Financing Africa’s fisheries: From informality to investability

by Emma Odera, Dennis Kuria and Pranav Singh

by Emma Odera, Dennis Kuria and Pranav Singh Jun 2, 2026

Jun 2, 2026 5 min

5 min

This blog highlights the journey from informal fisheries enterprises to finance-ready businesses through lessons from Kenya’s Kamarinyang Aqua Park. It emphasizes the role of financial education, stronger governance, and fit-for-purpose finance in driving sustainable growth.

Kamarinyang Aqua Park in Busia County, Kenya, illustrates both the promise and the financing challenge within Africa’s fisheries sector. The Kenya Climate-Smart Agriculture Program was established around 2021, in partnership with the County Government of Busia. The Aqua Park received more than KES 65 million (~USD 503,000) in investment and established 78 fishponds.

Yet, infrastructure alone did not result in a functioning enterprise, as the ponds remained unstocked. Project members also lacked the financial capability and collective management systems needed to operate the facility productively. This gap highlights how grant-funded initiatives can struggle to sustain impact without a viable market or a clear enterprise pathway.

The situation changed in March 2025, when 130 members received financial education and training on group dynamics from MSC (MicroSave Consulting) and the Association of Women in Fisheries Blue Economy Kenya (AWFBEK). Members reorganized into sub-groups, assigned pond responsibilities across women, youth, persons with disabilities, and cooperative members, and agreed to contribute KES 100 (~USD 0.77) every two weeks to support joint activities.

By June 2025, the ponds were stocked with tilapia and catfish, and the first harvest followed in February 2026. The shift went beyond pond use to include greater ownership, accountability, and readiness to engage more effectively with formal and digital finance, such as the Chama app.

The Kamarinyang story goes beyond financial education. It shows how enterprise support financial capability and how sector-appropriate finance must come together to move fisheries enterprises from informality toward investability. It also reflects a wider challenge across the fisheries sector.

Africa’s fisheries and aquaculture sector faces two competitive realities. It is already a major source of food and nutrition, with aquatic foods supplying about 18% of animal protein in Africa. At the same time, the continent faces a projected annual fish deficit of 11 million metric tons by 2030 unless supply expands significantly. Meeting this demand will require a substantial increase in production.

Aquaculture is widely seen as a sustainable and viable pathway. Yet, the investment needed to scale production in Africa has not materialized, with, according to recent analyses, an estimated annual financing gap of approximately USD 12 billion.

