Why female agents are the litmus test for Nigeria’s new agency banking guidelines

by John Olawole Martins, Mitali and Brenda Oyugi

by John Olawole Martins, Mitali and Brenda Oyugi Apr 15, 2026

Apr 15, 2026 6 min

6 min

Nigeria’s new agency banking guidelines promise better regulation, clearer accountability, and stronger oversight. Yet, without targeted support for female agents who have contributed to financial inclusion, such as Yetunde, these gains could be lost. Read her story to understand why this matters.

In Lagos’ bustling Balogun Market, Yetunde begins her day before dawn. A mother of three and a market trader, Yetunde balances trays of zobo, a popular Nigerian drink made from dried hibiscus flowers. Her point-of-sale (POS) devices sit ready beside her stall. She earns a small commission of about NGN 100 (~USD 0.07) to NGN 500 (~USD 0.3) per transaction on OPay and Moniepoint. Over a month, she earns NGN 90,000–360,000 (~USD 66–263). Yet, after she pays for data, float, rent, and electricity, what she retains falls below NGN 50,000 (~USD 32).

Please note that the figures are illustrative and based on stated assumptions. Actual income and costs will vary. USD equivalents reflect the prevailing CBN official rate as of the time of publication and are subject to change.

While the individual amounts may appear minimal, their cumulative effect is significant. Over time, these earnings contribute meaningfully to household expenses, school fees, and her family’s day-to-day financial stability. However, the reliability of her earnings depends on several factors. Yetunde must maintain adequate liquidity to meet withdrawal requests. Network connectivity must remain stable to process transactions without interruption. Customer demand must also remain steady to sustain transaction volumes.

Yetunde’s case illustrates the fragile economics that underpin the nearly 2 million POS agents in Nigeria. The sector has expanded access, especially in areas without banks. Yet, many agents operate on razor-thin margins. Their business hinges on stable cash flow, reliable connectivity, and steady customer traffic. A single outage or cash shortfall can wipe out their income and customer trust overnight.

Across emerging markets, agency banking has become a vital channel to reach women and other underserved populations. Regulators tighten their controls as these systems mature. Nigeria’s new agency banking rules intend to boost oversight, but their success hinges on protecting the agents who built inclusion. Female agents, who connect women to finance, are the true litmus test of whether the system becomes more inclusive or more exclusionary. Can new rules strengthen oversight without weakening the very agents that made inclusion possible?

