Cross-border payments in Africa: What is changing and why it matters

by Njeri Macharia and Jackson Kamau

by Njeri Macharia and Jackson Kamau Jul 9, 2025

Jul 9, 2025 5 min

5 min

Cross-border payments are the economic backbone of Africa, yet high costs, inefficiencies, and exclusion persist. This blog explores the shift from informal systems to digital innovations like PAPSS, and outlines the reforms needed for inclusive, intra-African trade.

The landscape of cross-border payments

Njeri, 34, is a small entrepreneur in Kenya who sells garments and needs to pay a supplier in Uganda. On the southern tip of the continent lives Jackson, a 40-year-old South Africa-based diaspora member who needs to send funds back home to his family in Ghana. In Africa, such cross-border transactions are more than a mere exchange of funds across nations. They serve as the vital lifeblood of entire economies that support millions of people who live, work, hope, and dream across geographies.

Yet these hard-working people must struggle with high costs, slow processes, and limited access to reliable, affordable, and readily available cross-border payment solutions, which hinder trade and stifle economic growth. The market faces several challenges, which include high remittance costs of 7.4% to 8.3%, regulatory fragmentation, foreign exchange liquidity issues that cause USD 5 billion in annual losses, and a continued reliance on offshore USD/EUR clearance that increases transaction costs.

Despite these setbacks, a glimmer of hope has emerged in the steady transformation of cross-border payments across Africa. As of 2025, the market is worth approximately USD 329 billion. It is projected to triple to USD 1 trillion by 2035, driven by FinTech innovation, the rise of mobile money, and increased intra-African trade. This expansion translates to a compound annual growth rate (CAGR) of about 12%.

Mobile money platforms are central to this growth. In 2022, they processed USD 837 billion in transactions globally, with Africa responsible for 66% of the volume. These platforms offer significantly lower fees than traditional banks, with rates that range from 1.5% to 3%. But for us to understand the landscape better, we must take a look back in time.

A shift from informal to structured systems

Cross-border payments in Africa began in pre-colonial times through vital yet informal networks that physically moved funds. These early systems were often unreliable, insecure, and slow, which were among the gaps that formal banks eventually addressed. Despite the emergence of formal banks, small-scale and informal traders continued to rely on physical cash. They chose it not because it was safe, but because it was the most direct and accessible option.

Things changed when the introduction of traditional banking systems formalized cross-border payments. Commercial banks enabled secure international transactions through services, such as bank transfers, SWIFT wires, and card payments. These systems supported high-value and corporate trade but remained inaccessible and inefficient. Further, banks continued to be costly, with average fees that exceed 11% per transactionlengthy process times, and limited access for people who need funds. Low financial inclusion further limited access, as only 49% of Sub-Sahara Africans had bank accounts as of 2021. This left vast portions of the population excluded from formal financial systems.

The present: A digital transformation

Today, Africa is witnessing a profound digital transformation in cross-border payments that directly addresses historical inefficiencies. With our multi-decade-old roots deep within the continent, MicroSave Consulting (MSC) continues to uncover a deep understanding of user needs through extensive research and solutions to meet these needs.

With the Mastercard Foundation, our demand analysis in Côte d’Ivoire, Mali, and Senegal revealed how migrant families depend on informal channels as they lack tailored financial services. Based on this research, we recommend human-centered, remittance-linked digital financial services (DFS) to support last-mile use and adoption, especially for low-value, frequent transactions. Our work in India, the Philippines, and West Africa further emphasizes the need for stakeholders to understand migrant behavior and design inclusive payment corridors.

When we move back to Kenya, we see Kenya Commercial Bank (KCB) and Equity Bank have produced KCB Connect and Equity Direct to offer faster and more affordable regional transfers. They reduce dependency on banking and offer competitive forex rates. Outside Kenya, top-tier banks, such as Nigeria’s Zenith Bank and Ecobank, use specialized trade finance solutions and multi-currency accounts to simplify cross-border businesses.

