A race against cyber threats: Biometric adoption in Southeast Asia’s banking sector

by Disha Bhavnani and Ha-Trang Nguyen

by Disha Bhavnani and Ha-Trang Nguyen Jul 10, 2025

Jul 10, 2025 4 min

4 min

Cyber fraud in Southeast Asia is surging, costing billions annually. Traditional authentication methods are failing against evolving threats. To counter this, governments and banks are increasingly adopting biometric authentication to secure digital finance and promote financial inclusion.

An older man in Vietnam from a low-income background lost his entire pension due to a fraud that has become all too common in the developing world. He received a call from someone who had posed as a bank employee and asked the older man to share his OTP over the phone. He fell for the scammer’s pitch and soon, his precious pension vanished from his bank account.

Cyber scams now generate more than USD 43.8 billion annually across Southeast Asia. As digital finance proliferates, cybercriminals are now more advanced. They use tools, such as artificial intelligence (AI), deepfakes, large language models (LLMs), and malware to steal data, impersonate individuals, and bypass security systems. In response, banks across the region have raced to adopt biometric authentication. Banks now use customers’ fingerprints, faces, or voices to verify identity and to protect against these evolving cyber threats.

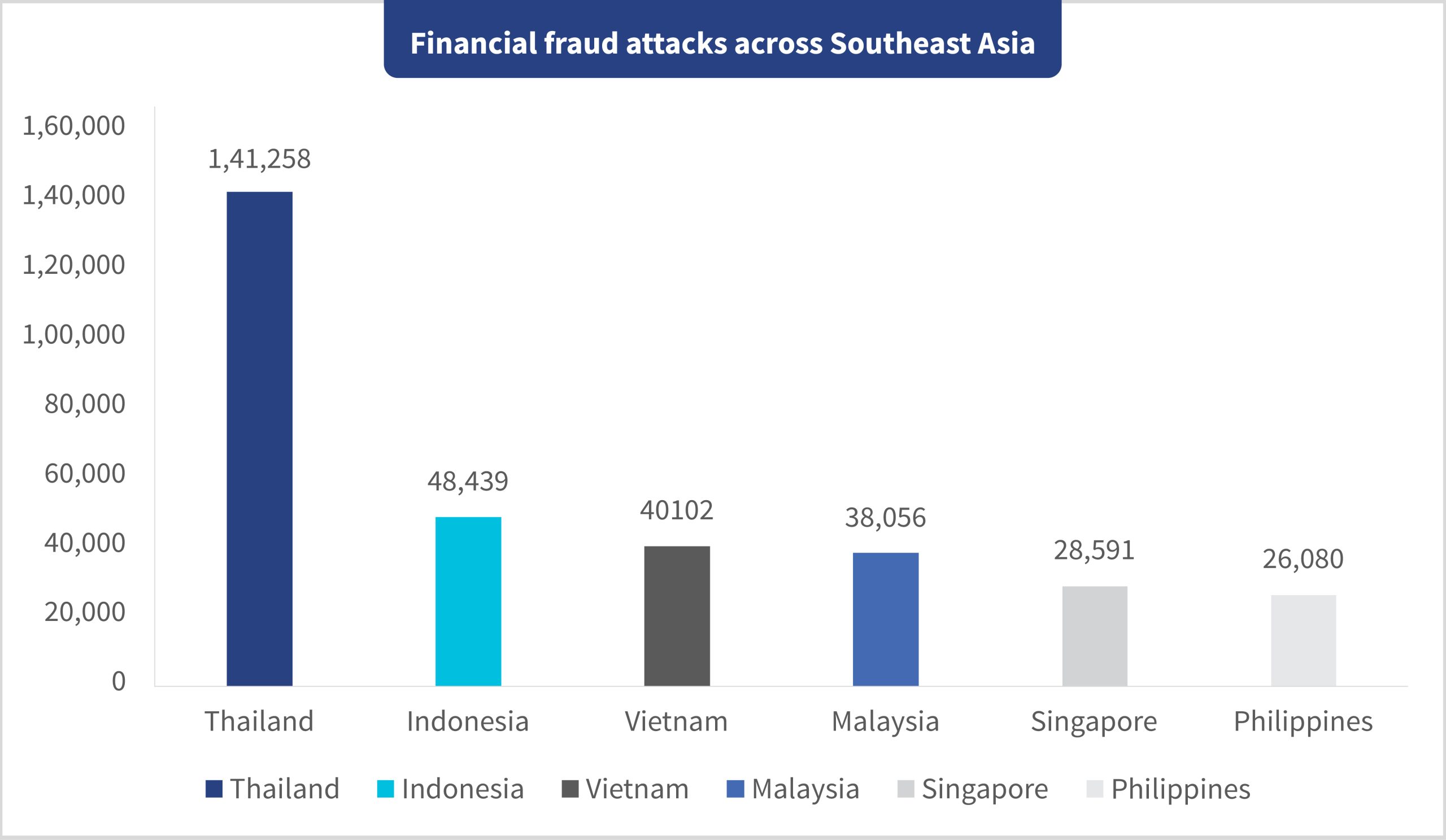

Online financial fraud has surged across Southeast Asia in recent years. In 2024 alone, Thailand recorded more than 14,000 cases, which makes it a regional hotspot, followed by Indonesia with 48,000. Thailand’s high rates of fraud stem from low public cyber awareness and scam operations in neighboring countries, such as Cambodia, Lao PDR, and Myanmar. Scammers have started to use smart devices and sophisticated tactics widely, which escalates the issue.