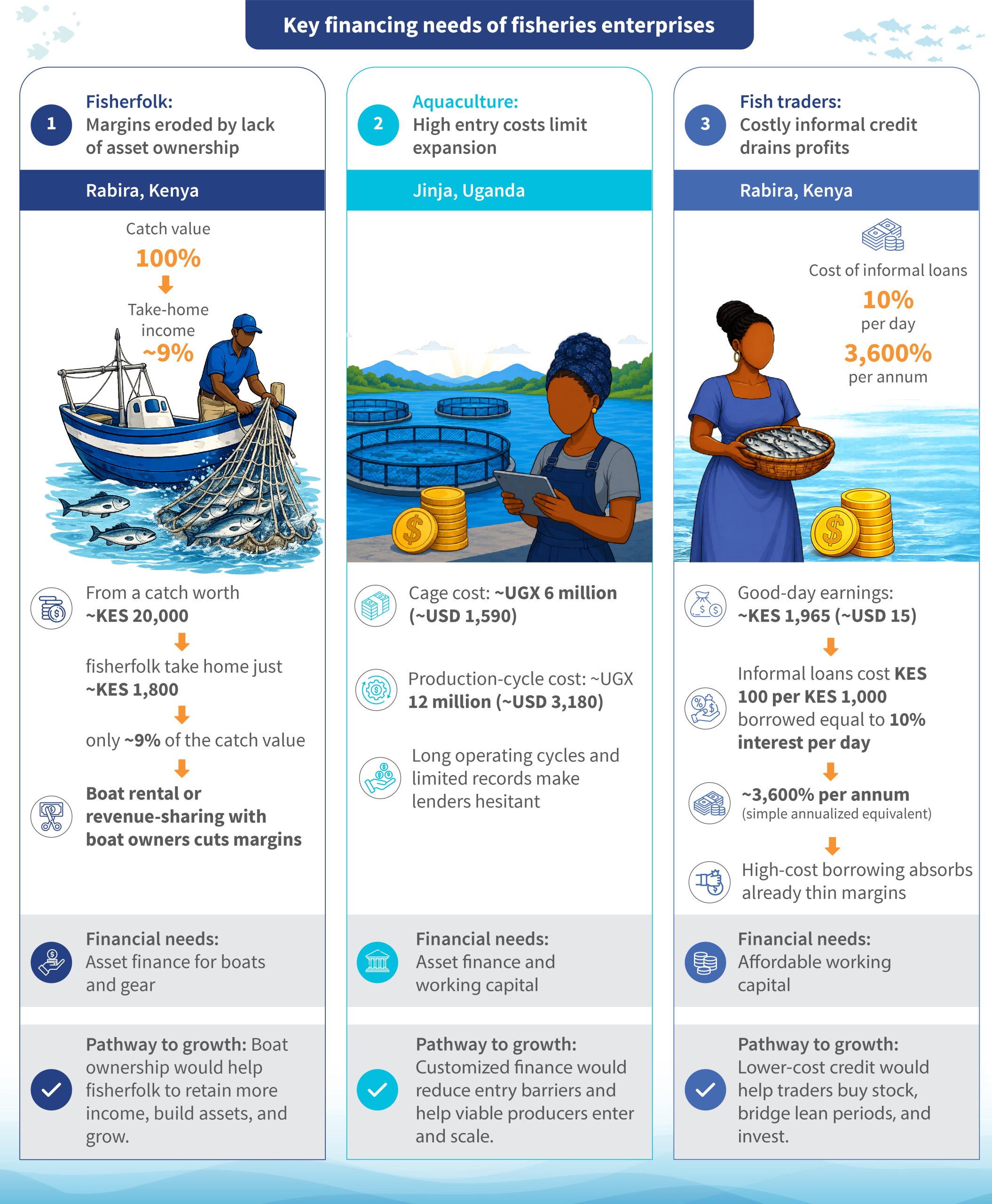

Financial institutions often perceive the fisheries sector as inherently high risk and commercially unattractive. Some of this risk is real, driven by weak records, limited collateral, long production cycles, and high transaction costs relative to the size of small loans. Yet, this perceived risk also reflects limited familiarity with the sector, as indicated by MSC’s engagement with partner financial institutions (PFIs).

Many lenders do not fully understand how fisheries enterprises operate, such as their seasonality, cash flow patterns, margins, growth trajectories, and risk exposure. This limits their ability to assess creditworthiness or design products that meet their working capital and investment needs. In aquaculture, this challenge is even more pronounced, as lenders must assess biological risks, such as disease outbreaks, stock losses, and weather-related shocks. They often lack the sector knowledge needed to interpret these risks effectively.

Yet, fisheries enterprises conduct substantial commercial transactions and demonstrate strong business discipline, despite constrained resources and market conditions. Young women and men are central to the fisheries economy, which accounts for 70% of employment in the sector across East and Southern Africa.

Many transactions are organized through Beach Management Units (BMU), chamas, and other local networks that help businesses coordinate, save, borrow, and trade. The problem is that much of this economic activity is informal and poorly documented. As a result, businesses with real turnover, market relationships, and demonstrated financial discipline remain largely invisible to lenders.

MSC’s work in the sector reveals the intensity of this activity and the extent of unmet financial need. These enterprises cannot grow, modernize, or scale operations without finance or acquire productive assets. They remain commercially active but structurally constrained.

High-cost informal borrowing diverts cash from already thin margins, limiting traders’ ability to reinvest profits and expand their businesses. These examples highlight the sector’s unrealized potential. If these enterprises can survive, adapt, and continue transacting under such constrained conditions, their growth potential with access to appropriate finance, assets, and business support is likely to be far greater.