Meanwhile, money transfer operators (MTOs), such as Western Union, offer speed but at high fees. Mobile money platforms, such as M-PESA Global, have revolutionized peer-to-peer (P2P) remittances and guarantee direct mobile-to-mobile transfers. Providers have successfully addressed fragmented networks and interoperability by forging extensive partnerships with other mobile money operators and banks, often leveraging global payment hubs and standardized APIs to connect disparate systems.

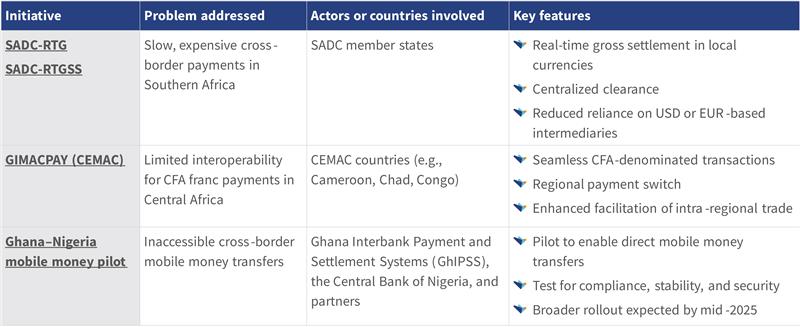

Regional payment systems further enhance efficiency and solve long-overdue payment challenges.

In 2022, the African Export-Import Bank (Afreximbank) and the African Union launched the Pan-African Payment and Settlement System (PAPSS). It provides breakthrough infrastructure for instant, secure cross-border transactions in local African currencies, a significant advancement that directly connects African currencies and bypasses traditional reliance on intermediary foreign exchange. The distributed ledger technology (DLT) in PAPSS eliminates the need for intermediary currencies, such as the USD or Euro. It reduces transaction costs by up to 50% and settlement times from days to seconds. DLT also enhances transparency through real-time tracking and anti-fraud protocols.

By early 2025, PAPSS had enabled real-time cross-border payments across 17 countries, connecting 14 national switches and over 150 commercial banks. This growth aligns with the African Continental Free Trade Area (AfCFTA) goals and positions the PAPSS as a vital part of intra-African trade, which is expected to increase from 18% to 50% annually by 2030. Recent innovations, such as the integration of PAPSS into mobile banking apps for small and medium enterprises and diaspora remittance corridors, further democratize access to Africa’s integrated financial future.

Yet, challenges persist

Despite significant gains, Africa’s cross-border digitization has yet to solve key challenges. Providers struggle to align frameworks, which block smooth interoperability, especially in regions without unified KYC rules, anti-money laundering (AML) measures, and consumer protection. Foreign exchange shortages and dependence on offshore clearance raise costs and slow transactions.

Moreover, users in rural areas cannot access last-mile infrastructure due to scarce mobile money agents and cash shortages. Many consumers are unaware of new cross-border solutions or lack the digital skills to use them. Remittance costs in Africa average 7.4%, exceed global targets, and limit affordable options for frequent, low-value transfers. This situation spells a need for expanded access. These gaps underscore a need for regulatory coherence, expanded access, and user-centric design to unlock the potential of Africa’s payment system.

Regulatory reforms as the way ahead

The regulation of domestic infrastructure, the introduction of national switches, and their integration to enable efficient, low-cost, and inclusive systems are essential for cross-border payments in Africa. Countries must connect national switches, such as Tanzania’s TIPS and Rwanda’s RSwitch, to the PAPSS and standardize AML/KYC regulations. This will improve interoperable digital infrastructure and promote local currency settlement.

MSC’s work in cross-border payments in India, the Philippines, and West Africa emphasizes the need to understand migrant user behavior, the risks of informal channels, and design human-centric products. These lessons will prove valuable for inclusive payment corridors under the AfCFTA.

Central banks, governments, FinTechs, and regional bodies must work together to uncover Africa’s payments potential worth USD 1 trillion by 2035. An increased focus on digital literacy and inclusion will reduce costs, boost transparency, and open the doors to Africa’s integrated and prosperous financial future.

Leave comments