Beyond borrowing: How women in Tangail make sophisticated investments

by Ihsan Mahboob Hoq and Tajul Islam

by Ihsan Mahboob Hoq and Tajul Islam Jun 2, 2026

Jun 2, 2026 7 min

7 min

In Tangail, Bangladesh, long-term MFI members have transformed from borrowers into sophisticated investors. They channel accumulated savings into productive assets without formal guidance. Yet, the lack of trusted investment options exposes them to risk and highlights the need for stronger investment pathways

“Cattle, savings, and hard work keep my household standing,” remarks Mita Ghosh, a BURO member for more than a decade.

Mita joined the microfinance institution (MFI) BURO soon after she got married. Her mother-in-law was already a member and brought her to a BURO meeting. At her first session, she learned why saving matters and began to put aside BDT 20 (~USD 0.16) each week. Over time, her savings grew and she took a bold step and took her first loan for BDT 67,000 (~USD 546). The purpose was to finance her child’s education and buy a cow to support the household by selling milk. She repaid the loan, borrowed again for buying some ducks. She repeated this cycle to buy income generating assets and repay until she no longer needed loans. Over time, her focus shifted from accessing credit to deciding where and how to invest her growing savings

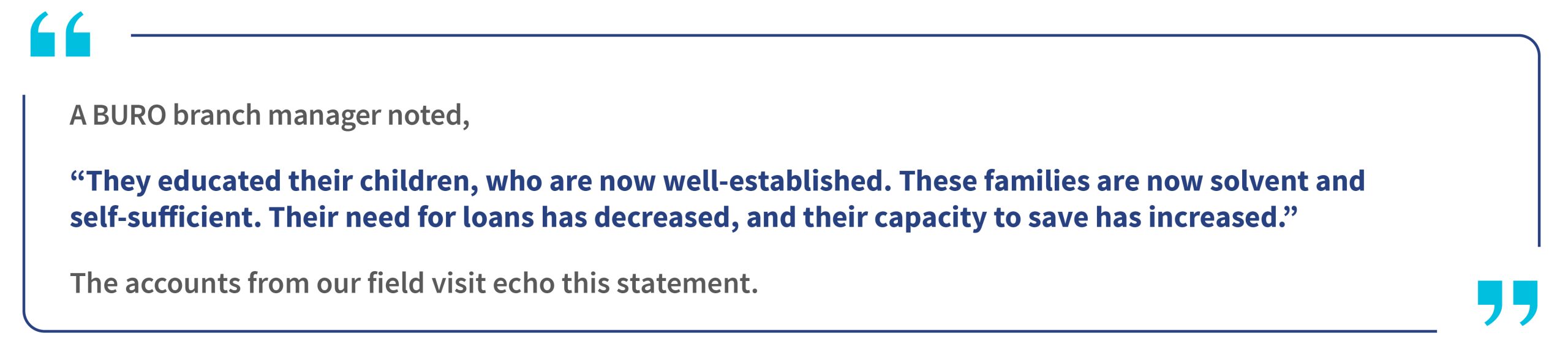

Institutions, such as BURO Bangladesh, have helped expand financial inclusion for their low- and moderate-income members by building savings habits early. 32 years ago, BURO experimented with flexible savings, on the view that forced savings do not create voluntary discipline. The industry practice was to have a mandatory savings for any active loans, which could be withdrawn only if the loan has been fully repaid. BURO realized this will deter customers from creating long term savings habit. 30 years later, it has played out exactly how they planned.

