Training, Monitoring & Support – Necessary Or An Opportunity To Cut Costs?

by Graham Wright

by Graham Wright Oct 13, 2015

Oct 13, 2015 4 min

4 min

The author explains whether agent training, monitoring & support is necessary or an opportunity to cut costs for mobile network operators.

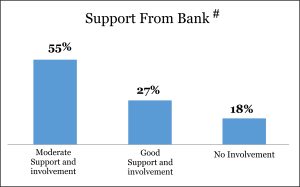

While only 27% of agent network managers receive good support and involvement from the banks for which they are providing services, another 55% do say that they receive moderate support, as per MicroSave’s recent State of the Industry Report 2015 on India note. The India 2015 ANA survey results enable us to understand this further by highlighting important differences across the different types of service providers.

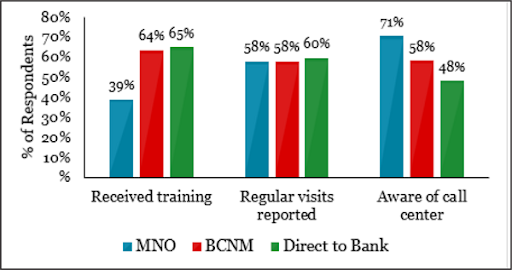

Perhaps unsurprisingly, MNOs show a higher use of call centres to support their agents – but sadly, deliver training to a much smaller proportion of them. This is evident from the fact that by and large, a much smaller proportion (59%) of Indian agents are trained than in other countries: Pakistan (62%) Bangladesh (68%), Kenya (92%), Tanzania (79%), and Uganda (94%). Of the 59% trained in India, 61% agents have undergone a refresher training. 36% of these have received refresher training only once.

