How community-led MSMEs and women entrepreneurs can rebuild rural distribution networks

by Shubha Bhanu and Ashwin Shukla

by Shubha Bhanu and Ashwin Shukla Apr 17, 2026

Apr 17, 2026 6 min

6 min

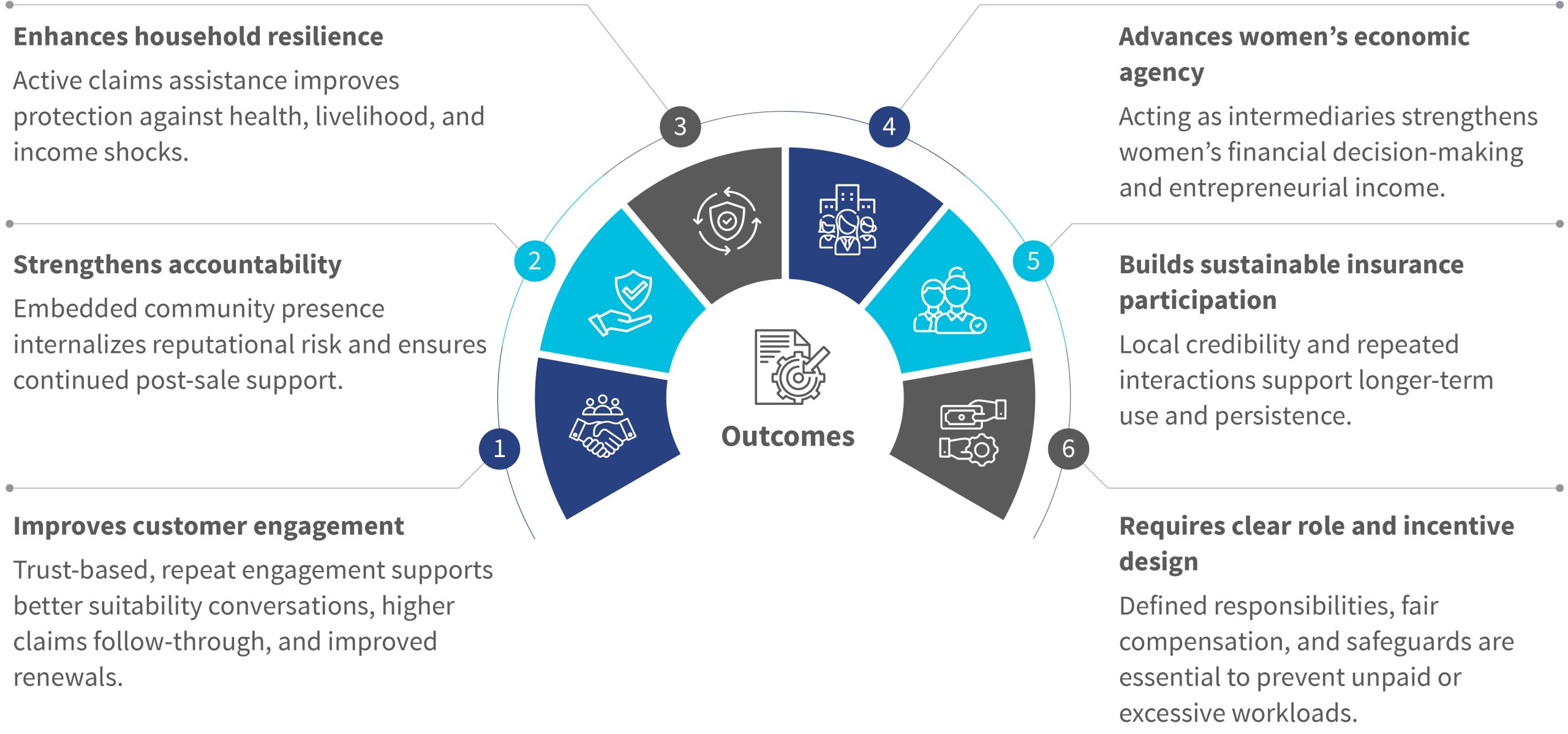

“Insurance creates protection only when people can access and trust it.” India’s rural insurance challenge lies not in the lack of products but in the absence of effective last-mile support. Empowering trusted community-based intermediaries, especially women-led MSMEs, can bridge this gap by improving awareness, simplifying claims, building trust, and turning insurance coverage into meaningful financial protection for rural households.