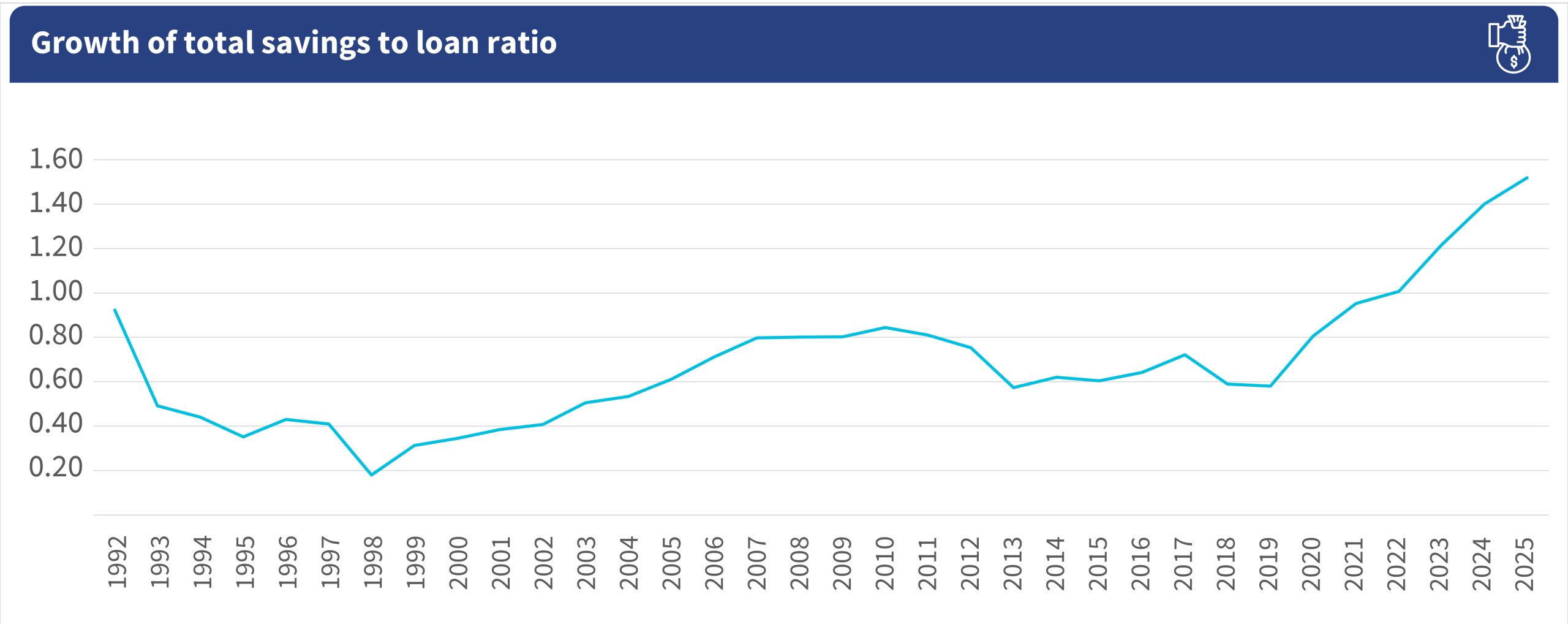

Currently, in the five model BURO branches in Tangail, savings have outgrown borrowing, and members save consistently and borrow strategically. The members built financial acumen through periodic financial literacy camps and knowledge-sharing sessions. Members could choose savings products that fit their needs. Branch level data shows The savings-to-loan ratio across the five model branches remained below 1 in the early years, meaning total amount of outstanding loans was greater than total deposit. Savings-to-loan ratio fell to its lowest point of 0.2 in 1998, when borrowing significantly outpaced savings. The trend then gradually reversed as members accumulated deposits over longer periods. The ratio reached parity in 2022, when savings equaled outstanding loans, and rose further to 1.55 by 2025. This shift indicates that many long-term members have transitioned from net borrowers to net savers.

Source: BURO’s historical branch-level data

Ratna from Dewli branch joined as a member 15 years ago. She has saved more than BDT 700,000 (USD 5,700) through consistent weekly deposits. She farms and rears cattle to support her family and borrows only when necessary. Meanwhile, Mina from Atia branch owns five cows and plans to acquire two more. She took a loan last year to build a bigger cowshed and has repaid it in full.

Sakhina Begum runs a grocery shop, which she built entirely from her own savings. She paid for her three daughters’ weddings without borrowing money. She still maintains an active Deposit Pension Scheme (DPS) account for her son’s future. Similarly, Aruna from Pathrail saved consistently for 16 years. She began with just a BDT 5,000 (~USD 40.67) loan and a BDT 500 (~USD 4.07) monthly DPS. Over time, she motivated her whole family to save. After years of saving, the family funded their daughter’s education, marriage, and resettlement.

We saw the same progression across several BURO branches in Tangail. Members initially borrow to finance reliable income-generating activities, such as livestock, small businesses, or electric autorickshaws. Over time, they increasingly rely on savings for major household goals, including children’s education, marriages, home improvements, and migration abroad. Borrowing gradually shifted from necessity to choice. Typically, members invest in four things: Livestock, electric autorickshaws, gold, and land.