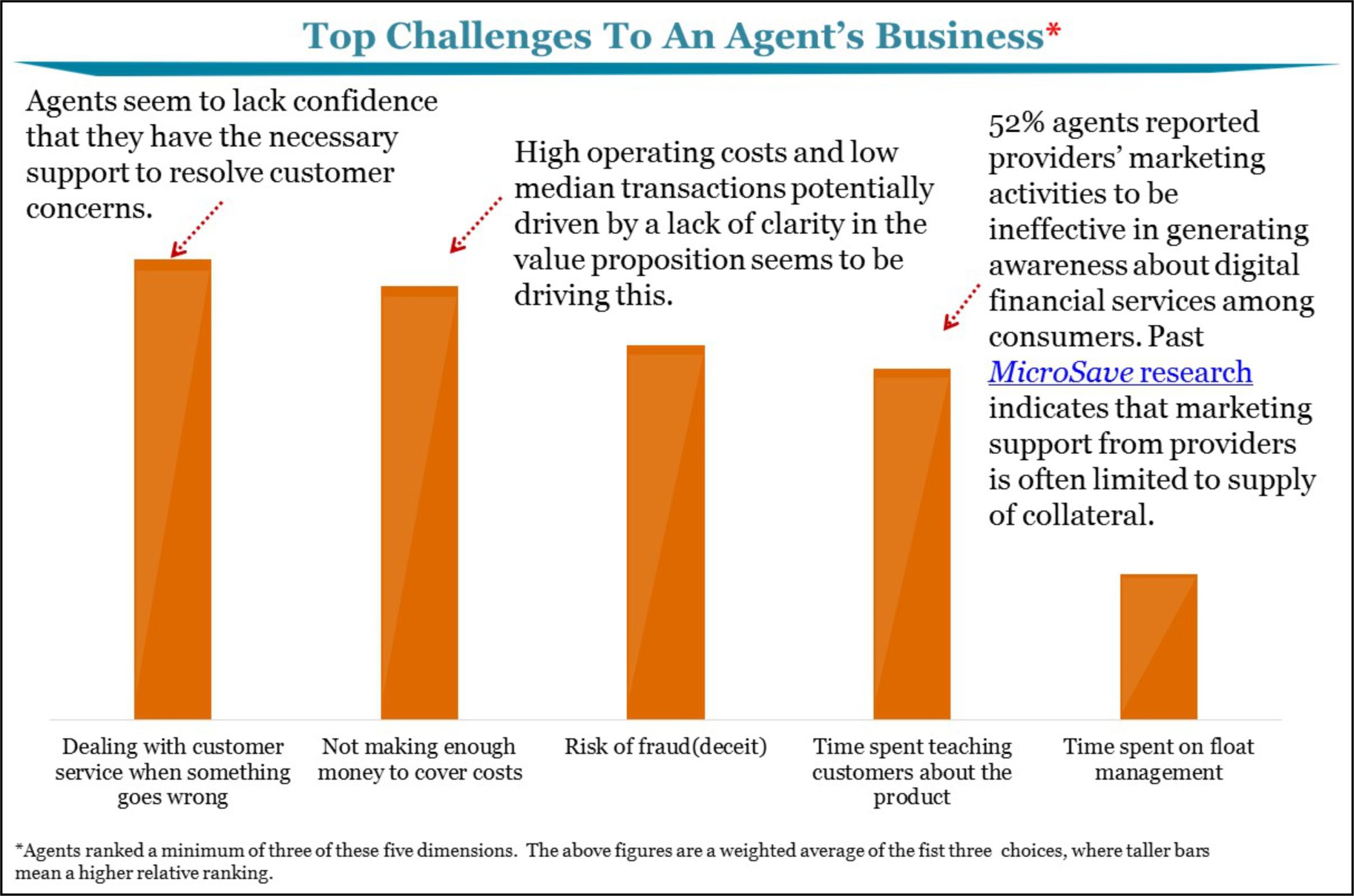

Indian agents also receive less monitoring/support visits than their counterparts in other countries. 58% of Indian agents reported regular visits (in contrast to 68% reported in major cities). The comparable percentages in other ANA countries are: Bangladesh (69%), Pakistan (76%), Kenya II (86%) Tanzania (76%) and Uganda (33%). Of those agents who received a visit, 60% were visited at least monthly and 32% reported ‘no fixed frequency’ of visits. All this matters enormously because the ANA survey highlighted that agents’ biggest perceived challenge was to “deal with customer service when something goes wrong”. If they were adequately trained, monitored and supported (on-site and through call centres), agents would be more confident about their ability to serve their customers – and (one reckons) things would “go wrong” less often.

Indian agents also receive less monitoring/support visits than their counterparts in other countries. 58% of Indian agents reported regular visits (in contrast to 68% reported in major cities). The comparable percentages in other ANA countries are: Bangladesh (69%), Pakistan (76%), Kenya II (86%) Tanzania (76%) and Uganda (33%). Of those agents who received a visit, 60% were visited at least monthly and 32% reported ‘no fixed frequency’ of visits. All this matters enormously because the ANA survey highlighted that agents’ biggest perceived challenge was to “deal with customer service when something goes wrong”. If they were adequately trained, monitored and supported (on-site and through call centres), agents would be more confident about their ability to serve their customers – and (one reckons) things would “go wrong” less often.

Furthermore, an elegant study by The Helix Institute and Harvard Business School revealed that, “Agents who are more transparent with their pricing and more knowledgeable about mobile money policies experience significantly higher transaction demand than their less transparent and less expert peers. More knowledgeable agents also experience an even greater increase in demand when there are competing agents nearby.” So, the quality of service matters and directly affects agents’ ability to build trust and grow their business. Indeed, the study concludes, “the ability to answer a difficult question about mobile money policy increases demand by over 10%. … The implications of this work to mobile money operators and agents are clear: service quality is critical to a healthy agency.”

Furthermore, an elegant study by The Helix Institute and Harvard Business School revealed that, “Agents who are more transparent with their pricing and more knowledgeable about mobile money policies experience significantly higher transaction demand than their less transparent and less expert peers. More knowledgeable agents also experience an even greater increase in demand when there are competing agents nearby.” So, the quality of service matters and directly affects agents’ ability to build trust and grow their business. Indeed, the study concludes, “the ability to answer a difficult question about mobile money policy increases demand by over 10%. … The implications of this work to mobile money operators and agents are clear: service quality is critical to a healthy agency.”

Regular monitoring and support visits are essential to ensure that agents’ outlets are complaint in terms of branding, transparent pricing, liquidity balances and transaction processing. Similarly, training (as well as monitoring and support visits) is the foundation for creating confident, knowledgeable and thus trustworthy agents that are both capable of, and interested in, delivering high quality digital financial services. And, as we have seen in multiple countries, trust is a key determinant of levels of uptake and usage of digital financial services.

Agent network managers in India seek improvements in two key areas from the banks they serve. The first, perhaps unsurprisingly, is the level of commission they are paid. The second is that of the marketing support they receive.

Agent network managers in India seek improvements in two key areas from the banks they serve. The first, perhaps unsurprisingly, is the level of commission they are paid. The second is that of the marketing support they receive.

When MicroSave conducted the State of the Industry survey in 2012, most of the agent network managers were dependent on banks for marketing – in 2015, most are responsible for marketing and communication themselves. Thus, the burden of promoting digital financial services largely falls on the shoulders of agents and their network managers. As a consequence, they use a variety of exclusively below the line approaches to promote uptake and usage of their services.

Naturally, agent network managers have a series of “asks” of the banks:

• Share marketing & communication, and customer enrolment campaign expenses.

• Co-brand marketing collaterals.

• Design and run financial education campaigns for customers to increase awareness of banking products amongst and build trust that customers place in agents and the digital finance model.

• Provide ID cards and certificates of association to agents with bank logo and signature to increase the perception of legitmacy amongst customers and gain their trust.

• Create special queues for agents at bank branches (as privileged customers or DSA), as currently they have to stand in the same lines as customers to meet their liquidity requirements, which limits their availability for end customers.

Additional appropriate and necessary “asks” that we, at MicroSave recommend, are:

• Make agent performance a key performance evaluation criteria for bank branches to which these agents are linked, and by which they should be serviced/supported.

• Enhance both above and below the line marketing in support of agent banking and the opportunities it provides to rural communities.

With the advent of payment banks, it will be in the interest of the commercial banks that these agent network managers are responded positively to these modest requests.

Written by

Leave comments