Powering financial inclusion through data intelligence at local levels

by Saloni Gupta, Gayatri Pandey and Shrabasti Dhar

by Saloni Gupta, Gayatri Pandey and Shrabasti Dhar Apr 28, 2026

Apr 28, 2026 6 min

6 min

This blog examines gaps in current financial inclusion data systems and how they constrain local planning. It highlights the need for granular insights to enable more precise, evidence-based decision-making.

“Good data illuminates our world. It can make invisible markets visible.”

— Charles Marwa, Head, Monitoring and Evaluation, Alliance for Financial Inclusion

Ownership of a bank account is not the same as an active one. Access to digital payment infrastructure is not the same as consistent use of digital financial services. Yet ensuring that people engage regularly and meaningfully with these services is yet to be fully understood at the levels where it matters.

Over the past decade, India has expanded financial inclusion at scale. Account ownership increased from 35% in 2011 to nearly 89% by 2024. Large-scale initiatives, such as the Pradhan Mantri Jan Dhan Yojana (PMJDY), supported this growth, under which more than 573 million accounts have been opened till December 2025.

The rapid growth of digital financial infrastructure has complemented this expansion. The Unified Payments Interface (UPI) now accounts for around 49% of the volume of real-time payment system transactions worldwide.

As of 2025, enrolments under the Pradhan Mantri Suraksha Bima Yojana (PMSBY) reached 440.9 million, while the Atal Pension Yojana (APY) reached 65.64 million subscribers. At the national level, these trends signal considerable progress in extending the reach of the formal financial system.

With financial access now widespread, the policy focus has shifted from access to usage. While existing systems capture significant granularity, this rarely surfaces in forms that support local decision-making. Opening accounts or enrolling beneficiaries does not ensure meaningful use, underscoring the need for timely, granular data on usage patterns to inform planning at district and sub-district levels.

India has a wide array of dashboards and reporting systems tracking financial inclusion across banking, payments, and social security programs, but their usefulness for planning depends on what they present and what remains unavailable at the levels where implementation decisions are made. Evidence-led local planning requires a clear understanding of the strengths and limitations of current financial inclusion (FI) data.

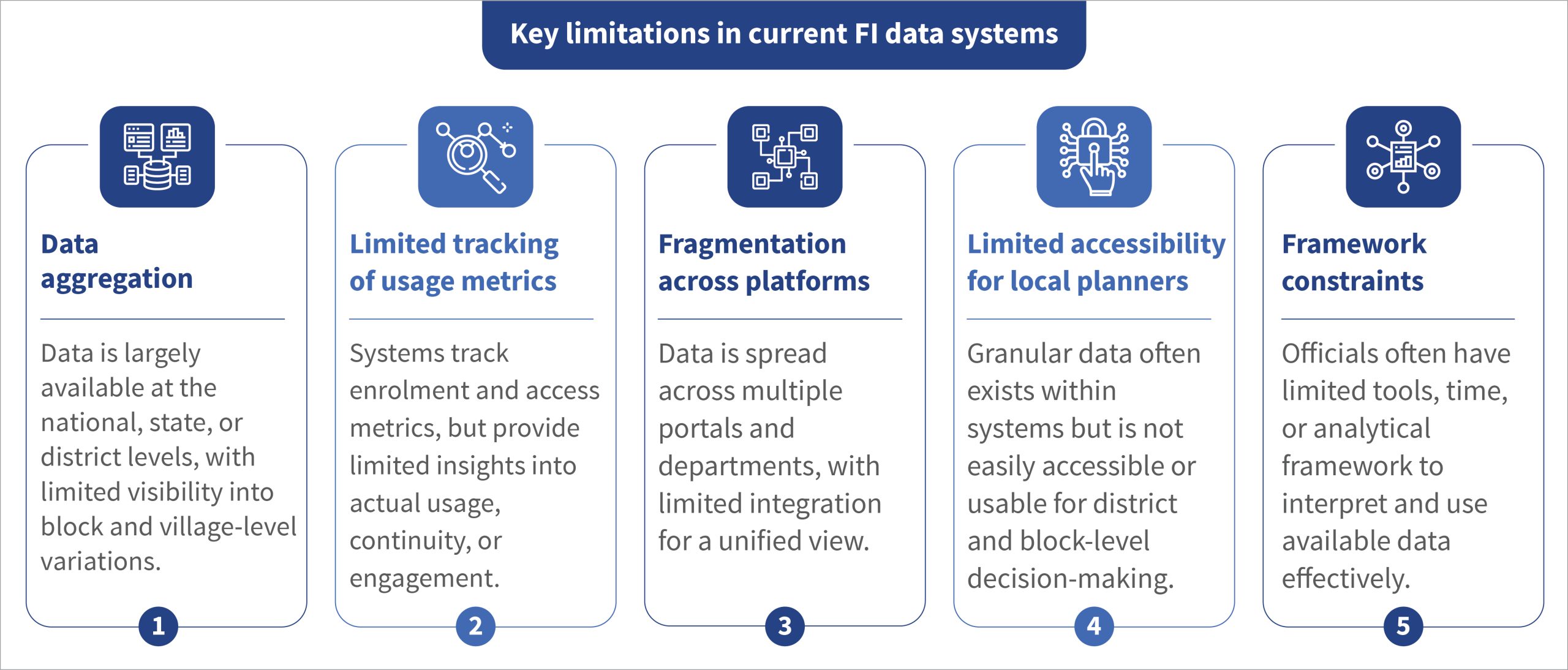

Where existing FI data systems fall short for local planning

India’s financial inclusion architecture generates large volumes of data across banking, payments, and social security programs. Yet, structural challenges limit how effectively this data informs local planning. While data may be available in many cases, constraints often lie in how granular information is aggregated, presented, and used across different levels of governance.