The first two of these investments yield regular income and can be managed from the homestead. Cows are a great asset, as highlighted by Stuart Rutherford in his book The Poor and Their Money, livestock functions as both an income-generating asset and a form of savings. However, livestock investment also has practical limits. Most households can manage only about five cows and a few chickens due to land and space constraints.

Electric autorickshaws are popular investments. Women often buy one and rent it out, usually to a family member between school and work or to someone looking for a job. Another important investment is gold. In Bangladesh, gold functions as an appreciating, portable, and liquid asset. Gold is a store of value and a key requirement for marriage, especially for the daughters of members.

Across Dewli, Atia, and Pathrail branches, women run 10-year contractual accounts earmarked for their daughters’ jewelry. Mukta Begum has two contractual savings accounts to buy gold: One in her own name and one in her daughter’s name.

Land is the next big investment. Our research found that most long-term members buy a plot, either farmland that they rent out at harvest or land near town for residential and commercial purpose. It is capital intensive, hard to liquidate, and comes with legal bottlenecks. However, land is where members park money once they have built a base and considers it as a personal milestone.

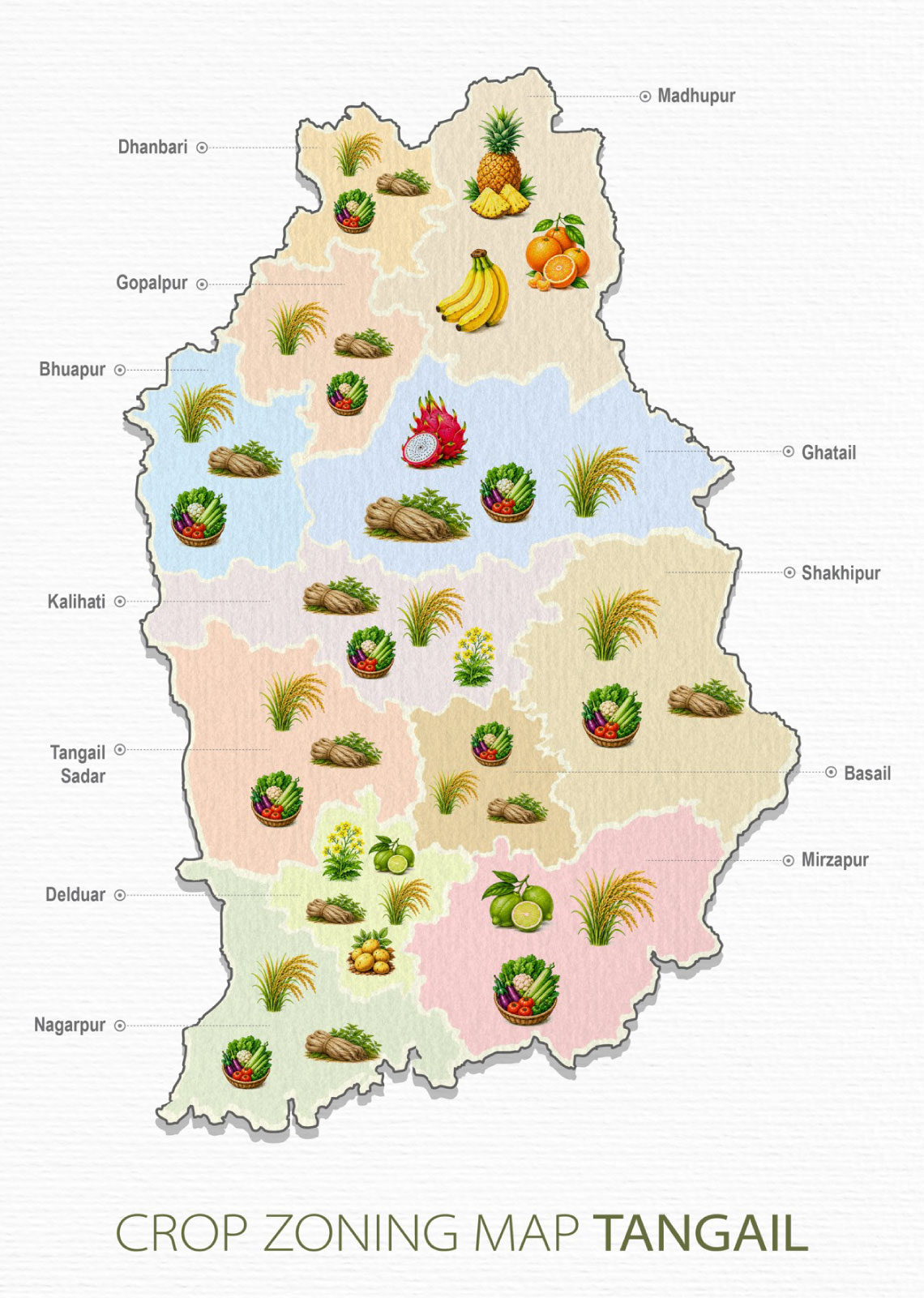

Members has a tenacity to invest in the agriculture sector, either directly in production or within the production value chain. This pattern of investment has created massive expansion in this sector. It has also led to a rise in the diverse field of borrowing and saving in various agricultural businesses and products, such as livestock fattening, aquaculture, and seed banking. This expansion has created an opportunity, especially for women, to invest financially in a sector that significantly contributes to the country’s economy. This directly contributes to food security and created income-generating opportunities for landless and marginalized farmers.

The agricultural crop map shows the diversity of agricultural products within Tangail where BURO’s members have actively invested.

These women did not read an investment textbook or roadmap. They built their own roadmap, decision by decision, with no advisor, no planning tool, and no institutional support.

BURO offered higher-tier deposit products as the savings capacity of the members grew, which shows the institution evolved alongside its members. However, some members seek alternative investment options for their surplus liquidity.

A member in Atia branch lost BDT 500,000 (~USD 4,748) to a fraudulent NGO. She lost this amount because she simply wanted higher returns on her savings. Our study document cases of institutions in Dewli branch that disappeared overnight and took hundreds of thousands of community savings with them.

