From prayers to power: Scaling climate-smart agriculture through inclusive finance

by Srilasya Nookala, Vikash Kumar Sinha and Anant Jayant Natu

by Srilasya Nookala, Vikash Kumar Sinha and Anant Jayant Natu Sep 24, 2025

Sep 24, 2025 6 min

6 min

Climate-smart agriculture (CSA) offers smallholders resilience against climate shocks by diversifying income and promoting sustainability. Inclusive financial institutions (IFIs) can bridge the financing gap by mobilizing climate-aligned capital, reengineering products, and strengthening ecosystems to scale CSA adoption globally.

In the quaint village of Thiruppachethi in Tamil Nadu, 46-year-old farmer Jayanti Amma often grappled with the uncertainties of the Samba season. Her livelihood depended on erratic rainfall and the Vaigai Dam’s water politics.

Jayanti is not alone. Countless farmers just like her across India struggle with the escalating impacts of climate change. Erratic weather patterns, such as prolonged droughts and unseasonal downpours, have led to frequent pest outbreaks, sharp yield losses, increased input costs, and post-harvest losses, which lead to falling incomes. Studies suggest average farm incomes have dropped by 15–18%. Some sectors report losses up to 25% due to unpredictable climate changes.

Climate-smart agriculture as a path to resilience

Jayanti Amma’s fortunes began to change when the local inclusive finance institution (IFI) she had been with for eight years introduced livestock loans. She and her sister-in-law purchased buffaloes for milk production. She also started to cultivate flowers along with paddy through technical support from a state-run agricultural unit.

This shift toward diversified, integrated farming brought her greater income stability. She now sells milk to a local dairy cooperative, uses paddy husk and cow dung as manure for floriculture, and markets flowers in Madurai’s bustling flower bazaar. She now has multiple sources of income, which enables her to meet each season’s uncertainty with renewed confidence. “I still look to the skies and pray for rain,” she says, “but I am no longer afraid.” Her story reflects how climate-smart agriculture (CSA) is the quiet transformation in rural India that protects our vulnerable farmers from unpredictable climate hazards.

For millions of smallholders like Jayanti Amma, CSA offers a pathway to withstand climate shocks. Promising technologies such as drip irrigation, solar pumps, no-till farming, and biodigesters can boost resilience by promoting water conservation, restoring soil health, and diversifying farmer incomes. Yet for many smallholders, especially women, these solutions remain out of reach due to the high upfront costs and limited access to finance.

Can IFIs bridge the climate resilience gap?

Inclusive Financial Institutions (IFIs) are well-positioned to catalyze CSA adoption, especially among smallholders. With deep community linkages and the ability to channel capital where it is most needed, IFIs can help close the resilience financing gap, (CGAP’s recent paper reinforces the same).While a few IFIs have piloted CSA-linked products, most IFIs’ engagement remains peripheral, limited to small-scale experiments that lack institutional commitments or clear pathways to scale.

We propose a three-level approach to get IFIs to commit and chart a pathway to scaling CSA adoption. While the strategies below focus on CSA, this template can be adapted to build resilience in other sectors, such as WASH, housing, and electric mobility. The three-level approach focuses on how to:

- Enable access to climate-aligned capital for IFIs.

- Reengineer IFI products and processes.

- Strengthen ecosystem-wide support across the supply and demand sides for CSA.

1. Enable access to capital for IFIs

IFIs need access to wholesale climate-aligned debt, such as concessional loans, guarantees, blended finance, and climate-focused equity capital to deliver resilience-linked financial services, guided by green and adaptation lending mandates. This represents a significant, but largely untapped, opportunity for multilateral climate funds.

Encouraging examples of CSA financing are emerging in India, partnerships, such as Pahal-GAWA Capital, Encourage Capital-Annapurna, GiZ-Caspian-Sadhan, Annapurna-Credit Agricole CIB-Grameen Crédit Agricole Foundation, and IIX-Samunnati, show early traction in CSA financing. Institutions, such as the Agri3 fund and Rabo Foundation, which offer risk-sharing mechanisms, reduce lending risks for IFIs and complement these efforts. Globally, the International Finance Corporation (IFC) has invested USD 100 million each in debt and equity in Equity Bank (Kenya) and Banco ABC Brasil S.A. for CSA finance.

