Part 2: Moving climate-displaced persons to financial self-reliance

by Gregory Ilukwe, Brenda Oyugi and Violet Njeri Kamau

by Gregory Ilukwe, Brenda Oyugi and Violet Njeri Kamau Dec 9, 2025

Dec 9, 2025 4 min

4 min

This second part of our two-part sequel moves from identifying the barriers faced by climate-displaced persons in Tanzania to exploring practical solutions. Building on Part 1, we now look at how flexible products, simpler onboarding, digital tools, and gender-responsive financial literacy can support displaced communities like Asha’s. Through coordinated action among regulators, FSPs, NGOs, FinTechs, and donors, we can shift financial access from emergency support toward genuine self-reliance and long-term resilience.

In Part 1 of this two-part blog, we explored the harsh realities faced by internally displaced persons (IDPs) in Tanzania, such as Asha, whose lives are upended by climate disasters. We highlighted how the lack of identification, limited access to agents, and systemic trust issues keep IDPs excluded from financial systems, despite the country’s high overall inclusion rates.

In Part 2, we turn from challenges to solutions. How can financial services be redesigned to meet the unique needs of displaced populations? And what roles can regulators, financial service providers (FSPs), and development partners play to transform financial access into genuine economic empowerment?

Asha’s struggle underscores that financial services must be intentionally designed around their lived realities to serve displaced populations effectively. This calls for simpler onboarding processes, flexible and relevant product bundles, trusted grievance redressal mechanisms, and gender-sensitive financial literacy initiatives.

We must promote coordinated action across multiple sectors to create financial services that truly support the underserved. We can redesign financial inclusion strategies to reflect the realities of displacement, which can help Asha and many more turn hope into tangible economic empowerment.

Collaborative pathways toward financial empowerment

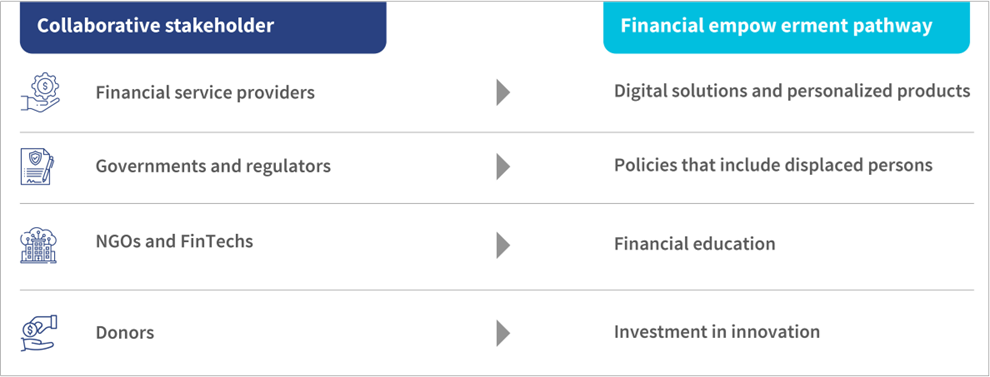

Global evidence shows that displaced persons can thrive when they are supported with the right financial tools within an inclusive financial system. Achieving this, however, requires coordinated action.

FSPs can design flexible, low-cost products customized to the realities of displaced populations, products that meet their immediate needs, and build pathways to long-term resilience.

- Digital solutions: Mobile money and digital wallets reduce the need for physical branches. In Jordan, refugees can register mobile wallets online, which proved vital during the COVID-19 pandemic. Uganda has allowed refugees to open bank accounts through their refugee IDs, which expands access quickly. MSC’s work in Uganda’s Bidibidi settlement under the Agent Network Accelerator (ANA) project highlighted how refugees use digital payments in practice. The study surfaced real-world challenges, such as registration bottlenecks, fraud, liquidity shortfalls, and weak agent networks. Insights from the study informed stronger digital payment strategies in humanitarian contexts.

- Tailored products: FSPs must develop accessible products with IDP-specific realities in mind. They must prioritize flexibility, affordability, and transparency. Small savings accounts with low minimum balances, microloans with flexible repayment terms and no collateral requirements, and insurance for climate or health risks are essential. Community finance groups, such as village savings and loan associations, continue to be a proven entry point, especially for women.

Governments and regulators should create supportive frameworks that address identification and access barriers, which enhance grassroots consumer protection.

- Policies that include displaced persons: National financial inclusion strategies must recognize IDPs as part of the population. Regulators can adopt flexible rules to make services accessible. For instance, policies need to accept refugee IDs or risk-based customer checks to be truly inclusive. MSC supported the Alliance for Financial Inclusion (AFI) in Tanzania to conduct a diagnostic study on the financial inclusion of climate-induced forcibly displaced persons (FDPs) and their host communities. The findings shaped a roadmap for the Bank of Tanzania to integrate FDPs into the National Financial Inclusion Framework (NFIF). This step brings displaced communities into the same financial system as everyone else. The roadmap suggested that government bodies should prioritize rapid, alternative identification methods, increase agent network density in areas affected by displacement, and strengthen consumer protection awareness at the community level. The roadmap suggested measures that ensure FSPs have effective complaint-handling and dispute resolution mechanisms.

NGOs and FinTechs are vital in order to promote trust, deliver effective localized financial education, and codesign community-centric and relevant financial solutions.

- Financial education: UNCDF’s financial education toolkit for refugees and host communities illustrates that training programs delivered through NGOs, local partners, or mobile platforms help people understand and use services effectively. Despite refugees’ and IDPs’ contextual differences, this toolkit, developed in collaboration with MSC, indicates that building financial literacy increases confidence and reduces exploitation. These training programs can include community-level financial literacy with a comprehensive curriculum that covers budgeting, saving, borrowing, and using digital financial services. These training programs have shown that we need to promote financial literacy initiatives to address systemic trust issues that resonate in local contexts. Simple, SMS-based educational modules and facilitated group training have bridged knowledge gaps, which promote greater confidence and proactive usage. Such efforts, though nascent, can possibly transform financial relationships from fearful transactions into empowered interactions.

Donors play a crucial role by funding pilots that innovate and test new solutions.

- Investment in innovation: 122 million people have already been forcibly displaced. These shocking numbers are expected to rise as climate events become more frequent and severe. Donors should invest strategically in innovative, displacement-focused financial inclusion initiatives. These initiatives include decentralized and locally led financing mechanisms that empower communities. Donors should also support green and inclusive financial policies that target vulnerable groups, and link funds to performance for transparency and impact on resilience.

Way forward

The challenge of financial displacement is urgent, but it can be solved. Governments can adopt inclusive policies and integrate displaced populations into national strategies, while regulators can allow alternative IDs and flexible risk assessments.

In turn, FSPs can design products that meet real needs, rather than focus solely on perceived risks. Technology providers can also extend digital solutions to remote areas and settlements.

Development partners can de-risk investments, fund digital infrastructure, and support blended finance mechanisms. Additionally, civil society can amplify the voices of displaced individuals, provide financial education, and serve as a bridge between communities and FSPs.

Financial displacement strips Asha and those many others of their agency and dignity. Financial inclusion can restore both. The choice is whether we continue with short-term aid or build systems that give displaced persons the tools to become self-reliant and contribute fully to their communities. The latter seems to be the most inclusive and empowers the path forward.

Leave comments