Such instances are the predictable result of liquidity without a safe, trusted next step. Yet, these investments rarely follow a structured plan. Many households must navigate the process on their own, as market prices fluctuate, timing matters, and informal brokers sometimes step in. Members are ambitious, but they need a roadmap.

The branch staff recognizes this gap. In Pathorail branch, they called for investment advisory services, lifecycle-based products, and partnerships to help members transition from savings into productive assets. Focus group discussion with BURO staff revealed that savings volumes grow faster than available investment channels. This gap extends beyond BURO and reflects a broader market failure.

Shamim has worked at BURO’s Atia branch for two years. She notes, “Our members need support to transition from cash savings to productive investments.”

When savings mature, the formal market offers more of the same or products not built for these households. The informal market offers higher returns, but has no rules, no protection, and no accountability when things go wrong. Even through disruptions, such as COVID-19, members who had built savings buffers fared markedly better, and BURO’s support during those periods deepened trust.

Partnerships open a bigger opportunity. Members already invest in vehicles, solar panels, housing materials, aquacultures, and livestock. The question is whether they receive fair prices and protection when things go wrong. MFIs are positioned to act as a connector and guarantor of quality in asset finance. A partnership with a solar supplier or an electric vehicle (EV) manufacturer can help bridge the quality infrastructure gap with optional financing.

BURO’s field officers can do something valuable at scale through light-touch guidance. They can simply show up at contractual savings maturity with a one-page sheet that shows what similar members did with their money and the outcomes they achieved.

The pathways from saver to asset owner and from inclusion to security are not clearly laid out. Yet the members who need it are already there, saving and investing without a map and with savvy and sophistication. BURO’s long-term impact is evident in households that no longer depend on it. BURO’s measure of success is members who outgrow it. Success is measured by the share of members who move their accumulated savings into safer, higher-return assets without being cheated along the way. BURO has the data, the trust, and 35 years of proof that it can deliver.

Finally, a major financial decision many of these households make is to send a family member abroad. This requires an upfront investment of BDT 300,000 (~USD 2440) to BDT 1.8 million (~USD 14,641), with uncertain returns, and is typically the single largest capital outlay these households ever make.

The next blog in the series explores migration as a household investment and why finance arrives too late.

Written by

Ihsan Mahboob Hoq

Assistant Manager

Leave comments