A village story that reveals a national problem

When Meera Devi’s husband died suddenly in rural Odisha, she knew her family had insurance. Every year, the bank automatically deducts a small premium from their account under government schemes, such as the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), the Pradhan Mantri Suraksha Bima Yojana (PMSBY), and the Ayushman Bharat card. However, when Meera tried to claim the benefit, she was lost. She did not know which policy to apply, whom to approach, or what documents were required. The bank branch was far away, the agent who enrolled her was no longer available, and the process felt intimidating. Eventually, she gave up.

A few kilometers away, another woman, Nita, faced a similar crisis but had a different experience. Nita reached out to a local MSME woman owner in her neighborhood, who helped her identify the right policy, collect documents, and follow up with the insurer. The MSME owner patiently explained insurance and support claims, thanks to her training by a financial institution. Within weeks, the family received the payout. The difference here was not the insurance product but the presence of a trusted, trained local intermediary.

This is a problem that remains all too common across India’s hinterlands, where millions of households have insurance but lack protection due to gaps in distribution and service.

The last-mile gap: When insurance exists but protection remains out of reach

Today, banking outlets reach 99.7% of India’s villages through more than 550 million Pradhan Mantri Jan Dhan Yojana (PMJDY) accounts, two-thirds of which are in rural areas, while UPI powers 87% of transactions among rural youth. Yet, insurance coverage continues to lag. Life insurance penetration and density remain disproportionately low at 10% in rural geographies, with protection levels significantly below risk exposure levels. This leaves most households financially vulnerable to shocks.

Despite growing access to financial services, households have poor understanding of insurance, underuse it, and often distrust it. Complex products, weak post-sale support, and low trust in claims processes mean that many households continue to rely on savings, informal borrowing, or asset sales during shocks.

Within this broader landscape, rural women experience risks more severely due to lower asset ownership, income volatility, and limited access to formal support systems. Their experience with insurance is often as bundled coverage linked to bank accounts, credit products, or government schemes. Enrollment happens automatically and offers little understanding of benefits or claims procedures. Insurance models that prioritize enrollment volumes over suitability assessment, disclosure quality, and post-sale servicing have resulted in low persistency or renewals, grievance escalation, and erosion of trust.

Global research from the Centre for financial inclusion, Accion reveals that complex products, opaque communication, and cumbersome claims erode trust, which pushes households toward savings or informal loans during crises. These factors underscore how flawed last-mile engagement and incentive designs undermine insurance’s protective potential. To address these challenges, regulators and the industry are beginning to rethink insurance distribution.

For example, the Insurance Regulatory and Development Authority of India (IRDAI) recognized the need to strengthen last-mile insurance distribution. It introduced the Bima Vahak Guidelines 2023. The initiative seeks to place trained bima vahaks at the gram panchayat level to serve as local insurance intermediaries. These agents help communities with policy enrollment, proposal, and KYC processes, premium payments, and claims support through digital devices. The guidelines embed accountable, locally trusted representatives within villages to close long-standing gaps in awareness, accessibility, and post-sale service that traditional insurance channels have struggled to address.

The pan-India insurance gap for rural women

As per government sources, enrollment under the Jan Suraksha schemes remains 47% among low-income women, yet effective utilization during income shocks remains negligible. Voluntary retail insurance penetration among rural women remains limited at 18-20% as per Department of Financial Services (DFS) report. These numbers indicate weak demand-side confidence despite high scheme-based enrollment. Many first-time policyholders perceive insurance as less of a tool for protection and more as a routine bank deduction, with a limited understanding of benefits, exclusions, or claims processes.

