Driving transformative financial inclusion across India’s aspirational blocks by unlocking the power of last-mile convergence

by Sushma Kaw and Ravi Prakash Kaushal

by Sushma Kaw and Ravi Prakash Kaushal Apr 22, 2026

Apr 22, 2026 6 min

6 min

Interdepartmental convergence lays the foundation for joint action planning. This approach enables coordinated service delivery across departments and bridges top-down operational gaps, which are unaddressed, and weaken last-mile impact. In this blog, we show how collaborative execution helps close these gaps.

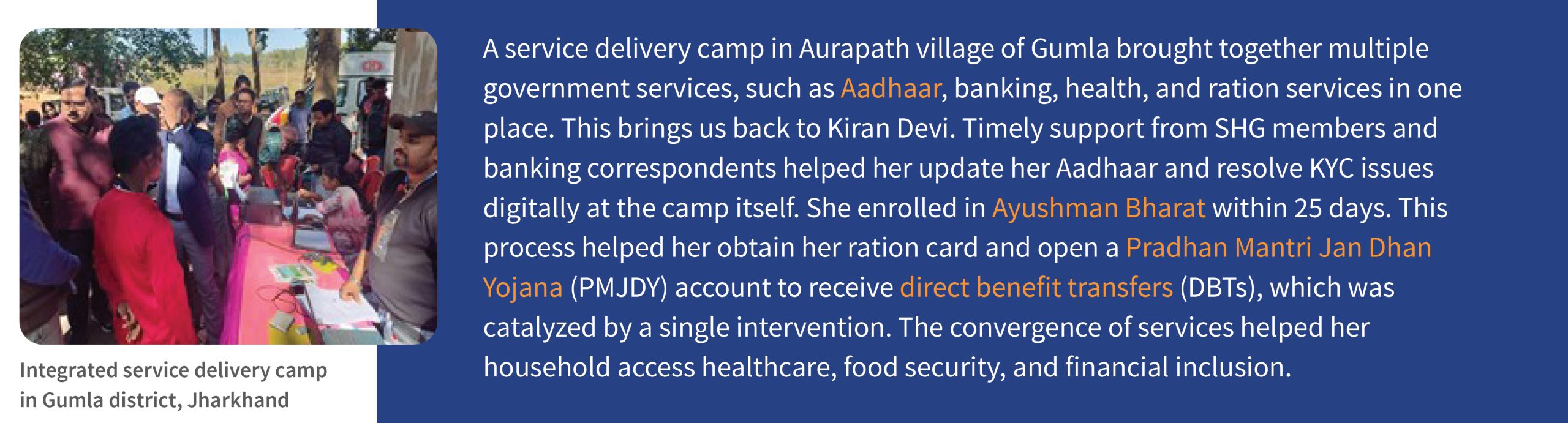

Kiran Devi comes from a remote tribal village in Gumla district in Jharkhand. Recently, her village hosted a community outreach camp to help residents access key government services, such as ration cards and Ayushman Bharat health cards, and open bank accounts. Kiran Devi needed these services, yet she could not participate in the camp due to apprehensions.

Her hesitation stemmed from fears about several challenges, which include procedural uncertainties, documentation gaps, and prior difficulties with know-your-customer (KYC) processes. This was not a case of a lack of demand, but a delivery failure caused by fragmented processes and weak follow-up.

Many households in India’s aspirational blocks and particularly vulnerable tribal group (PVTG) areas share Kiran Devi’s experience. They face barriers to prerequisite processes, such as Aadhaar updates or bank account requirements, which affect access to multiple welfare programs. Government departments and financial service providers have made significant efforts to promote the use of formal financial services through enrollment drives and financial literacy campaigns. However, these also leave a proportion of the population underserved.