However, several ecosystem gaps persist, such as the absence of standardized CSA taxonomies and reporting frameworks, limited access to granular climate-agriculture data, and a lack of cost-benefit analyses for CSA products. These foundational gaps hinder the efficient flow of capital into IFIs. On an encouraging note, the Government of India’s draft climate finance taxonomy and the RBI’s Green Deposit guidelines are progressive steps that can help release more climate-aligned capital for CSA.

2. Product and process reengineering at the IFI level

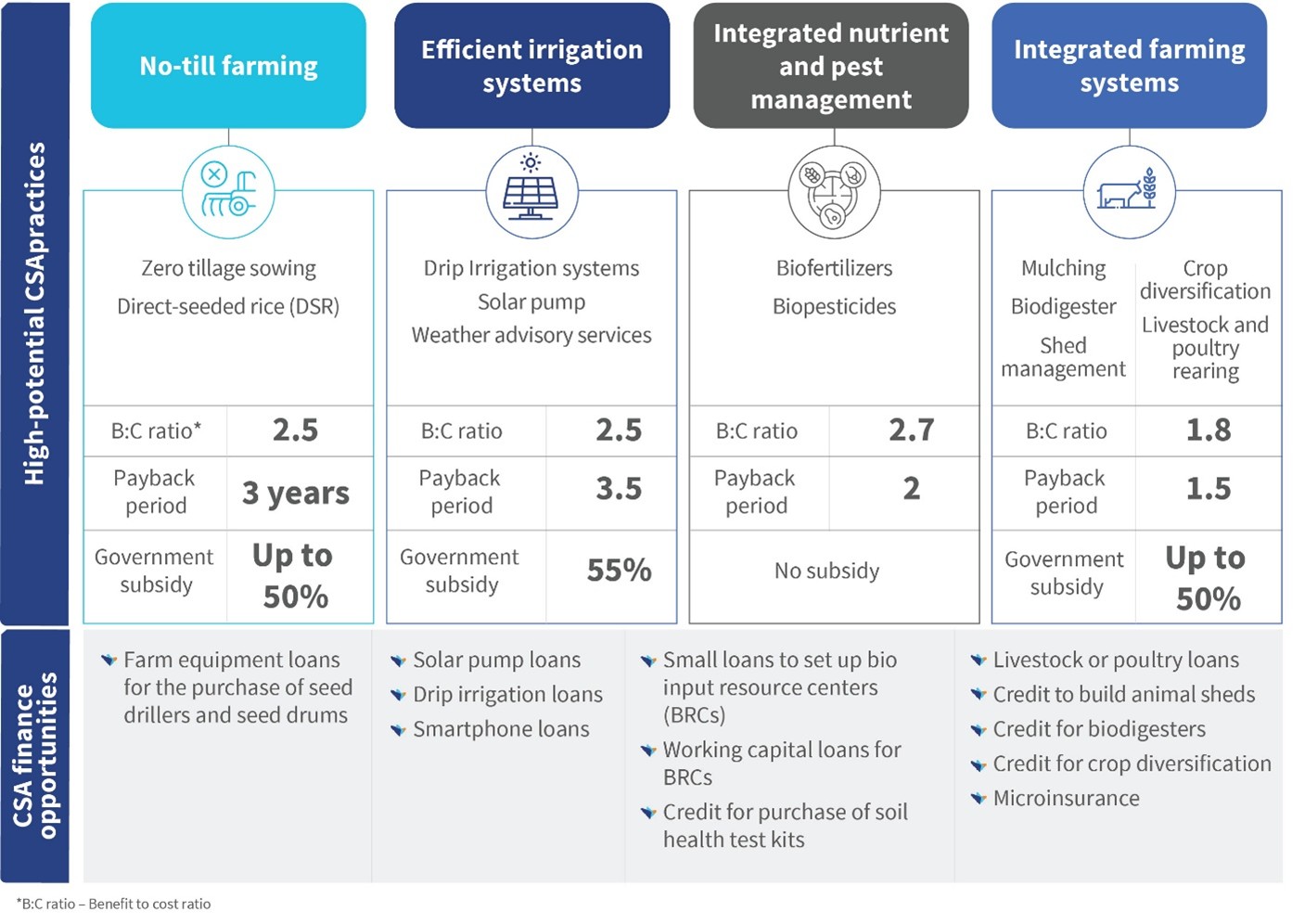

Progressive IFIs, such as Pahal, Annapoorna, and Midland, are moving beyond traditional loans to pilot innovative financing for CSA assets, such as solar pumps and biodigesters. MSC’s research with AGRI3 across three Indian states highlights several pathways for IFIs to scale CSA lending to support high-potential CSA practices, as illustrated in Figure 1 below.

