Why Bangladesh’s supply chains still run on cash despite digitization

by Md Farista Andalib and Alvina Zafar

by Md Farista Andalib and Alvina Zafar May 14, 2026

May 14, 2026 6 min

6 min

Digital payments stop at the shop counter because retailers cannot forward funds to suppliers. Wholesalers and distributors reject digital money due to trapped balances, margin‑crushing fees, and the lack of instant, order‑matched confirmation. This situation keeps upstream supply‑chain payments stubbornly cash‑based.

A retail shopkeeper in Manikganj, Rubel single-handedly handles sales, ledger updates, and cash counting. He sells packaged foods, beverages, and household essentials, such as lentils, rice, and soybean oil. While he owns a Bangla QR from a mobile finance service (MFS) provider and understands merchant payments through this channel, he rarely uses it to receive payments from customers. The reason, though, is practical.

After Rubel receives a digital payment, he must withdraw the funds from a nearby agent and incur both merchant discount rate (MDR) charges and agent fees. Why is this so? Because the wholesalers and distributors who restock his shop demand cash instead of digital funds, which otherwise could be transferred to their accounts. As a result, even when customers pay digitally, Rubel must use cash to stay in business.

This experience is not unique to Rubel. Across Bangladesh’s 7.8 million small and medium retailers, digital payments often enter shops and businesses but cannot circulate through the supply chain. The issue is not whether retailers accept digital payments, but whether they can use digital money to restock inventory. Currently, most retailers cannot use digital money for restocking.

Bangladesh has been actively advancing the digitization of payments at retail points of sale. However, the broader digitization of liquidity flows across the supply chain has yet to begin.

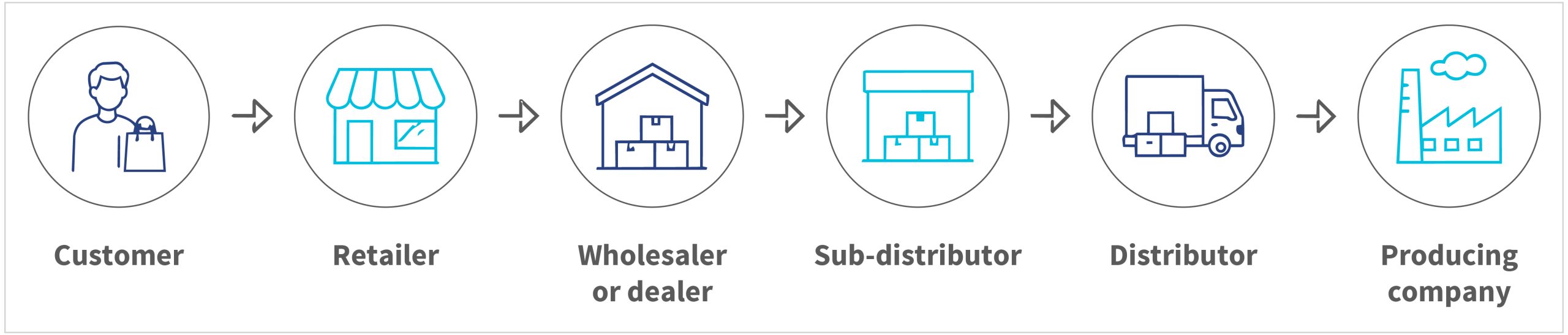

Wholesale and retail trade contribute nearly USD 160 billion (BDT 17.4 trillion) across the sector in 2025. Every retail transaction triggers a chain of upstream payments: Retailer to wholesaler, wholesaler to distributor, and distributor to manufacturer. These payment cycles keep essential goods flowing daily across the country.

MSC (MicroSave Consulting) conducted a long-term study of merchant digital payments to understand how they function in practice. The study highlights two critical findings:

- It shows that only a small share of payment flows, nearly 10% beyond the retail counter, remain digital once transactions move upstream into distributor and wholesaler payments.

- It reveals that around 37% of retailers avoid digital payments not because they prefer cash, but because their own suppliers, such as distributors and wholesalers, require cash settlement.

This pattern reflects a structural mismatch between how digital payment tools are designed and how retail supply chains actually function.

Bangladesh has made visible progress in the digitization of payments at the retail counter. Interoperable QR acceptance has expanded, mobile wallets have seen wide use, and consumers are increasingly comfortable with digital payments in everyday transactions. Digital payments are becoming part of routine commercial activity at the point of sale. However, payment flows change once they move beyond the retail counter to wholesalers and distributors.

Cash dominates payments in Bangladesh’s retail value chains despite the availability of interoperable payment tools, such as Bangla QR and the inter-FSP fund transfer system. More than 9 million microentrepreneurs, from fast-moving consumer goods (FMCG) shops to pharmacies and agri-business retailers, contribute roughly 25% to the nation’s GDP and drive significant economic activity. Yet most transactions between retailers, wholesalers, dealers, distributors, and producers still occur in cash. The challenge is not the absence of digital infrastructure. It is that existing payment pathways were designed primarily for people-to-business transactions (P2B), not for business-to-business (B2B) ones.