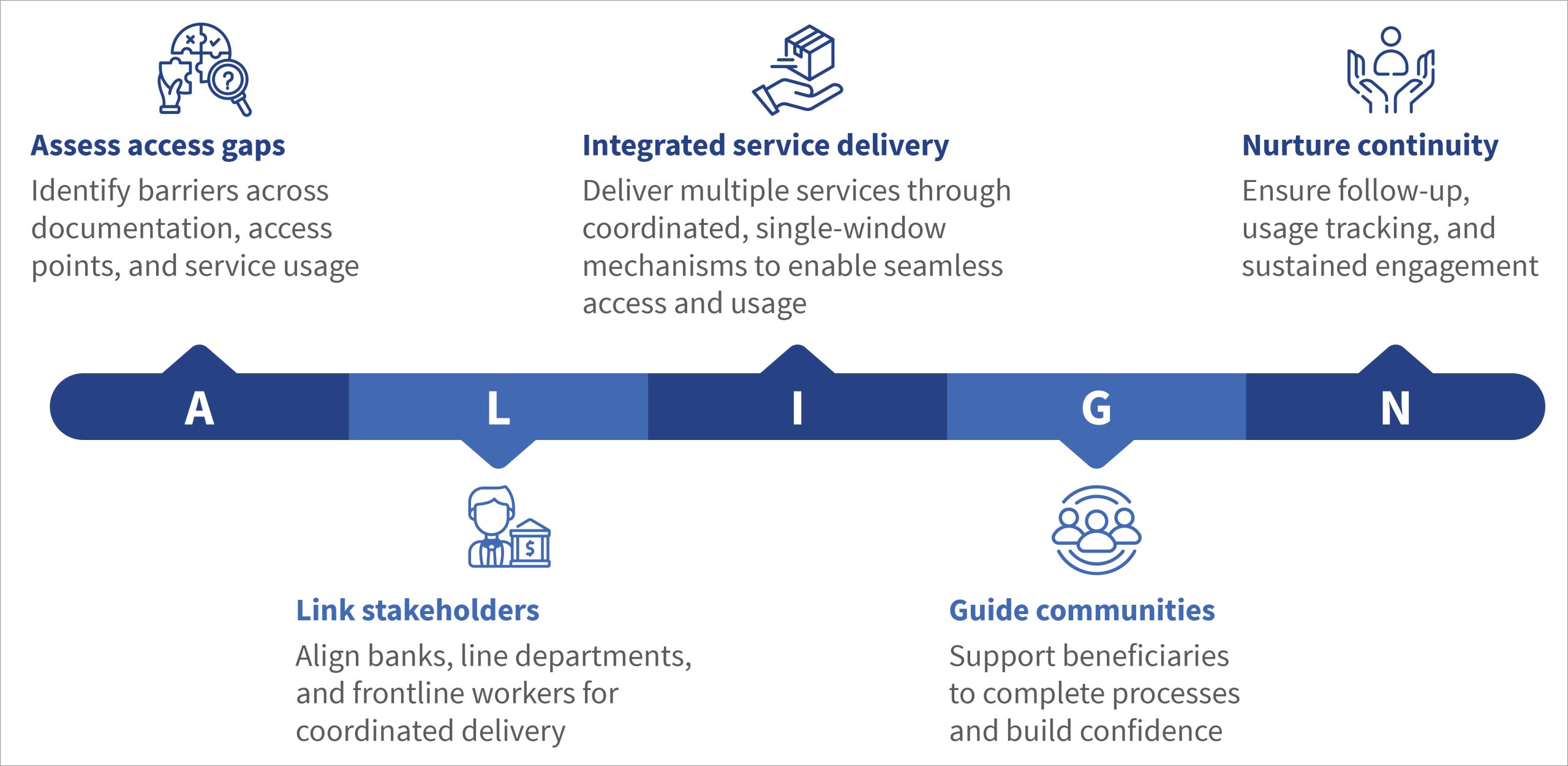

Lessons from the ground show that when we integrate the delivery of services with regular follow-up and provide consistent guidance, people participate easily, and inclusion is more effective. These insights often lead to a shift from isolated service delivery to coordinated, people-centric approaches. To operationalize this shift, the ALIGN framework provides a simple pathway for local governing bodies to design and deliver convergence-led financial inclusion efforts.

The following examples clearly demonstrate this shift.