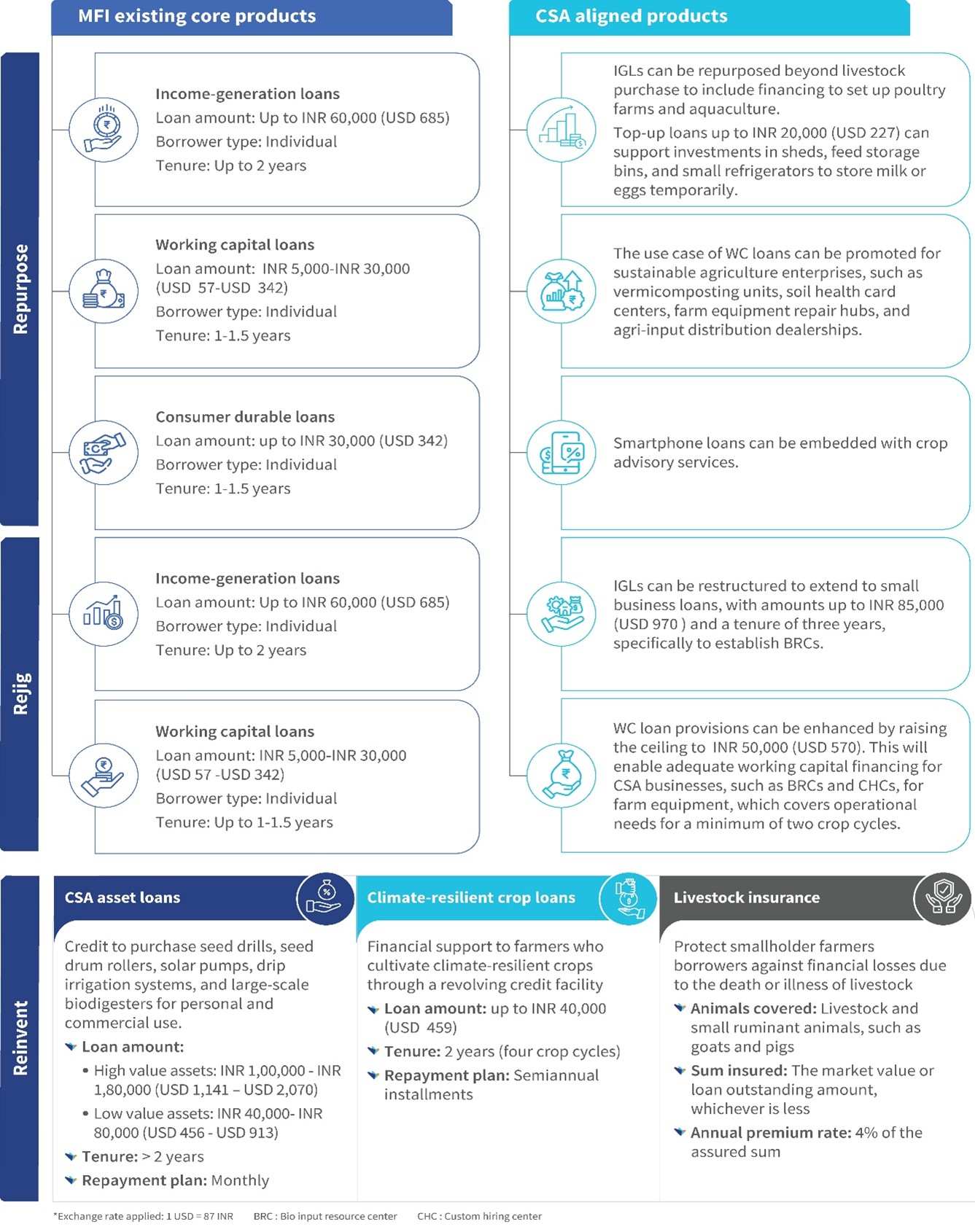

We also identified the CSA financing opportunities for IFIs based on an analysis of their current product portfolio. We proposed that IFIs can adopt one or a combination of three product strategies: Repurpose, Rejig, and Reinvent, to support high-potential CSA practices, as illustrated in Figure 2.

- Repurpose the existing loans for income-generation (IGL), working capital (WCL), and consumer durables to finance smallholders’ investments in backyard poultry, aquaculture, vermicomposting, soil testing, CSA equipment repair centers, and smartphones bundled with digital agri-services apps. Additionally, IFIs can extend top-up loans to support the ancillary financing needs of livestock borrowers.

- Rejig existing loans to support income diversification and resilience. Redesign IGLs by increasing ticket sizes and tenure. This approach would finance business resource centers (BRC) that distribute organic fertilizers in local markets. IFIs can raise the ceilings of WCLs (Working capital loans) to support CSA enterprises, such as BRCs and custom hiring centers (CHCs), that provide farm equipment for rent. This would ensure their operational viability across at least two cropping cycles

- Reinvent products such as asset loans to help smallholders acquire CSA assets such as drip irrigation and bio-digesters. IFIs can provide crop loans to support a shift to climate-resilient contingent crops. IFIs should expand offerings to include livestock insurance for enhanced climate risk mitigation through partnerships.

To strengthen the full credit cycle—outreach, assessment, disbursement, tracking, and risk management—IFIs should collaborate with agritechs (for farm-level data), for performance-based incentives (despite some concerns), government schemes, Original Equipment Manufacturers, and social enterprises. Additionally, IFIs need to invest in three core areas:

