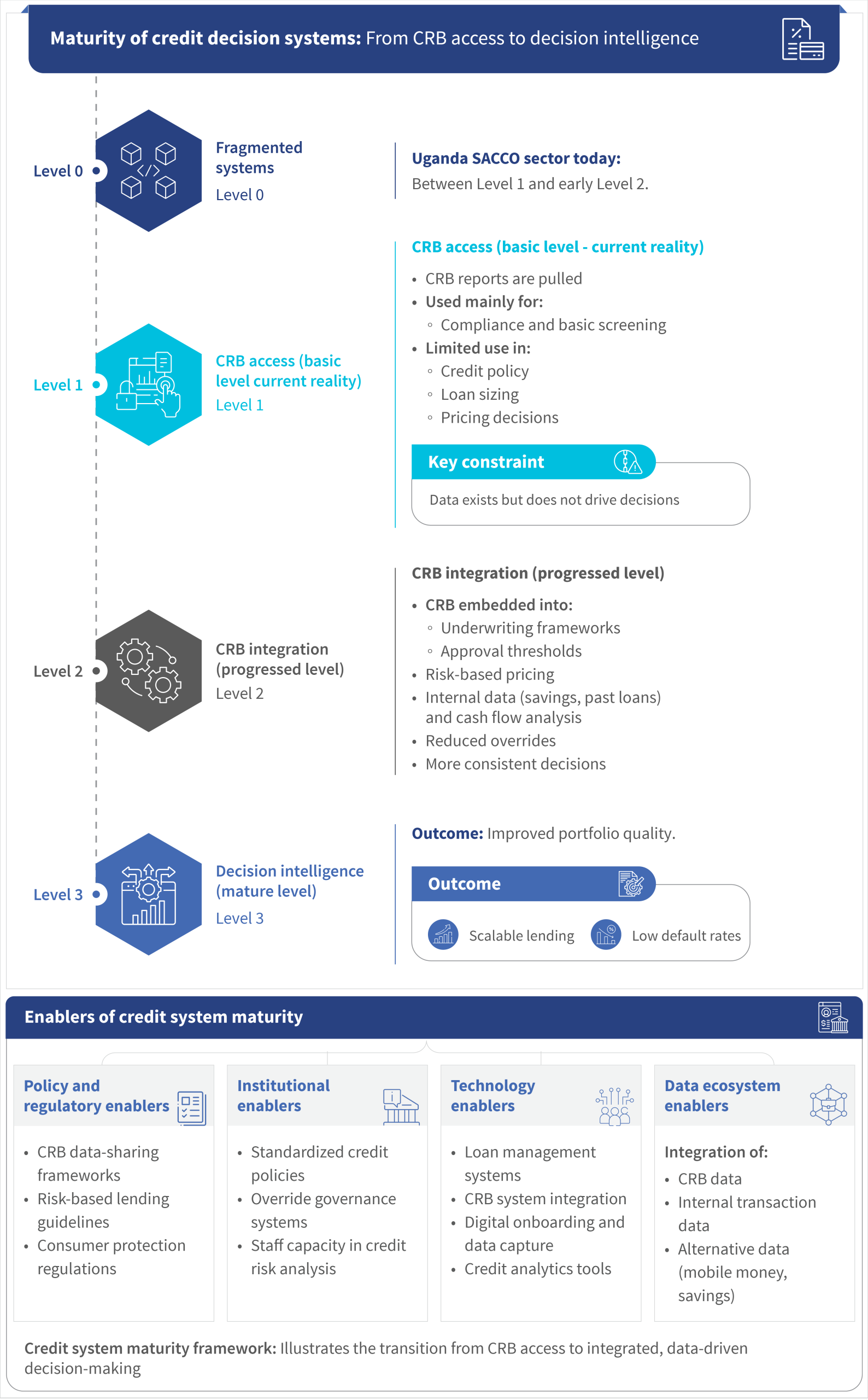

Uganda’s credit ecosystem has moved from data scarcity to data availability but has not reached decision-level integration.

Figure 5. Financial infrastructure maturity framework that illustrates the transition from basic functionality to fully integrated and interoperable systems

For MSERF 2.0 and similar initiatives, this requires a shift in focus to support SACCO digitization, pairing capital with technical assistance to strengthen credit risk management, data use, and institutional governance, and tracking decision quality alongside loan volumes.

Uganda’s experience shows that CRB systems improve transparency, but their impact depends on how effectively they are integrated into decision-making and how accurately scoring models reflect borrower realities. Poorly calibrated models can introduce bias, misrepresent risk, and weaken incentives for positive repayment behavior.

The focus has shifted from CRB adoption to effective CRB use for SACCOs and financial institutions. The key question is how to turn CRB data into better decisions, and ultimately, better outcomes.

Written by

Leave comments