Expansion of financial services access through integrated camps: A case study from Gumla district, Jharkhand

The district administration in Gumla, Jharkhand, redesigned its approach and built customer centricity into its service delivery model, particularly for financial and social inclusion. It recognized that lasting impact comes from convergence, where banks, government departments, self-help groups (SHGs), and frontline workers coordinate over time. With MSC’s support, the administration organized and integrated one-stop camps that combined awareness, enrollment, and troubleshooting (A-E-T).

Unlike regular camps that focus on single services or one-time enrollment, these camps address multiple needs together. They resolved documentation issues on the spot, provided step-by-step guidance, and ensured follow-up after the camp. This approach reflects a structured model of awareness, enrollment, and troubleshooting (A-E-T), ensuring residents complete processes rather than return repeatedly without resolution.

Figure 3 links:

Aadhaar

Ayushmaan

PMJDY

Direct benefit Transfer

The District Program Manager of SRLM Gumla reflected on the issue of convergence and noted that “without coordinated, doorstep delivery of services, many would remain excluded or less engaged with financial services. This integrated approach has helped build community trust and ensured that no one is left behind due to procedural barriers.”

Kiran Devi’s story proved that meaningful inclusion takes time, coordination, and commitment in making service delivery more customer centric. MSC has supported district administrations across aspirational blocks and districts in several states to apply similar convergence-led approaches to financial inclusion.

Lessons from dedicated efforts in Kaushambi district, Uttar Pradesh

In Uttar Pradesh’s Kaushambi district, a collaborative approach to design and implement financial literacy camps helped drive greater financial awareness and access, with the involvement of the district leadership, financial institutions, and local governance. This inter-departmental collaboration brought together key stakeholders to align priorities and drive collective action for the effective delivery of outreach activities. Participants included representatives from the district administration, Bank of Baroda (the lead bank), the National Bank for Agriculture and Rural Development (NABARD), the State Rural Livelihoods Mission (SRLM), and local governance institutions.

The collaborative initiative led to critical actions that strengthened the delivery of outreach camps. For instance, the sensitization and training of Gram Panchayat Pradhans, the elected heads of a village council, to strengthen community participation. This initiative shows how targeted financial literacy initiatives can effectively reach unserved or underserved regions when backed by institutional coordination and local leadership. As part of the initiative, a month-long financial literacy campaign was conducted to activate bank accounts, link beneficiaries to programs, and enroll them in insurance products. The campaign covered the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and the Pradhan Mantri Suraksha Bima Yojana (PMSBY). The campaign involves participation of more than 5,000 citizens and emphasized on ways to translate access into usage. It moves beyond mere awareness and ensure that beneficiaries opened accounts and services and used them actively. The campaign focused on specific goals, which includes account enrollment, KYC completion, insurance coverage, and promotion of digital transactions.

The camps brought together all the key local stakeholders under a single platform through departmental convergence. The convergence addressed local needs, promoted trust-building, and supported practical usage of financial services through collaboration with banks, insurers, financial literacy counselors, and Gram Panchayat Pradhans.

It demonstrated how well-coordinated, goal-oriented efforts, supported by multi-stakeholder partnerships, can bridge gaps in access and usage and move the financial literacy drive into pathways for sustained financial empowerment.

