Building the rails for B2B digitization in Bangladesh’s retail supply chains

by Md Farista Andalib and Alvina Zafar

by Md Farista Andalib and Alvina Zafar May 14, 2026

May 14, 2026 5 min

5 min

Cash‑based upstream payments trap liquidity, block credit access, and fragment supply chain data. Digitization requires supply chain‑native architecture. This includes instant settlement, distributor‑friendly fees, embedded reconciliation, and seamless fund circulation across tiers so digital money flows as reliably as goods.

Part 1 of this series discussed how Bangladesh’s digital payments ecosystem works well at the retail counter but breaks along supply-chain payment routes. Digital money enters shops through QR-based transactions and interoperable transfers, yet it rarely travels further upstream to wholesalers, distributors, and manufacturers. It affects the growth of MSMEs in Bangladesh and the way it happens across emerging markets and developing economies (EMDEs) .

In cash-based supply chains, the confirmation of transactions is instant. Digital payments have not yet matched that certainty. Until they do, businesses will continue to reach for cash, and the supply chain will depend on informal, unrecorded transactions.

Digitizing B2B payments, therefore, changes more than payment methods. It changes how liquidity circulates, how credit is assessed, and how supply chains are managed. If upstream payments remain cash-based, four structural consequences follow.

1. Liquidity remains tied to physical movement rather than digital circulation

Retail distribution operates on daily working-capital cycles. Today, liquidity moves quickly within local cash-based routes, but that speed depends on physical handling, transport, and deposit. This limits how efficiently funds move across actors, locations, and financial institutions.

The risk is that cash is slow. As a result, payment speeds continue to depend on physical proximity rather than on real-time confirmation across the supply chain. Inventory release remains tied to where cash is located, not where digital liquidity could circulate instantly.

2. Supply-chain credit cannot scale without transaction visibility

If B2B payments remain cash-based, millions of businesses stay invisible to lenders. A retailer may purchase goods from the same distributor every week for years. Yet, without digital transaction histories, that relationship remains outside formal credit systems. Without verified purchase records, lenders cannot reliably assess how much a business earns, their repayment discipline, or inventory cycles.

As a result, lenders continue to exclude retailers and distributors from structured working-capital financing despite their active participation in the retail economy. Digital supply chain payments would make these commercial relationships visible and help develop inventory-linked lending and distributor-anchored credit models.

3. Inventory intelligence remains fragmented across supply chains

Cash-based transactions make reconciliation slow. Distributors and sales representatives report incidents inconsistently across networks. Manufacturers lack visibility into distributor-level offtake. Distributors manage fragmented ledgers across routes and outlets, while policymakers lack reliable insights into transaction flows across retail networks.

Without digital settlement trails, supply chains cannot generate the transaction intelligence required to forecast demand, manage inventory efficiently, or support evidence-based policy decisions to formalize the retail sector.

4. Cash-handling risk remains embedded in distribution operations

Across distribution routes, sales representatives and distributors handle large volumes of cash daily. Each step, including collection, transport, counting, deposit, and reconciliation, introduces operational risks and cost.

The lack of better digital payment solutions for upstream supply chains ultimately constrains the growth of MSMEs in Bangladesh. When digital money cannot flow from retailers to distributors to manufacturers, working capital stays trapped, formal credit remains out of reach, and millions of small businesses operate below their potential. Digital transformation must extend beyond the shop counter to drive inclusive economic growth.

The persistence of cash in upstream retail payments is not primarily a question of merchant awareness or consumer adoption. Bangladesh already has widespread QR infrastructure, strong mobile financial services usage, and expanding interoperability across providers.

Regulators and payment providers designed the existing pathways for person-to-business transactions, not for distributor-led inventory payment settlement across layered supply chains. Distribution networks depend on route-level confirmation, thin-margin settlement economics, and same-day liquidity cycles. Without payment systems that reflect these operational realities, digital tools cannot replace cash for inventory purchases.