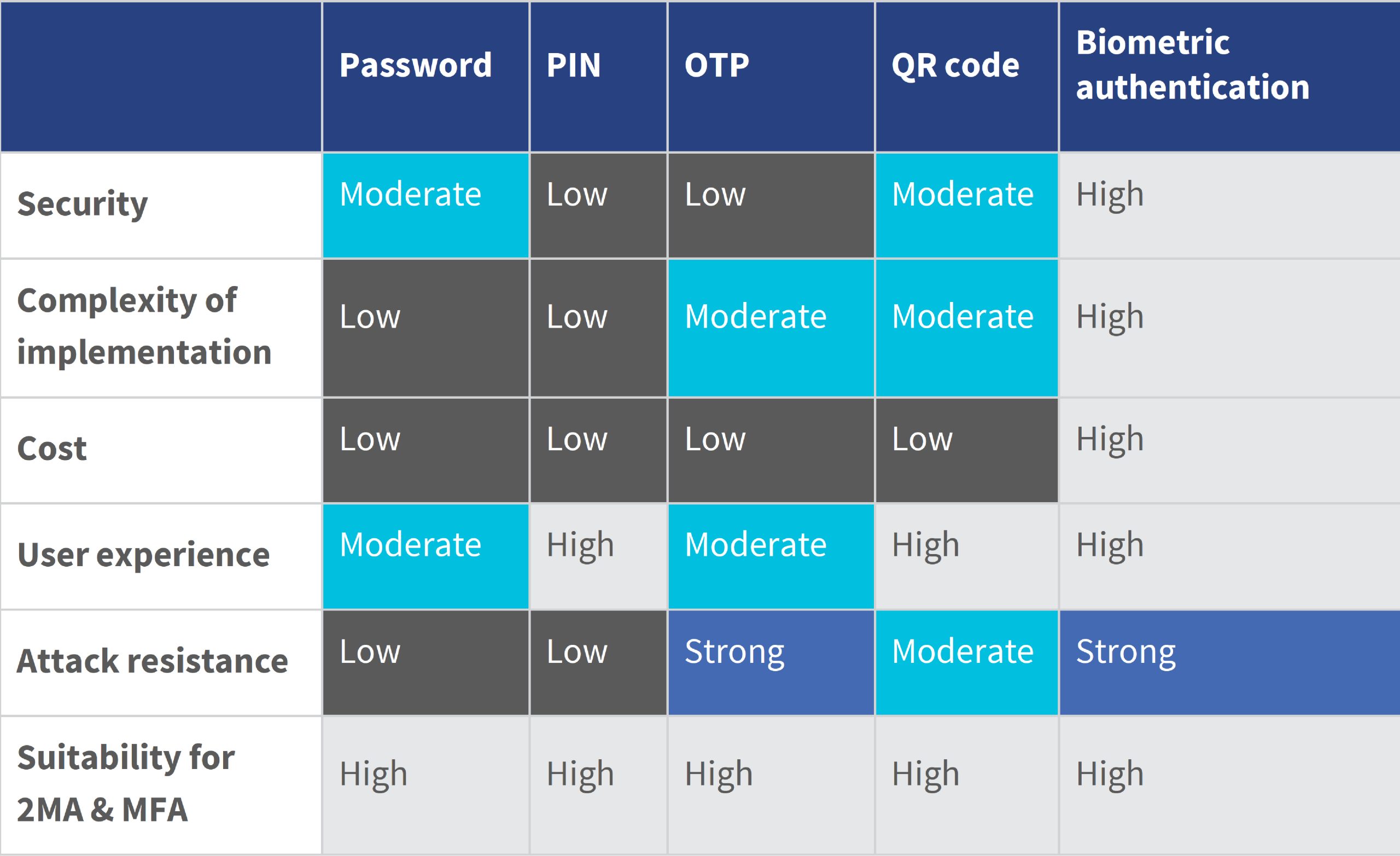

Southeast Asian countries have taken measures to safeguard their citizens against cyber fraud, particularly in finance, which is a primary target sector. In response, financial institutions and FinTech companies have adopted advanced methods to authenticate customers and ensure secure services. However, traditional authentication methods still face limitations. Passwords, which are one of the standard knowledge-based authentication (KBA) methods, are often reused and forgotten by users. This exposes users to phishing or data breaches that increase cybercrime risks and user friction. Cyber attackers can manipulate PIN codes through simple methods, such as social engineering.

Meanwhile, possession-based authentication (PBA) methods, such as SMS-based OTPs, are easy to deploy but vulnerable to SIM-swapping. Similarly, QR code authentication poses risks as bad actors can copy or tamper with them. It relies on a separate scanning device and often fails in poor environmental conditions, such as low lighting.

Biometrics-based authentication has addressed the shortcomings of traditional security solutions and has emerged as a more reliable and secure technology in recent years.

Biometric authentication verifies an individual’s identity through unique biological characteristics, such as fingerprints or facial features. Unlike passwords, biometric data is complex to imitate and not subject to human errors, such as forgotten passwords. Many banks now combine biometrics with other verification procedures to establish a multi-factor authentication (MFA) system, which improves customers’ experience and strengthens digital security.

Across Southeast Asia, governments have taken strong action to build a banking security ecosystem using biometrics. Malaysia has adopted biometric authentication to enhance payment security after Bank Negara’s 2023 directive to phase out SMS-based OTPs with more secure measures. Major banks, such as Maybank, CIMB, and Public Bank, use biometric features, such as facial recognition and fingerprint scanning, in their mobile apps and ATMs. These technologies allow customers to log in, make transactions, pay bills, shop online, and withdraw cash easily.

Decision 2345 by the State Bank of Vietnam implements high security solutions in digital and banking payments. As of July 2024, banks must adopt biometric authentication for high-risk transactions. These include money transfers worth more than VND 10 million or exceeding VND 20 million per day, and for first-time mobile banking use or access from a new device. Verification is based on the verification of customers’ biometric data with information stored in chip-based ID cards, which is the Vietnam Electronic Identification (VNeID) system, or bank databases.