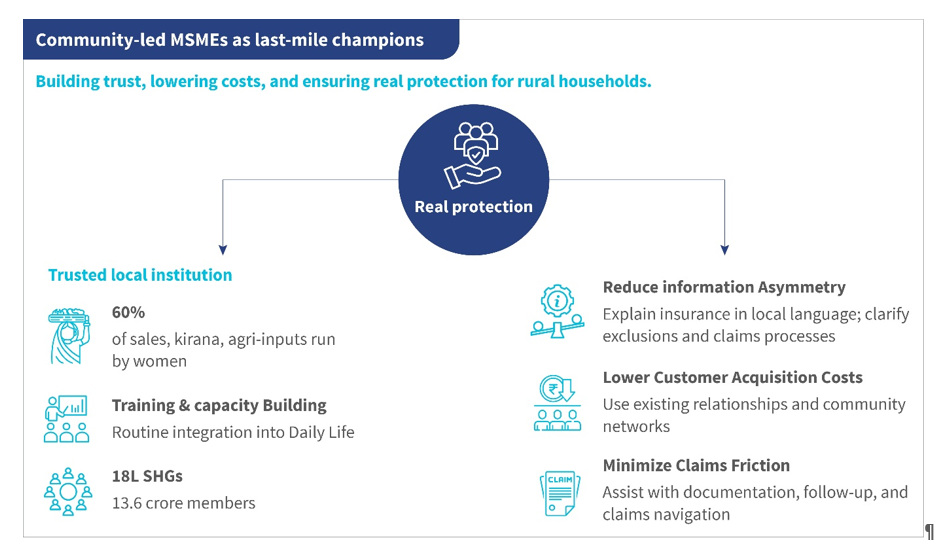

Community-led MSMEs as last-mile champions

Community-driven MSMEs make insurance more relevant, accessible, and effective

Community-led MSMEs are micro and small enterprises owned, operated, and trusted within the communities they serve. These include agri-input shops, self-help groups, and women collectives that provide advice, informal credit, and solve the local issues.

They offer a structurally different architecture rooted in embedded trust networks and livelihood-based engagement. Embedded within communities, they can act as educators, suitability filters, premium collection points, and claims navigators. They support customers across the insurance lifecycle, and help reduce information gaps, reduce customer acquisition costs through existing networks, and ease claims processes through documentation support and follow-ups. This shifts insurance from transactional sales toward sustained engagement and practical protection.