A primary limitation is the continued reliance on highly aggregated FI data. The Lead District Manager(LDM),as the nodal point for financial inclusion at the district level as per the RBI’s Lead Bank Scheme, anchors district-level FI monitoring and planning.

The LDM typically receives data aggregated at the district level for review and upward reporting. The system offers limited or inconsistent disaggregation by block, gram panchayat, or demographic characteristics, such as gender, age, or occupation. While more granular data may be captured within implementing systems, or in select geographies, systems do not routinely present it in formats that support sub-district analysis. As a result, planning often relies on averages, even in contexts where local conditions may differ sharply.

Limited visibility of usage as a distinct dimension of financial inclusion. While the systems consistently track access and enrolment indicators, information on how financial services are actually used remains uneven. Usage data has begun to be tracked across parts of the system, but definitions, indicators, and reporting practices vary across programs and geographies. For instance, in states, such as Assam, State Level Banking Committees (SLBCs) have begun to track renewals under the PMJJBY and the PMSBY, while in Madhya Pradesh, the MP SLBC has started to report indicators related to digital transaction volumes.

Yet, these efforts are not standardized. Even where transaction data is available, systems often present it in aggregate form. As a result, planners cannot identify variation in usage intensity, frequency, or purpose at the block or gram panchayat level, and thus cannot distinguish between nominal account ownership and active usage.

Gaps between where systems hold FI data and who can use it for plans further compound these challenges. The large volumes of granular data that exist across financial service providers and government systems are not always accessible to district- or block-level planners, while public systems often share data primarily for reporting purposes, it has limited use for analysis. Our work across aspirational blocks also shows that local authorities sometimes aggregate FI data across different parameters, primarily for reporting purposes, which further limits its usefulness for planning.

In addition, FI data exists across multiple platforms and departments, with limited interoperability. Different agencies maintain program-specific datasets through distinct formats and reporting structures. Platforms, such as Champions of Change, provide granular information on select indicators with a focus on aspirational districts and blocks, while portals, such as the PMJDY dashboard, focus primarily on scheme-specific uptake. While each system serves a specific purpose, greater integration across platforms could enhance their combined use for holistic planning.

Finally, the capacity to analyze and use available data is limited at the local level. Even where disaggregated data is available, officials may face constraints related to analytical skills, time, or access to user-friendly tools. Systems often present data in formats that officials cannot interpret easily for routine decision-making. This limits its integration into planning processes, such as district consultative committees (DCCs) or block-level reviews. These capacity constraints further reduce the practical value of existing FI data to strengthen usage on the ground.

Turning data into actionable insights to support local planning

India’s FI data systems have matured significantly. These now provide greater visibility into access and enrolment across schemes and geographies. As the focus shifts toward usage, continuity, and quality of services, the opportunity now is to strengthen how existing data supports decision-making at the district and block levels. These systems do not need to be built anew, but need a clearer focus on how these are organized and used.

The following areas highlight where focused improvements in data use can enhance local planning and implementation meaningfully.

- Create a planning-oriented view at the district level using block-level data: District administrations require consolidated view of FI indicators across access and usage, disaggregated to the block level, to support decision-making. Simple analytical tools, including AI-enabled dashboards, can combine indicators such as account activity, digital transactions, insurance renewals, and pension contributions into a single view. This will enable them to identify specific gaps and move away from uniform approaches to focus facilitation efforts.

- Shift the focus from enrolment to sustained usage and continuity: With increased access, the need of the hour is to review usage and continuity indicators, such as account activity, scheme renewals, contribution regularity, and claims settlement. This review provides a clearer picture of financial inclusion outcomes and helps local administrations better understand whether gaps relate to access, service delivery, or user confidence.

- Interpret local data using simple and relevant population benchmarks: Administrations could interpret enrolment and usage data against basic population benchmarks, such as adult population, SHG households, or farmer households. This approach enables a more accurate assessment of coverage levels at the block level. It also helps distinguish between areas nearing saturation and those with meaningful gaps to support better prioritization of local actions.

- Strengthen local capacity to interpret and use financial inclusion data: As data becomes more granular and planning-oriented, district and block administrations require the ability to interpret trends, identify gaps, and decide suitable responses. This includes building familiarity with AI-supported analytics and other user-friendly tools to translate data into actionable insights within routine review processes. If officials strengthen this capacity, they can help ensure that improved data availability translates into better planning decisions.

These recommendations highlight a clear direction. Financial inclusion efforts should move from tracking access to enabling informed intervention. As these systems continue to evolve, the real opportunity lies in bridging the gap between data availability and its use in planning. These steps are aimed to ensure that financial inclusion translates into meaningful and sustained outcomes on the ground.

Leave comments