Singapore promotes biometric authentication under the Payment Services Act 2019, which was enacted in . It requires robust customer and transaction verification for digital payment services. The Monetary Authority of Singapore (MAS) has also issued detailed guidelines that encourage financial institutions to adopt biometric technologies that help strengthen security and improve authentication. In response, banks, such as DBS, Oversea-Chinese Bank (OCBC), and United Overseas Bank (UOB) have implemented facial and fingerprint recognition features in their mobile apps and ATMs.

In March 2023, the Bank of Thailand mandated biometric authentication for high-value transactions. Starting June 2023, banks must use facial recognition for transfers worth more than THB 50,000 (USD ~1,350) per transaction or THB 200,000 per day (USD ~6,160). The central bank issued official guidelines on biometric technology in financial services, effective September 2023. In response, banks, such as Siam Commercial, Kasikornbank, and Standard Chartered Thailand, implemented facial and fingerprint recognition to ensure seamless, secure customer transactions.

The central bank of the Philippines, the Bangko Sentral ng Pilipinas (BSP), promotes advanced security technologies to replace the traditional use of OTPs, after the Anti-Financial Account Scamming Act. Banks such as the UnionBank, Philippine National Bank (PNB), and Asia United Bank (AUB) pioneer this area. It implemented voice, facial, and fingerprint scanning in its banking services.

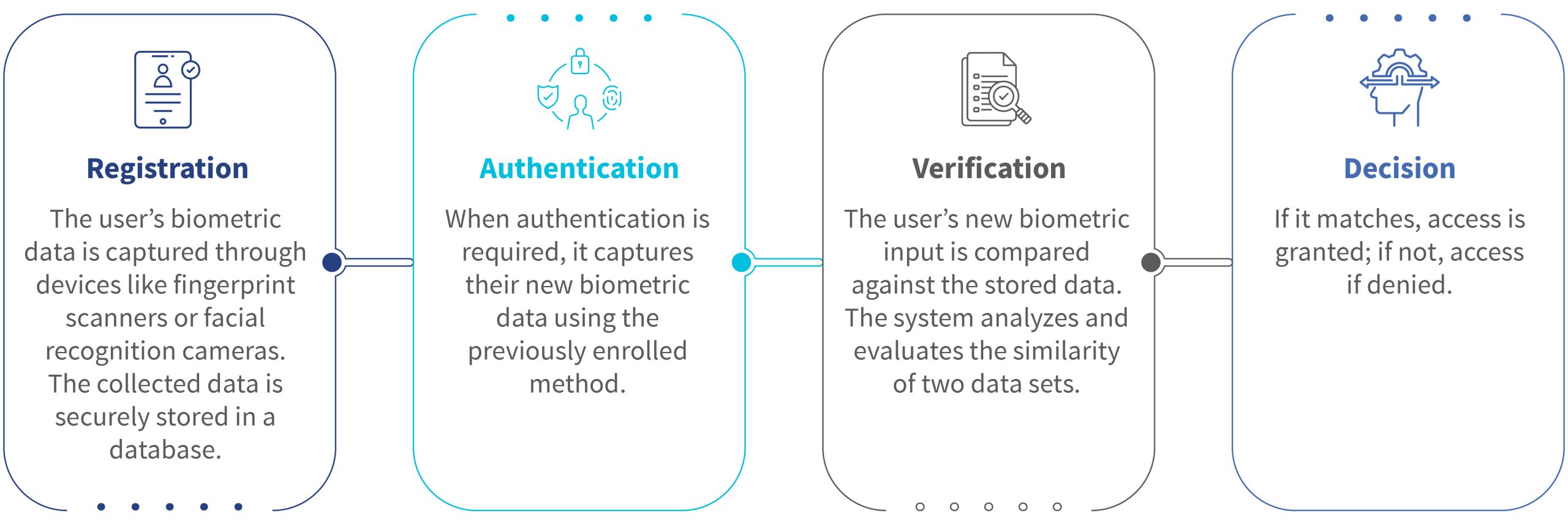

Step-by-step overview of biometric adoption in the finance sector across Southeast Asia