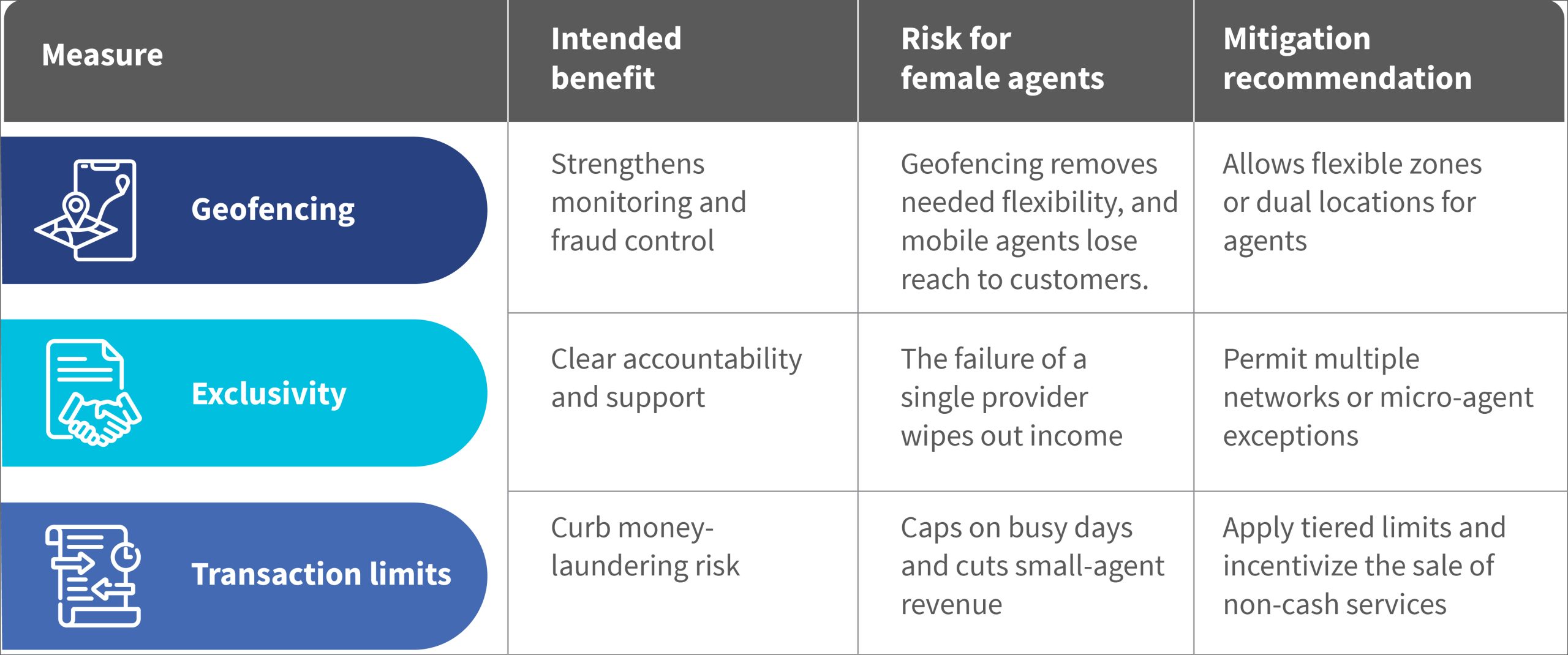

Nigeria’s new agency banking guidelines test this question. The Central Bank of Nigeria (CBN) released new guidelines for agency banking operations. These guidelines introduced measures on exclusivity, geofencing, and transaction limits. The measures offer meaningful benefits to the financial ecosystem. They also significantly help financial service providers (FSPs) and the Nigeria Inter-Bank Settlement System (NIBSS) to monitor agent activity in real time through geo-fencing and transaction data. These systems flag anomalies when agents attempt to breach transaction limits or geo-fenced boundaries and sanction non-compliant agents to enforce compliance. However, these guidelines have unintended consequences for the very agents who built financial access from the ground up. Female agents are particularly exposed to the consequences, which include, but are not limited to, income loss, reduced flexibility, and a higher risk of dropping out.

This exposure has adverse effects on an already underrepresented group. As per a CBN-commissioned situational analysis published in April 2023, women accounted for just 15% of Nigeria’s 700,000 registered agents. Besides being a minority in the network, they also face structural constraints that make it disproportionately harder for them to meet the new requirements.

Female agents, such as Yetunde, play a critical role in this ecosystem. These agents are not just participants but catalysts for financial inclusion. The 2025 Breaking Barriers report by MSC (MicroSave Consulting) finds that female agents generally provide higher-quality service and build stronger trust with customers.

In Northern Nigeria, women often avoid bank branches because the nearest one may be too far, transport is unaffordable, or because social norms make women’s interactions with male staff uncomfortable. In Nigeria, this is a core issue, not a side effect. Female agents reduce these barriers and bring banking services into spaces where women feel comfortable, which addresses both distance and cultural barriers to access. EFInA reports that only 70% of women are financially included, as against 79% of men. Female agents are therefore not just part of the network but are central to closing Nigeria’s gender inclusion gap.

At the same time, female agents operate under more constrained conditions. Safety concerns, harassment, and security risks influence where and when they can work, which often limit their work hours or compel them to avoid certain areas. These factors directly affect income stability and business continuity. Female agents report higher exposure to threats when they handle cash. Many cut business hours or drop out entirely because of these risks. These constraints determine who survives a tightening regulatory environment.

Nigeria’s new CBN guidelines have been introduced in this context. They are meant to improve oversight, but each guideline also impacts agents differently:

This new framework opens opportunities, but mostly for those already capable. Geofencing can protect a fixed-location agent from random interlopers. Exclusivity can deepen agent–bank partnerships if the bank invests in its agents. Transaction caps can push agents to sell higher-value services, such as bill payments, account opening, and loans that carry higher fees. Yet, these upsides will mostly help agents with capital and support, not the micro-operators on the margins.

Scale alone does not mean stability. Beneath this rapid expansion lies a fragile and sensitive business model. This fragility does not affect all agents equally. Those with stronger capital buffers can manage peak demand and absorb short-term shocks. However, smaller agents, particularly female agents with limited working capital and additional constraints, are the least equipped to absorb these shocks.

In effect, these rules tighten control at the system level but create shocks at the agent level. Female agents work with lower margins and have fewer buffers. Hence, they feel that shock more sharply.

Nigeria’s broader inclusion trends underscore the stakes. Financial inclusion increased from 68% in 2020 to 74% in 2023, but women still lag. Progress is uneven, and women often gain last. If the new guidelines make it harder for female agents to survive, inclusion could stall or even reverse.

The critical question now is how to manage this transition. The rules that help some may force out the most vulnerable without targeted support. The regulator should ensure the new framework strengthens inclusion rather than undermines it. We propose the following policy recommendations for regulators to protect vulnerable agents and strengthen the system.

Regulators can introduce a micro-agent tier that exempts low-volume, single-location agents from strict exclusivity and higher caps, based on Tanzania’s model:

- The Bank of Tanzania’s agent banking guidelines document that agents shall not be exclusive to a Financial Service Provider. MSC’s report states that female agents in Sub-Saharan Africa operate across multiple locations. These include homes and market stalls to serve clients safely and in culturally suitable spaces. Regulators can allow flexible geofencing, such as registering multiple approved locations at home and market stalls, or a small service zone per agent. A rigid single-location geofence would therefore directly undermine this operational reality.

- Regulators can require gender-disaggregated data and a formal post-implementation review. The review will mandate that providers report agent activations and attrition by gender. EFInA’s Access to Finance survey shows the value of gender-disaggregated financial data in Nigeria. The same rigor should apply to agent network monitoring.

- Regulators can provide liquidity and float support that includes dedicated float loans or cash pools for female agents to meet peak demand. MSC’s report establishes that female agents face greater liquidity constraints than their male counterparts, partly due to smaller starting capital and limited access to credit. Providers and the CBN should explore targeted float credit facilities for female agents.

- Regulators can offer female agents tailored training and support, capacity-building in fraud prevention, liquidity management, and diversified services, such as bill payments and microcredit. The GSMA’s report shows that structured training for female mobile money agents meaningfully increases their transaction volumes and retention rates. The CBN and licensed operators should make such training a formal requirement of the new agent certification process.

- Regulators can pair strong regulation with dedicated support for female agents. Otherwise, the system may become more regulated yet less inclusive.

For Yetunde and thousands of women like her across Nigeria, these guidelines will determine if they can continue to serve their communities. Nigeria’s agency banking success was built on trust and flexibility. If female agents thrive, inclusion wins. If they falter, the gains of the past decade may unravel.

Leave comments