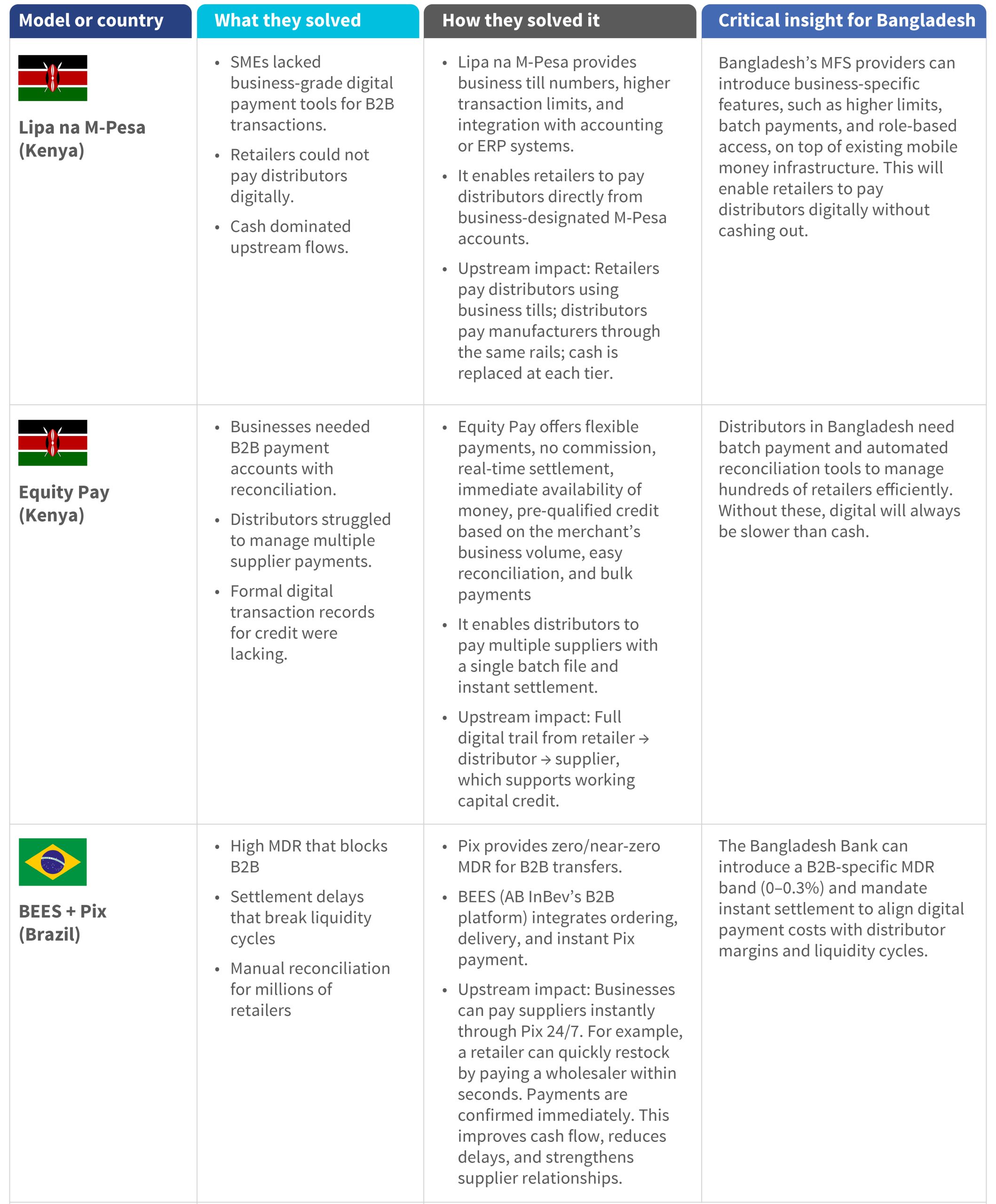

Experience from other markets show that upstream digitization succeeds only when payment architecture is redesigned around supply-chain economics rather than consumer payment behavior. Bangladesh alone does not face breaks in supply chains. Across emerging markets, consumer payments digitized quickly while B2B flows remained cash-dependent due to liquidity timing, reconciliation gaps, misaligned merchant discount rate (MDR) structures, and sales-representative-driven workflows.

These markets overcame these constraints through ordering, delivery, and settlement systems rather than treating payments as a separate layer.

So, what will it take to digitize B2B payments in Bangladesh? Global experience shows that B2B digitization succeeds only when payment architecture reflects the realities of supply chains. For Bangladesh, five design principles emerge clearly.

- Instant settlement as the foundation, not a feature: Distributor liquidity cycles operate daily. If settlement is delayed or uncertain, inventory release slows immediately. B2B payments require guaranteed real-time settlement aligned with inventory movement rather than end-of-day confirmation cycles.

- MDR and pricing rules aligned with distributor margins: Consumer-grade MDR levels do not match wholesale distribution economics. As seen in Brazil’s Pix model, zero or near-zero MDR enabled B2B payments to scale rapidly across thin-margin supply chains. Pricing frameworks for B2B transactions must reflect the operating margins of distributors, which MSC’s research shows are often only 1–2%. This can be achieved through tiered pricing structures, capped transaction fees, or near-zero cost transfers for high-value supply chain payments.

- Reconciliation must be embedded within distribution workflows: B2B payments function reliably only when ordering, delivery, and settlement confirmation are synchronized. Payment confirmation must be visible to retailers, sales representatives, distributors, and manufacturers simultaneously. Dispute-resolution mechanisms must link directly to digital invoices and the delivery of receipts.

- Digital funds must remain usable across supply-chain tiers, not trapped within merchant collection channels: When a retailer pays a distributor digitally, the distributor must be able to reuse those same funds immediately for upstream purchases from manufacturers or suppliers. Today, most digital collection tools do not support seamless onward circulation across supply-chain relationships. Without this ability to reuse incoming digital liquidity across tiers, payment systems cannot support continuous digital settlement along distribution routes.

- Incentives must support upstream liquidity circulation: Supply chains depend on the predictable availability of liquidity. If distributors cannot reuse incoming digital funds immediately for upstream purchases, they revert to cash. Settlement certainty must be combined with liquidity-assurance mechanisms that support continuous digital circulation across supply-chain tiers.

Bangladesh has successfully digitized how consumers pay in shops, but not the movement that keeps supply chains running. Upstream flows remain cash-driven because existing payment pathways were never designed for high-value, time-sensitive distribution networks. The next step, therefore, is to enable digital liquidity to move across the supply chain with the same certainty as cash. Bangladesh does not need more digital touchpoints. It needs digital money that can move with the same reliability as the goods it pays for.

Written by

Md Farista Andalib

Manager

Leave comments