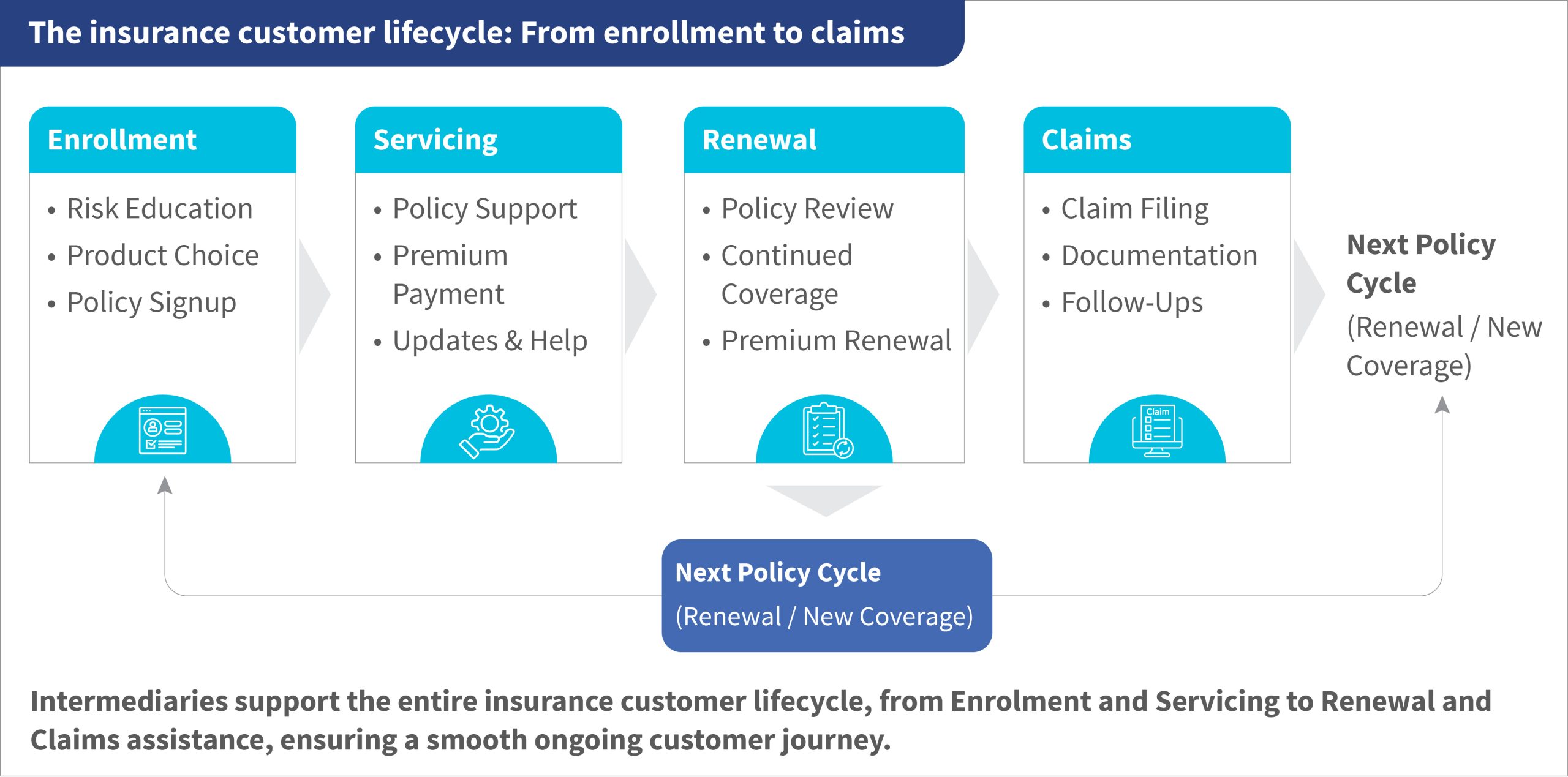

The insurance customer lifecycle: From enrollment to claims

Women entrepreneurs as last-mile risk intermediaries

Women entrepreneurs as a last-mile champion

Within this ecosystem, women entrepreneurs play a vital role as insurance intermediaries. Their credibility stems from strong social capital and reputational accountability, where failure to support customers can affect their community standing and core livelihood activities. Through regular interaction with households, they simplify communication, explain insurance in local contexts, and help with enrollment, renewals, and claims. Their proximity and familiarity with digital tools improve customer understanding, strengthen policy persistence, and build confidence in insurance as a reliable risk management tool.