- Staff capacity building: IFIs can improve staff capacity through training on CSA appraisal tools. Institutions, such as the National Institute of Bank Management and Sa-Dhan, already offer programs for IFI staff to deploy green and CSA finance.

- IT system upgrades: IFIs can handle flexible loan tenures, differentiated pricing, and adaptive risk scoring for CSA lending.

- Operational de-risking: IFIs can use geotagging, the Internet of Things (IoT), and machine learning tools for real-time CSA monitoring.

These interventions will raise awareness of climate risks within IFIs, equip them to respond actively, and address the gaps highlighted in this MSC–Sa-Dhan study.

3. Ecosystem efforts to prime both the supply and demand sides

Scaling CSA finance requires a supportive ecosystem that empowers farmers, nurtures innovators, and builds financing pipelines. Some promising initiatives include:

- Grassroots programs, such as the NRLM’s Krishi Sakhi initiative and the Tata Trusts’ Lakhpati Kisan, which integrate CSA into rural livelihood programs.

- Startup incubators, such as ThinkAg, AgHub, and a-IDEA, which offer mentorship and seed capital to CSA innovators.

- Government innovation challenges and digital platforms, such as Agri Stack, which support product development, pilot testing, and scale-up through data access and public-private partnerships.

- Blended finance facilities, such as NABARD’s AgriSURE Fund, which supports growth-stage agri-startups with patient capital, technical guidance, and market linkages.

From pilots to scale

As climate change erodes borrower incomes, especially among smallholders and microentrepreneurs, IFIs can feel the strain on their credit portfolios. Diversification into resilience-linked products such as CSA offers a dual opportunity to strengthen customer resilience and expand their own product offerings. IFIs can lead a new wave of climate-smart finance where prayers persist, but power returns to farmers like Jayanti Amma. The shift has begun, quietly but surely, in villages like Thiruppachethi.

Leave comments