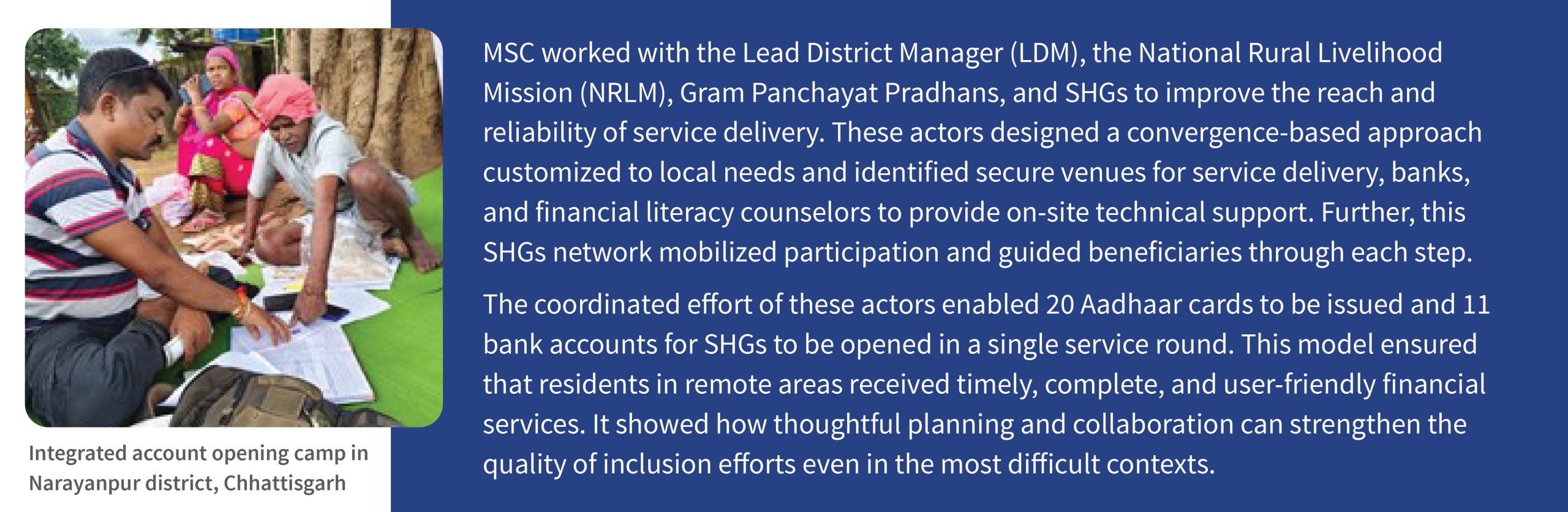

Addressing service gaps in remote areas: Convergent approach in Narayanpur district, Chhattisgarh

The Orchha block in Narayanpur district of Chhattisgarh has long faced unique challenges in terms of access to formal financial services due to its location, security concerns, and limited infrastructure. These factors often mean that services take longer to reach communities and require additional effort from residents.

The convergence approach has led to measurable results across India’s underserved areas. From March 2024 to March 2025, the effort led to the addition of more than 40,000 new banking touchpoints (bank branches/ Business Correspondents (BC)/India Post Payments Bank (IPPB) centres) in the aspirational blocks. Over the same period, Pradhan Mantri Jan Dhan Yojana (PMJDY) accounts increased by 7%, while Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) enrollments expanded by 38% and Pradhan Mantri Suraksha Bima Yojana (PMSBY) enrollments grew by 22%. These changes reflect growth in access to and uptake of these schemes, with all values expressed per 100,000 population. across some of the country’s most underserved regions. This effort highlights how sustained collaboration can transform financial access into meaningful usage that ensures that women, low-income families, and remote communities are included and empowered through active participation in the financial ecosystem.

Convergence as a strategy for inclusion

Financial inclusion is not a one-time intervention but a continuous process of building access, usage, and trust. Experience from India shows that progress is most effective when local governments, financial institutions, and communities work in coordination, rather than in isolation. These efforts demonstrate that convergence across stakeholders is essential to make financial systems accessible, responsive, and sustainable, particularly for underserved populations.

In each case, the fundamental enabler was not a single program, but multiple parts of the system. The availability of Aadhaar, ration card, and bank services at the same location meant that one missing document no longer halted progress. Additionally, the presence of SHG members, local leaders, and frontline workers bolstered confidence, provided guidance, and encouraged participation.

Convergence remains a highly effective strategy to bridge financial inclusion gaps and create lasting change. It works best when a single coordinated approach integrates government initiatives, financial institutions, and community participation to improve access, promote active usage, and build trust in financial services. Convergence is most effective when it appears seamless to the person who receives the service. Joint planning and delivery across departments ensure that beneficiaries receive multiple services in one visit. Simple, technology-enabled tools streamline the process, while trusted local actors promote trust and engagement.

As a result, sustained coordination and local follow-up are essential to transform initial access into long-term financial inclusion. This coordination enables millions of people, such as Kiran Devi, who live in India’s more remote corners, to participate in the economy and live a life of dignity.

Written by

Sushma Kaw

Manager

Leave comments