Digital convenience: New ways for India’s MFI borrowers to repay loans

by Vivek Anand, Pramiti Lonkar, David Mathew and Disha Bhavnani

by Vivek Anand, Pramiti Lonkar, David Mathew and Disha Bhavnani Jun 26, 2025

Jun 26, 2025 5 min

5 min

New digital repayment solutions are easing loan repayments for India’s MFI borrowers. Tailored tools and collaboration are helping women like Reena, Seema, and Asha transition from cash to digital.

Millions of women across India rely on loans from microfinance institutions (MFIs) to support their livelihoods, manage small businesses, and fund essential household needs. While most MFIs have digitized loan disbursements, the vast majority of repayments—nearly 87% as of FY 2021-22—still occur in cash. This reliance on cash makes borrowers’ lives difficult every day.

Take Reena, for example. A factory worker in Bengal, Reena must carve time out of her hectic schedule to withdraw her banked salary to pay her loan for house repairs. Grocery store owner Seema’s story has a similar ring. Hailing from a small village in Bihar, Seema has an irregular income and often relies on her husband for financial support. However, even if she wishes to access her loan repayment details to update him, Seema must first deal with a cumbersome offline process.

Meanwhile, in the southern state of Kerala, fish vendor Asha uses a basic phone. She constantly worries about carrying cash to repay her business loan, which remains a common challenge among borrowers who lack access to digital EMI payments.

Across India, more than 83 million MFI borrowers have a similar story to tell. Despite the clear advantages of digital transactions and the efforts of MFIs to introduce solutions, the shift away from cash repayments is yet to pick up pace.

Several factors contribute to the persistence of cash. Many digital solutions fail to align with the varying technical capabilities and trust levels of a diverse borrower base. Additionally, several borrowers use basic phones or are new to digital platforms, which causes a potential mismatch between the borrowers’ requirements and the solutions’ design. Moreover, the integration of digital payment systems with the MFIs’ existing loan management infrastructure has proved . It involves multiple stakeholders, incompatible software that hinders easy integration across players, and high costs. It calls for substantial technical investment and efforts to achieve a suitable technology fit for the MFI’s systems.

The combination of such issues explains why borrowers continue to rely on traditional cash collections. Existing digital payment options frequently do not suit them. If MFIs wish to scale up digital payments, they must offer customized solutions that consider borrowers’ preferences, levels of digital readiness, and awareness.

The Microfinance Industry Network (MFIN) recognized these challenges alongside the need for tailored approaches and partnered with MSC in 2022. This partnership sought to address the barriers to the adoption of digital repayment solutions and digitize repayments at scale. As part of this initiative, MSC conducted an in-depth study with nine partner MFIs of the MFIN. The study sought to identify tailored digital repayment solutions aligned with each institution’s capabilities and their borrowers’ specific needs.

The study revealed critical insights. While smartphone ownership and internet connectivity are on the rise, borrowers’ ability and willingness to repay digitally vary widely based on awareness, skills, and comfort with technology. Although most borrowers know about digital methods, many lack the literacy to use them independently. Only 24% of borrowers reported using their phones for payments. Even those who use digital payments elsewhere strongly prefer cash. Safety concerns also further discourage borrowers with limited digital exposure.

MSC designed a framework to overcome these barriers that accounts for MFI readiness, cost implications, borrower access, ease of use, and safety. Based on this framework, we recommended tailored solutions and emphasized multitier training programs for MFI staff and borrowers. We share key insights from the study and highlight the solutions implemented across partner MFIs.