The financing challenge in fisheries cannot be solved through a single intervention. When enterprise transactions are poorly documented and business practices remain informal, financial institutions struggle to assess cash flows, governance, repayment capacity, and risk. As a result, viable businesses may be excluded from credit or offered products that are too costly, too short-term, or poorly aligned with their operating cycles. This weakens repayment capacity and discourages demand for formal finance, even among commercially active enterprises.

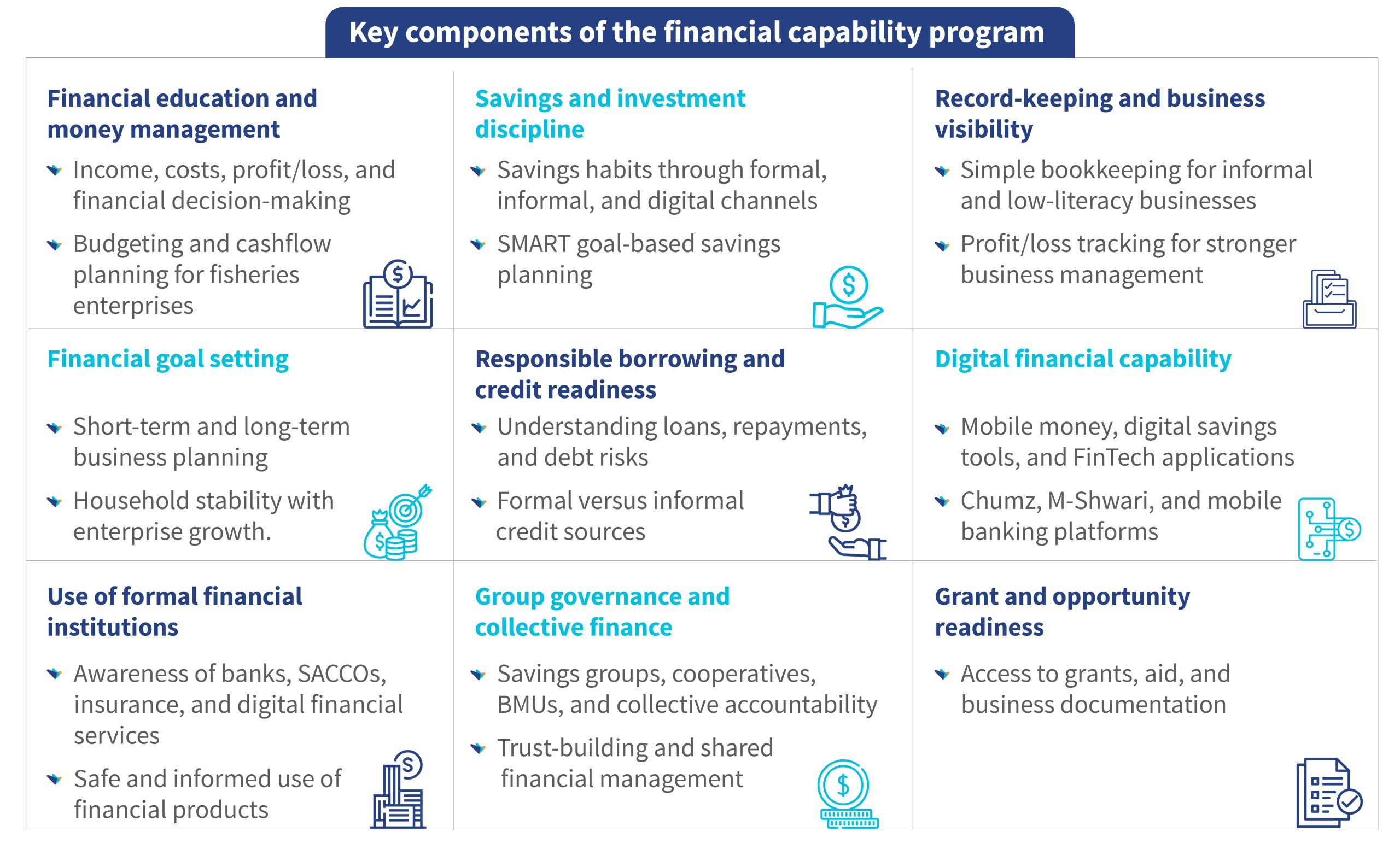

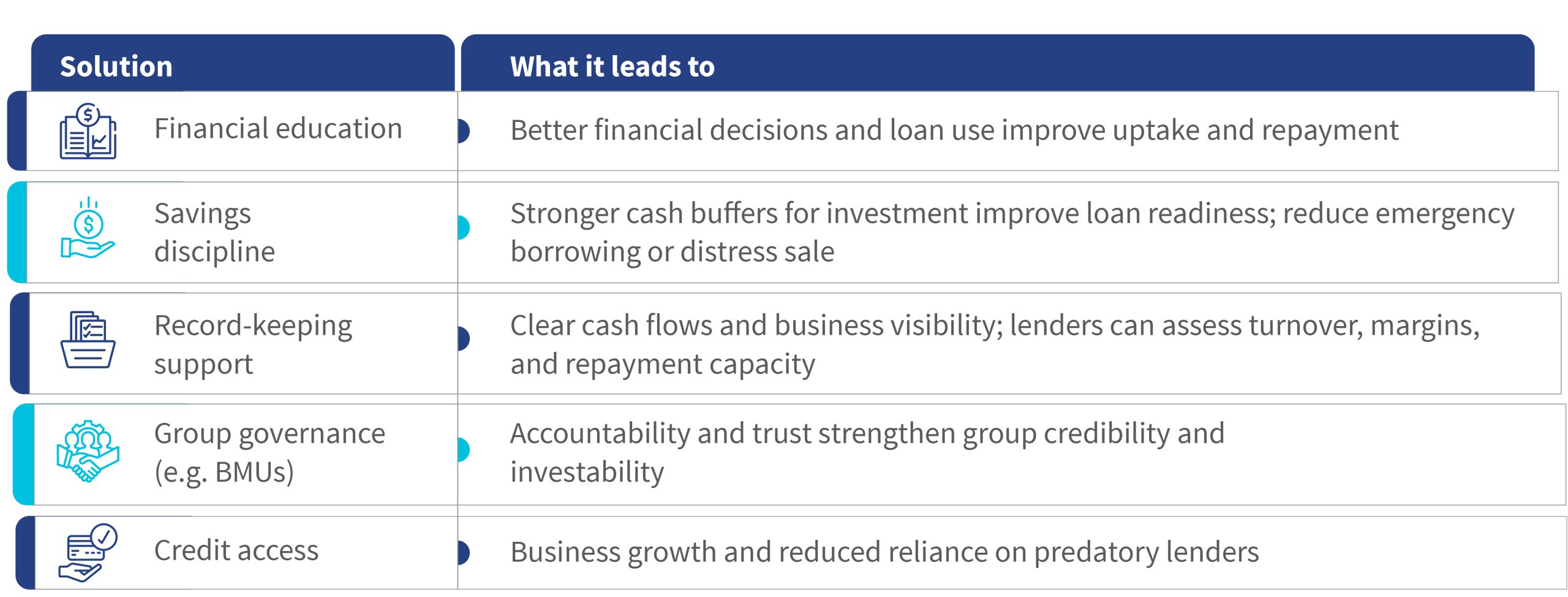

These constraints require financial education and enterprise support. Savings discipline, record-keeping, technical training, and stronger group governance help translate informal economic activity into information that financial institutions can use. While they cannot eliminate all risks, they reduce uncertainty and make businesses easier to understand and assess.

Financial education also influences how entrepreneurs engage with financial services. Familiarity with financial terms, product features, loan conditions, and repayment obligations can support better borrowing decisions and long-term financial health.

However, effective financial behavior requires more than training. Financial education is more likely to influence behavior when it is practical, delivered at teachable moments, and linked to timely access to relevant financial solutions. This approach allows entrepreneurs to apply and consolidate new knowledge and build financial capability through use.