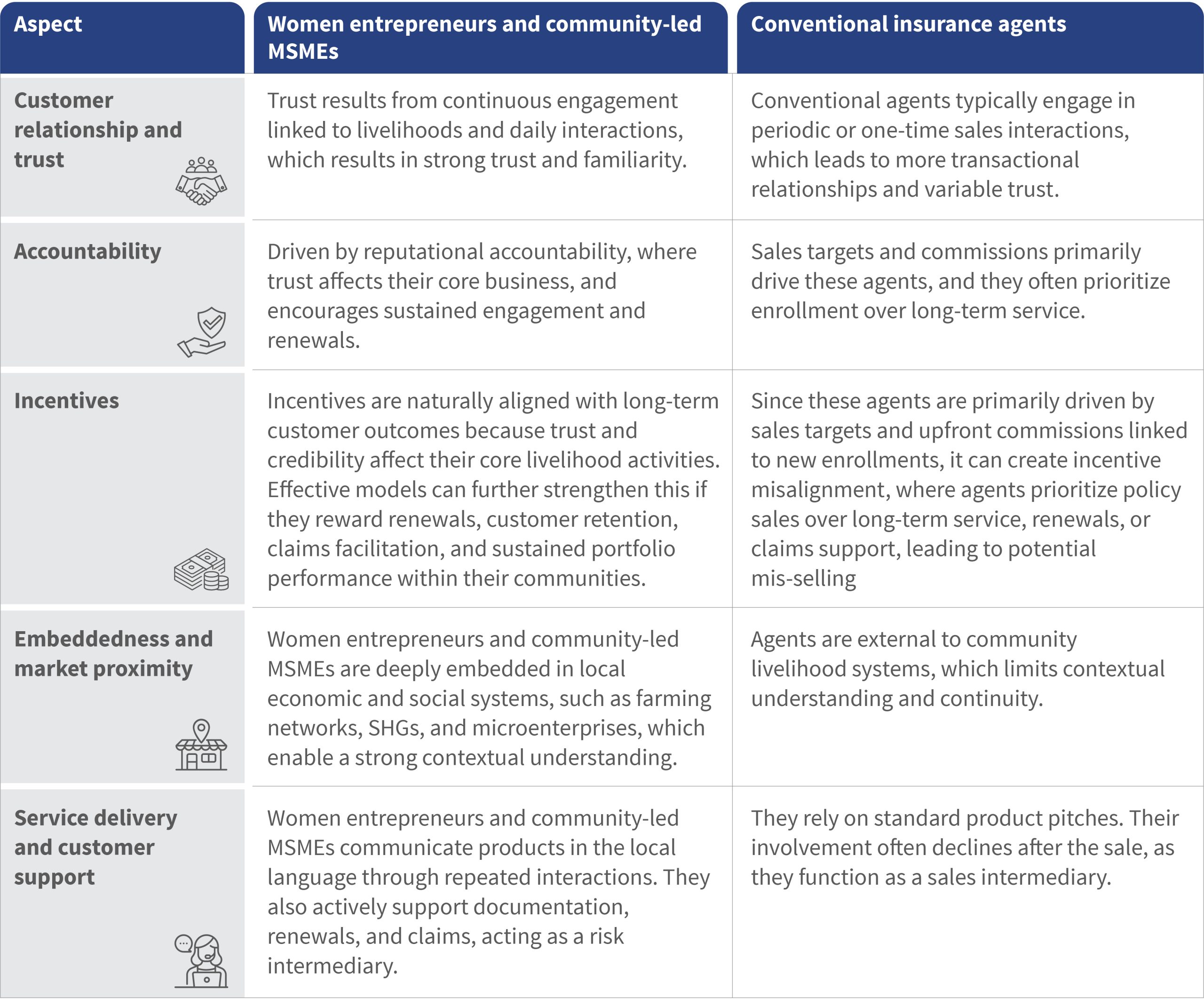

How women entrepreneurs differ from conventional insurance agents

The differences between community-led women intermediaries and conventional insurance agents are structural, not merely operational. They reflect fundamentally different incentive systems, accountability mechanisms, and relationships with customers, as outlined below:

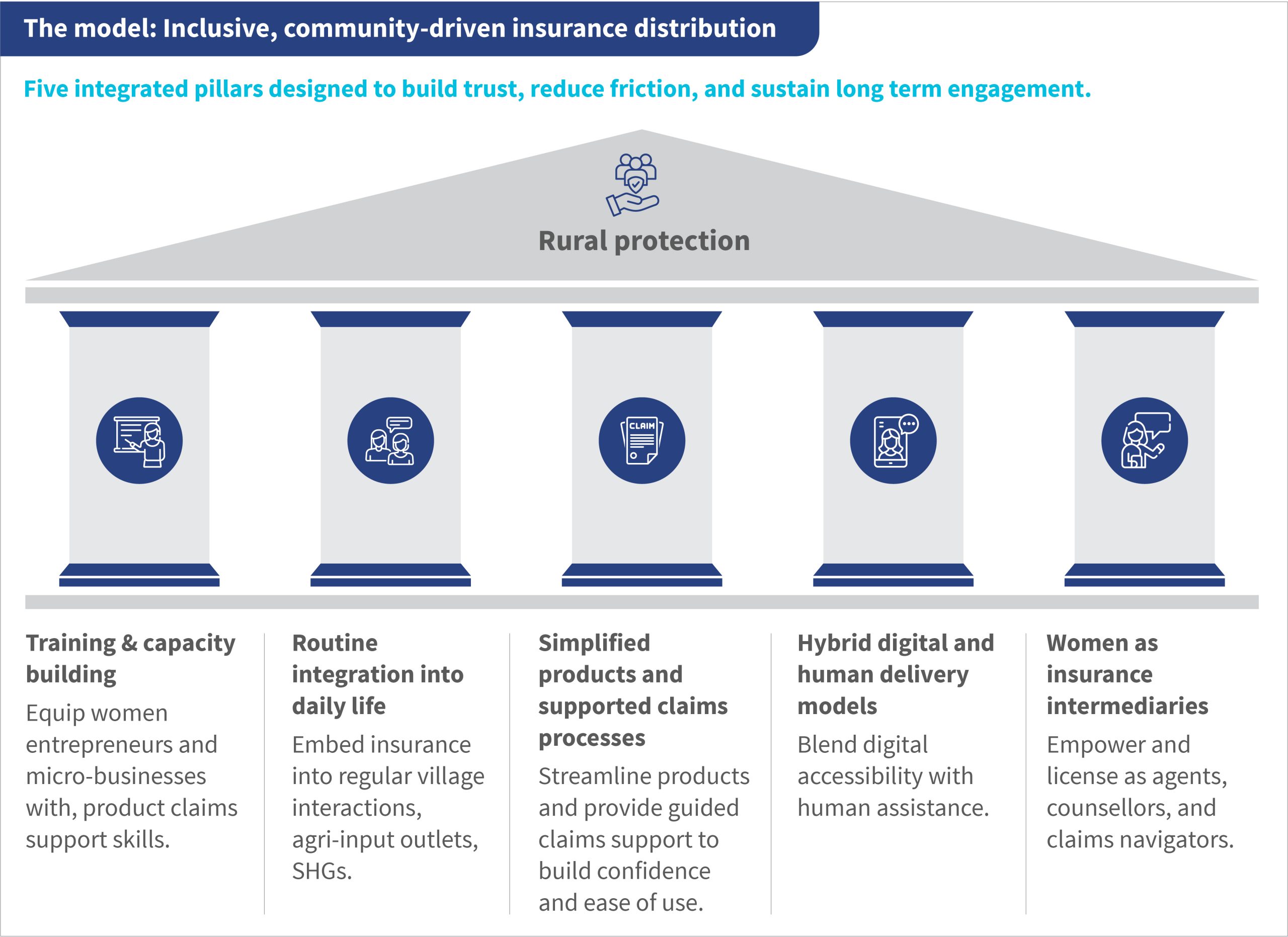

An inclusive, community-driven insurance distribution model

Experience from rural insurance markets shows that access without trust weakens protection. When customers do not understand products or lack post sale support, coverage remains underused. Addressing this requires a distribution model that is designed to build confidence, reduce friction, and sustain engagement.

Structured certification and modular training linked to performance-based incentives can equip women entrepreneurs and microbusinesses with product knowledge, suitability assessment capability, digital onboarding proficiency, and claims facilitation skills. The use of simplified products, supported claims processes, and a ‘phygital’ model that integrates assisted digital tools with human advisory can further improve onboarding accuracy, enhance documentation quality, and foster trust among first-time users.

The scalable model where coordinated pillars reinforce resilient rural insurance systems

Benefits beyond insurance sales

Beyond insurance enrolment, community-led distribution strengthens market conduct, household resilience, and women’s economic participation. When women entrepreneurs and community-based MSMEs act as insurance intermediaries, they also create income diversification opportunities, as it adds a new service line to their existing livelihoods. Commissions, renewal incentives, and service-based payments can provide supplementary income and simultaneously strengthen their role as trusted financial resources within their communities.

The outcomes below highlight why distribution design matters as much as product design in rural insurance markets

Recommendations for scaling across India

The benefits women entrepreneurs and community-based MSMEs bring about when they work as agents is abundantly clear. In this context, we propose a set of actionable recommendations for key stakeholders to enable scalable and sustainable adoption across India.

- Partnership ecosystems: Build alliances between insurers, SHGs, local microenterprises, and government programs for cohesive outreach

- Localized product innovations: Customize micro-insurance offerings to reflect regional risks and socioeconomic contexts

- Effective agent training: Continuous, gender-sensitive capacity building for women agents that focuses on communication and trust-building

- Awareness and literacy campaigns: Deploy community campaigns with familiar social networks and media suited to rural audiences

- Technology enablement: Introduce accessible digital interfaces enhanced with human support for trust and ease of use

Conclusion

While Meera Devi gave up, Nita could access timely support, thus highlighting that India’s rural insurance gap is driven less by product availability and more by weaknesses in distribution and market conduct. In the absence of accountable last-mile engagement, high enrollment can mask significant protection gaps. Misaligned incentives, weak separation between advice and sales, and limited post-sale support have historically eroded trust, prompting regulators to strengthen norms around suitability, disclosure, and intermediary accountability.

Expanding insurance coverage alone will not close this gap. What matters is trusted, continuous engagement at the last mile. Women entrepreneurs and community-led enterprises, when embedded within insurance delivery systems, can bridge this divide by transforming enrollment into understanding, claims into confidence, and coverage into meaningful financial protection.

Written by

Shubha Bhanu

Associate Partner

Leave comments