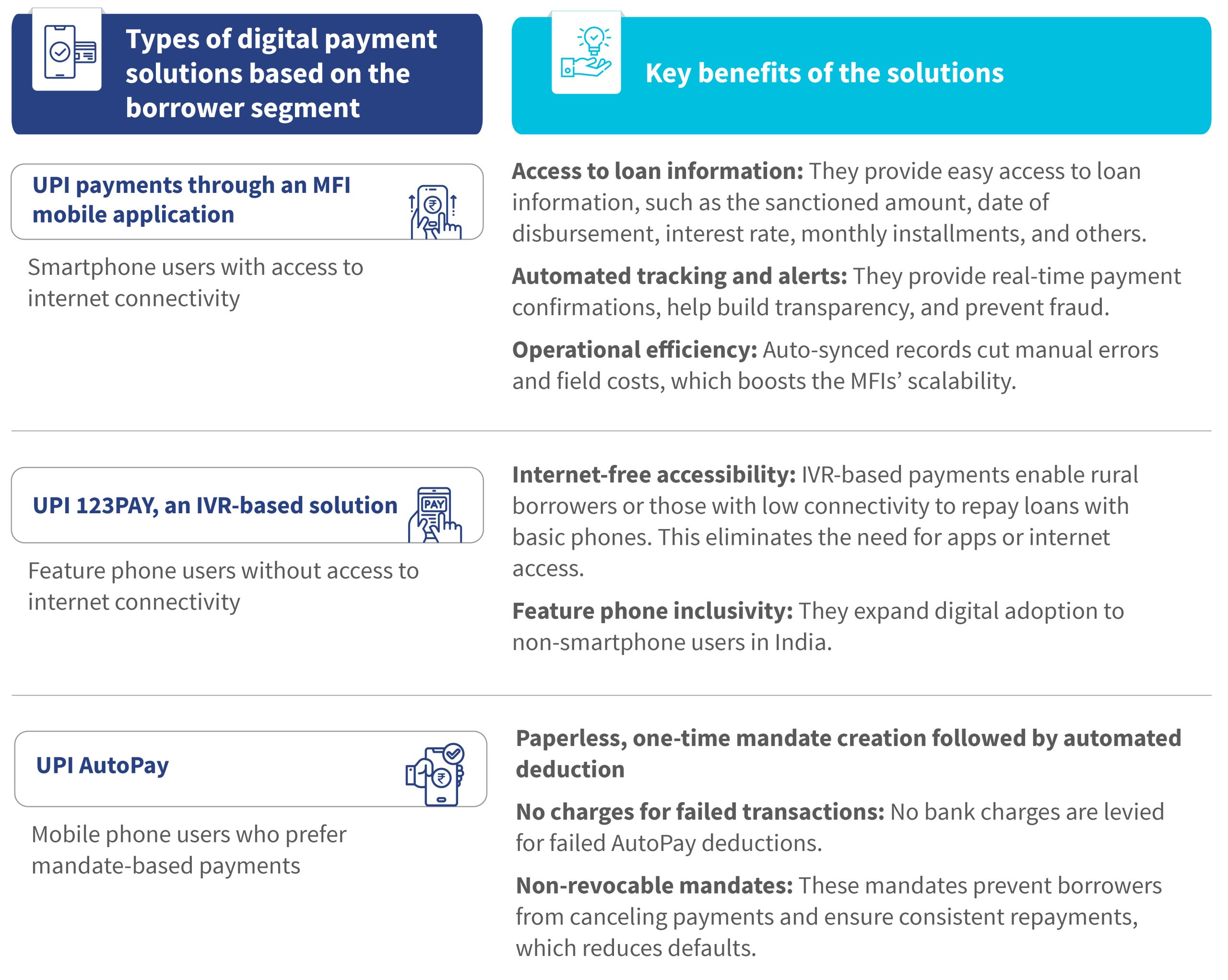

Based on the assessment and framework, the project focused on implementing key digital payment solutions tailored to borrowers’ varying needs. The partner MFIs implemented three leading solutions:

- UPI payments via MFI mobile applications:Research showed that borrowers trust mobile apps developed by their own MFI. The MFIN sought to meet this preference and engaged FinTech partners to create customized mobile applications for each participating MFI.

- UPI 123PAY IVR-based solution:MFIN recognized that 34% of borrowers use feature phones. It introduced a dedicated IVR number for each institution and integrated it with the MFI system to allow borrowers to repay digitally without a smartphone.

- UPI AutoPay:Targeted to borrowers who seek convenience, this option allows automatic, recurring EMI deductions without manual initiation or PIN entry each time.

Such tailored solutions directly addressed the challenges of borrowers like Reena, Seema, and Asha. Thanks to UPI AutoPay, Reena no longer needs to take time off work to withdraw cash. Her EMI is automatically deducted from her savings bank account, which has freed up valuable time and effort. Seema benefited from the MFI’s mobile application, which gave her easy access to up-to-date loan repayment information. This allowed her husband to conveniently view her loan account details on the app and digitally pay the EMI as per the schedule. Meanwhile, basic phone user Asha used UPI 123PAY as a safe and accessible way to pay her loan installments digitally, which eliminated the risks associated with carrying cash for repayments.

The initiatives introduced through this project showed notable results. Digital repayments increased to 30% of all repayments across the pilot branches. Beyond individual impact, the adoption of digital payments streamlined MFIs’ collection processes as well, which freed up staff’s time and resources for loan sourcing and other services.

Such operational improvements are especially valuable given the way MFIs structure their lending. Typically, MFIs rely on joint liability groups—small groups of female borrowers who come together to access loans and support each other’s repayment efforts. These groups promote financial discipline, mutual accountability, and social support to help women build credit histories and strengthen their economic resilience.

Center meetings, which are regular gatherings of these groups, have shifted their focus away from cash transactions to build awareness and encourage the use of additional financial services. Digital repayments also create a transparent transaction history to benefit borrowers. They help borrowers track finances, demonstrate repayment capacity, and potentially uncover greater financial opportunities.

This initiative’s success offers several key lessons for the microfinance sector:

- Custom solutions drive adoption: Digital tools tailored to MFI operations and local context lead to higher adoption.

- Integration with existing systems is essential: Solutions are most effective when they fit seamlessly into staff routines and technology infrastructure, build trust, and save time.

- Collaboration is vital to encourage digital adoption: Since the initial demand from borrowers may be low, MFIs must proactively build awareness among both staff and borrowers. A collaborative approach nurtures sustainable adoption.

While India’s microfinance sector moves toward digitization, the experiences of borrowers, such as Reena, Seema, and Asha, shine a harsh spotlight on the persistent challenges they face as they try to break free from their dependency on cash for repayments. While this project shows that tailored approaches and focused training can boost adoption, gaps in digital readiness remain a major barrier.

If MFIs are to overcome this hurdle, they must urgently prioritize the development of user-friendly and seamlessly integrated digital repayment tools. Stakeholders must invest substantially to build the digital capacity of staff and clients. Meanwhile, MFIs, FinTech partners, and policymakers must take intense collaborative action to address fundamental infrastructure and literacy barriers and ensure digital systems are both accessible and secure.

Only evidence-based, collective effort will allow the sector to revolutionize repayment processes, deepen financial inclusion, and unlock greater opportunities for the countless Reenas, Seemas, and Ashas across India. We look forward to sharing deeper insights from our ongoing engagement with MFIN to digitize MFI repayments. Watch this space for more details on our lessons and impact as the work progresses.

Written by

Vivek Anand

Financial consultant

David Mathew

Associate, Digital Financial Services - Payments and Distribution

Leave comments