How will the COVID-19 pandemic affect the Indian fintech startup ecosystem: Four predictions and one suggestion

by Anshul Saxena

by Anshul Saxena Apr 20, 2020

Apr 20, 2020 3 min

3 min

As with all players in the economy, fintechs too are feeling the heat of the COVID-19 pandemic. Early trends indicate a host of changes in the horizon. These include four key developments in the fintech ecosystem. Read our analysis for more.

Around the world, the COVID-19 pandemic has changed the way we think about life and work. India remains in lockdown as field operations have been shut down and work-from-home is implemented across the board. Much of the fintech startup ecosystem will have to wait and watch to see how the situation unfolds after the official lockdown is over.

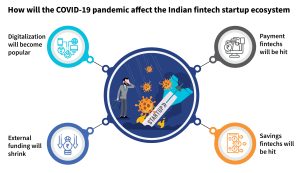

However, some early trends signal what is in store:

Digitalization wave

We will see digitalization happening across the board, from processes, to how employees interact with each other, to how the banks, fintechs, and other players reach their customers. Let us look at a few examples:

Functioning of microfinance institutions (MFIs) and non-banking financial institutions (NBFCs): MFIs and NBFCs have traditionally been driven by physical methods of cash collection, physical verification and onboarding of new customers. With the new normal of curtailed physical interactions, these institutions will seek ways to transform their physical and manual processes into automated and digital ones. They will look toward fintechs, especially start-ups, as they can support the MFIs and NBFCs in making this change with lower costs and quicker turnaround.

Agricultural practices: The COVID-19 pandemic will affect the incomes and modes of payments of farmers. In India, agricultural practices are largely labor-intensive and manual. This applies to tilling, plowing, sowing, and harvesting. Farmers also need to physically visit lenders—private money-lenders in most cases—and must get cash to revisit and repay their loans. The farmers, especially small landholders who have feature phones and even smartphones generally use them to consume entertainment content. We anticipate a big change coming here. Due to the restrictions imposed because of the pandemic, many lenders will embrace the idea of digital payments and farmers will thus be aligned to do so as well. In the coming months, digital payment collections should see large-scale adoption in rural areas through methods, such as UPI, IMPS, and auto-debit facilities, such as NACH.

E-commerce and its effect on payment fintechs

A major bulk of revenue for fintechs that work in payments comes from transactions in the e-commerce industry. E-commerce platforms like Flipkart and Amazon India sell a mix of non-essential and essential items. Because of the COVID-19 pandemic, these online retailers have recently stopped selling non-essential items in the short to mid-term, or between a few weeks and a few months. Since the essential items that are now sold on these platforms have low margins, the private digital payment companies or payment fintechs in India will see their revenues shrink. This will be because their margins ride on the volumes and values of transactions. With essential services being sold more frequently, despite higher volumes being sold, the effect on the margins on these low-priced goods will have a more drastic impact on their revenues.

Hit on short-term savings

With the uncertainty around the availability of food and essential items in the market, many people will switch from savings to keeping money (cash or digital) readily available to spend at short notice. This behavior will lead to a decrease in the usage of short-term savings instruments for the near future.

Survival or not

As private investors get jittery over making any new investments, they are trying to first selectively invest any available money to protect companies in their portfolios in this hour of crisis. Hence, fintechs with weak business models that rely heavily upon investor money will fizzle but the ones with solid though smaller revenue models, especially the bootstrapped ones will have a good chance to come to the fore, provided they have or can build their runways for the next 6-12 months at least.

What can be done to help the fintech ecosystem?

In these times when the future of business is uncertain and survival of fintechs—especially startup fintechs—is doubtful, the government can play a pivotal role in supporting them. How? For instance, the central and state governments can give tax breaks, tax holidays, or other incentives to the banks and financial institutions who utilize the technology strengths of fintech startups in digitalizing their processes—especially in the priority lending sector. As discussed earlier, many NBFCs and MFIs still have either manual processes or rely on archaic technologies. They have never prioritized upgrading to more automated software systems. Yet now is the perfect time to help them do it as they look at ways to grow their businesses with a minimal workforce.

The blog was first published on News 18 Tech and then picked up by Yahoo news.

Leave comments