Digital money stops at the shop counter because existing payment tools are not designed to serve upstream business requirements. Consumer-grade payment tools were designed primarily to help businesses receive payments from customers. When these same tools are used for inventory purchases across supply chains, they fail to match the liquidity timing, pricing realities, and confirmation requirements of distribution networks. The following three operational barriers explain why digital money often stops at the shop counter instead of moving upstream.

Barrier 1: The retailer’s trap, money goes in, but cannot move upstream

When a customer pays retailers like Rubel digitally, the funds are received in the retailer’s mobile wallet. Rubel’s wallet could be a personal MFS account, such as bKash, Nagad, or Rocket, or a dedicated merchant wallet offered by the provider. In both cases, the funds cannot be easily forwarded to upstream suppliers for inventory restocking. However, the retailer cannot easily use those same digital funds to pay suppliers.

Most digital payment products, such as merchant wallets and QR-based collections are designed primarily to receive customer payments. While options, such as bank transfers or QR payments technically exist, they lack features essential for routine B2B use that include bulk transfers and seamless onward payments. As a result, funds become trapped. The retailer who receives a digital payment from a customer cannot easily forward those funds to wholesalers or distributors and are forced to cash-out.

Barrier 2: The distributor’s math, fees that work for shops do not work for bulk

A typical shopkeeper, such as Rubel, might make a profit of BDT 5 (USD 0.041) to BDT 10 (USD 0.081) for every BDT 100 (USD 0.81) of goods sold. A distributor, who moves goods in bulk, often makes only BDT 1 (USD 0.0081) to BDT 2 (USD 0.016) for every BDT 100 (USD 0.81) of goods sold. Digital payment fees, that is, merchant discount rates (MDR), are usually around 1%. For retailers, this fee is deducted from the payment they receive, but their profit margin is wide enough to absorb the cost. Yet for a distributor, the same 1% fee is deducted from the payments they receive from retailers. Since their margin is only 1% to 2%, this fee consumes half or more of their profit. As a result, even if the technology worked perfectly, economics would still block the adoption of digital payments upstream.

Barrier 3: The confirmation gap, which the distributors cannot afford to wait or wonder

When distributors hand over goods to retailers or wholesalers, they need immediate confirmation that payment has been received and matched to a specific order. Cash provides instant confirmation of payment. Existing digital payment tools cannot yet provide the order-linked confirmation and reconciliation that certain distributors require to release inventory confidently. These tools also do not support the partial-payment structures that are common in B2B transactions. As a result, distributors continue to rely on cash as it remains the only payment instrument that reliably matches inventory release with settlement confirmation.

These operational barriers are closely linked to how retail distribution networks function. Retail supply chains operate through layered relationships that connect retailers, wholesalers, dealers, sub-distributors, distributors, and manufacturers. Sales representatives (SRs) play a critical role in the delivery of goods, collection of payments, and confirmation of settlement across these networks.

Distribution routes depend on route-level confirmation and same-day liquidity availability, which makes the certainty of payment essential for inventory movement or management. Consumers increasingly use mobile wallets and banking apps for payments. However, transactions within upstream relationships remain overwhelmingly cash-based, as existing digital tools do not yet match the liquidity timing, confirmation certainty, and reconciliation needs of distribution networks.

The three operational barriers described are deeply embedded in the policy rules, provider systems, and merchant incentives that shape Bangladesh’s digital payments ecosystem for its vast number of micro, small, and medium enterprises (MSMEs).

- At the macro level, which covers policy, pricing, and rails: The same MDR misalignment and lack of instant settlement make digital payments economically unviable for distributors and break daily liquidity cycles.

- At the meso level, which covers provider systems and operations: The absence of batch payments, multi‑user access, and SR‑level reconciliation means distribution networks cannot replace cash‑based workflows.

- At the micro level, which covers merchant incentives and behavior: Retailers perceive digital balances trapped, as upstream actors demand cash, and settlement uncertainty discourages retaining digital value for inventory purchases.

Together, these reflections show that upstream payments remain cash‑based. The issue is not the unavailability of digital tools. Rather, the problem stems from the ecosystem, where policies, providers, and merchants remain focused on consumer-facing payments rather than supply‑chain settlement.

Bangladesh has successfully digitized customer payments at the counter. It has not yet been digitized how that money moves through the supply chain, from retailer to wholesaler to distributor to manufacturer. Until digital money can move upstream with the same speed, certainty, and reconciliation as cash, B2B payments will remain outside the country’s digital payment ecosystem.

Understanding this structural gap is the first step. Part 2 explores what this means for liquidity circulation, credit visibility, and the depth of Bangladesh’s digital transformation. Read the next part here.

Written by

Md Farista Andalib

Manager

Leave comments