MSC’s ongoing work under Women and Youth Economic Empowerment in Fisheries through Inclusive Market Access (WYEEFIMA) reflects this approach. This project combines enterprise support with financial sector engagement to improve financial readiness and unlock more suitable pathways to inclusion, sustainability, and job creation.

The following table summarizes how specific financial capability interventions address key constraints and support better outcomes for fisheries enterprises.

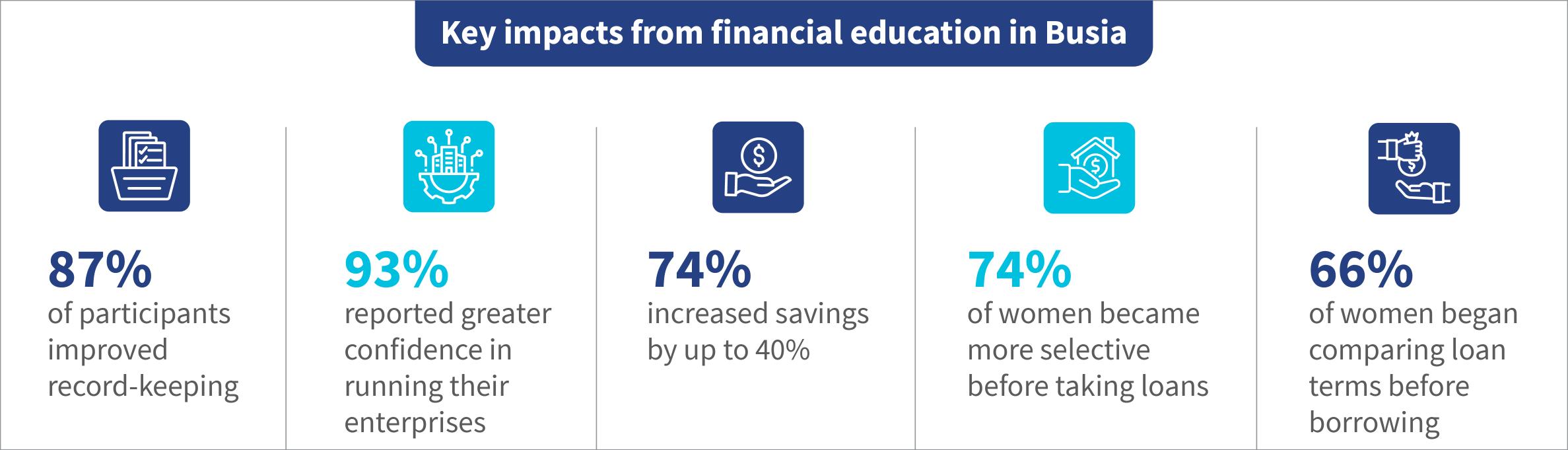

Financial education lays the foundation for graduating from informal mechanisms to structured financial services. MSC’s post-training results in Busia show how stronger financial capability can improve financial readiness by making business performance and risk more visible and manageable.

For financial institutions, the opportunity extends beyond increased lending to fisheries enterprises. It includes creating structured pathways that help commercially active enterprises become finance-ready and bankable. They must distinguish the needs of different actors, such as working capital for traders and asset finance for producers, and design products that reflect production cycles, cash flow patterns, and repayment realities. These institutions must also improve underwriting for informal enterprises by working with partners to strengthen financial capability, governance, record-keeping, and transaction visibility.

Africa’s fisheries sector has strong demand and a diverse enterprise base. Yet, it lacks a financing system that understands the sector’s business cycles and uses increasingly accessible, high-quality data to recognize viable businesses and inform product specifications. Financial institutions, value-chain actors, development partners, and local enterprise networks must act in coordination to close this gap. Together, these stakeholders can strengthen business discipline, improve visibility, and design fit-for-purpose financing that enables enterprises to grow.

Over the next three years, MSC will partner with financial institutions and sector partners to test practical pathways to expand finance for commercially active fisheries enterprises. We invite financial institutions to collaborate to strengthen fisheries portfolios through better underwriting, fit-for-purpose products, and enterprise support.

Leave comments