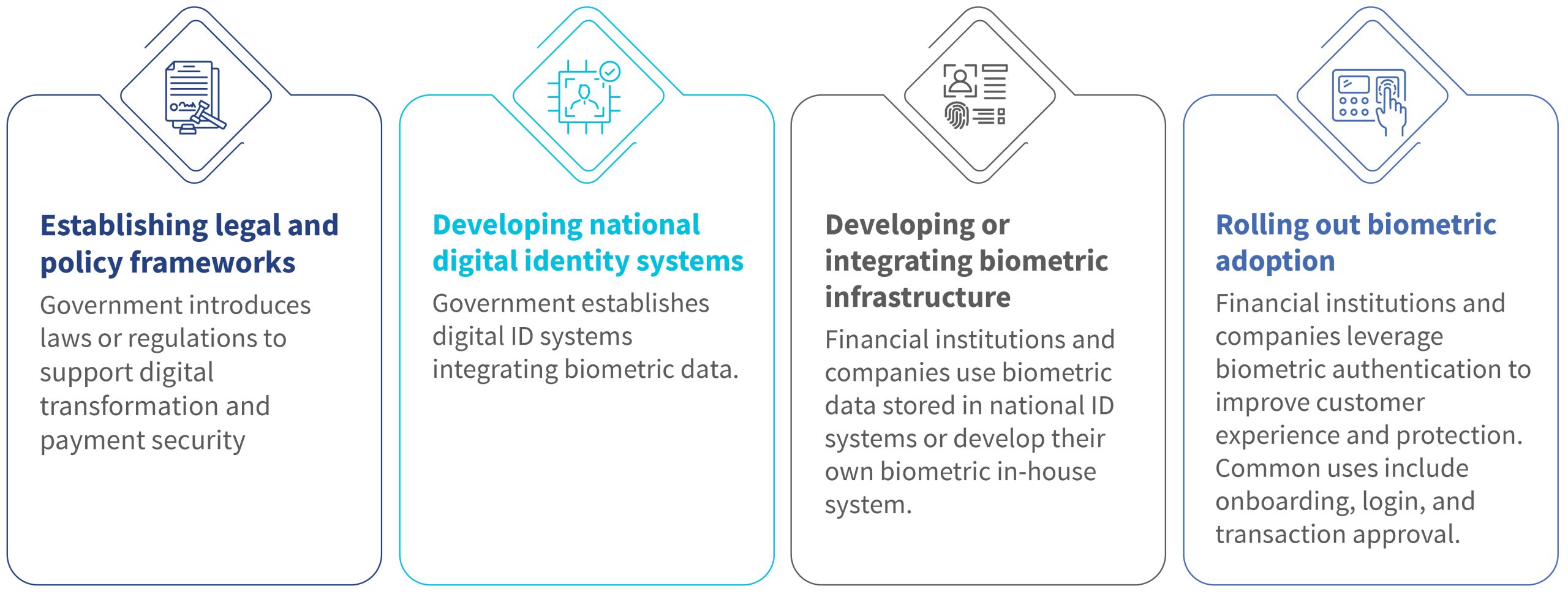

The adoption of biometric technology across Southeast Asia aligns closely with national goals for digital transformation and economic development. As digitalization grows globally, each Southeast Asian country has developed a national digital identity system that uses biometric data to serve its citizens. Citizens must navigate cyberspace securely and confidently to thrive in a digital economy, while banking systems must keep up to remain relevant and effective.

In the long run, biometric technology can serve as a secure gateway to financial inclusion. Banks can simplify access to financial products and services through biometric verification, especially for those previously excluded. With people’s needs at the center, biometrics offer a secure, efficient, and inclusive path toward safer digital finance.

Written by

Disha Bhavnani

Senior Manager

Leave comments