Women Digital Ambassador: Linking agents to cooperatives for parity in financial inclusion

by Putu Monica Christy and Putri Agnesia Wardhani

by Putu Monica Christy and Putri Agnesia Wardhani Mar 30, 2023

Mar 30, 2023 7 min

7 min

In partnership with BRI (Bank Rakyat Indonesia), MSC connected BRILink agents to cooperatives under the Women Digital Ambassadors (WDA) project. The linking was part of our efforts to increase the accessibility of financial products and services for Indonesia’s rural women. We used MSC’s Datin app to monitor and evaluate each agent’s transactions and generate findings from the field. These findings allowed us to identify opportunities and challenges in linking agents to women cooperatives, which we distilled in our new blog. Read it here.

In the previous blog, we discussed how Women Digital Ambassadors have their tailored digital business training. We also mentioned that linking women cooperatives to the agent banking network brings financial products and services closer to women’s reach—eradicating barriers and obstacles to access.

Digital transformation fostered a growing number of female banking agents

The number of agents in Indonesia grew exponentially during the pandemic. In 2021, the number rose from 1.24 million in September to 1.45 million in December. Presently, 35 national and regional banks serve the branchless banking (Laku Pandai) agent network across more than 511 Indonesian regencies or cities in 33 provinces. However, the expansion of agents concentrates on Java Island at around 64.18%. West Java province has the highest density (18.79%) of agents, while Maluku and Papua provinces have the lowest density at 2.02%. Regrettably, gender-disaggregated data is absent on agent ownership, making it difficult to monitor the growth of female agents.

Despite the missing data on female agents in Indonesia, mounting evidence worldwide shows that applying a gender lens to agent networks can help identify these opportunities and threats that affect the expansion of their reach. A previous MSC study on female business correspondents or BC agents resonates with the everyday challenges of recruiting more female agents, which require more resources and effort.

Female agents face several challenges in their path. Even as they maintain their business, female agents: 1) need to convince their families to permit them to start working as agents; 2) face mobility and safety challenges in commuting; 3) can only have fewer working hours due to the more significant burden of domestic responsibilities; and 4) meet greater challenges with technology due to low prior exposure.

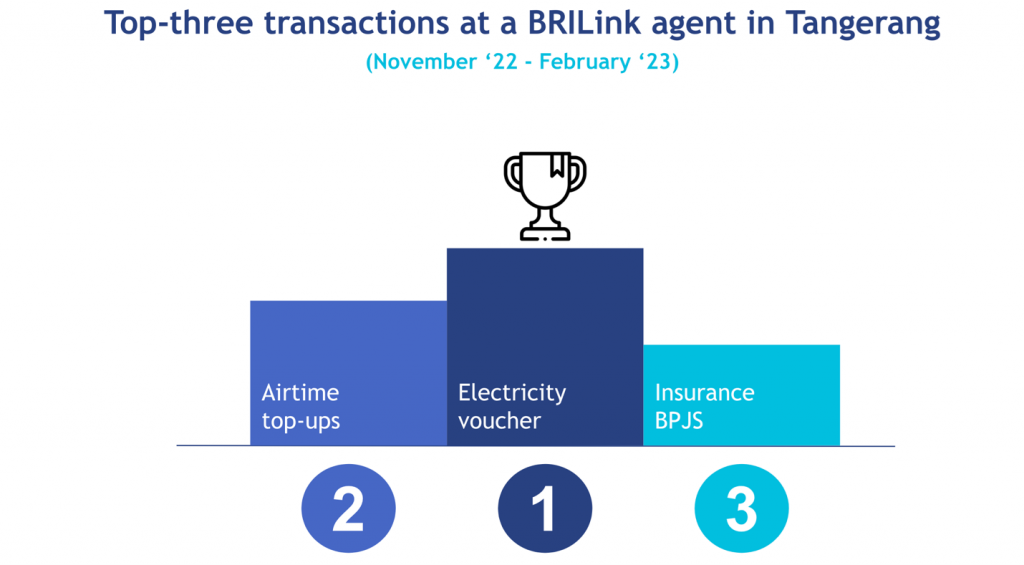

Starting in June 2022, we gradually onboarded three cooperatives under the Women Digital Ambassador project in Tangerang, Bantul, and Karawang regencies. We partnered with BRI (Bank Rakyat Indonesia) to connect the BRILink agents to women’s cooperatives and bring financial products and services to women in rural areas. Our agent in Tangerang has regularly served customers from cooperative members and the public. Monthly, they conduct ~114 transactions.

Photo 1. Ibu Neng, the BRILink Operator in Tangerang

We plugged in MSC’s Datin app to make monitoring and evaluation more effective. The app helps MSC supervise the flow of transactions conducted by each agent remotely. We found out that linking women’s cooperatives to agent networks presents unique challenges:

- Cooperative members must reach a consensus for careful decision-making

Unlike retail-based agents, onboarding a legal entity, such as a cooperative, to the agent business requires more documents. Onboarding cooperatives requires several signatures and IDs from the cooperative’s management. The service provider’s staff helped ease the process and tailor different criteria to the specific conditions of each cooperative. of criteria was also made regarding support and the type of device used. For cooperative members, the service provider gave an electric data capture (EDC) machine from the beginning of the application process, unlike the other agents that began with the mobile application, BRILink Mobile.

Getting consensus from cooperative members on the agent onboarding process also took time. The addition of BRILink to the cooperative features is considered a new business unit in the organization. Therefore, members have to agree and commit to growing the business further. Members also decided to re-invest the profits from BRILink transactions into the cooperatives’ account, which will be distributed at every year-end as part of the dividend.

Photo 2. BRILink agent in Bantul, Yogyakarta, with our Women Digital Ambassadors

- Modalities for BRILink operators’ candidates include: digitally savvy, committed, and trustworthy

The cooperative boards selected the operators from active members. Ideal candidates had to have a good reputation, be honest, and be sociable. They also had to have no issues with moving around to do their job, which also broke from the social norm where women are usually embedded with familial responsibilities and norms that limit their operational capabilities. Most of our agent operators know how to ride a motorbike, so they can hop from one cooperative group meeting to another to complete the transactions.

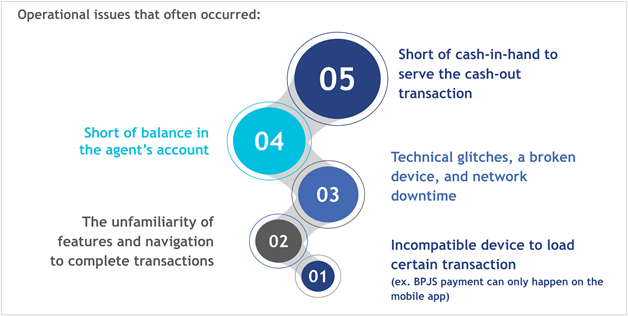

Although relatively tech-savvy, the operators still need close support from the provider’s staff to overcome technical glitches. We created a group chat among agents to allow them to discuss issues and experiences to smoothen the onboarding and familiarization process. Agents also need to practice soft skills to serve the customers, especially women—a skill equally crucial to the technical understanding of the operations. Agents must be equipped with complaint-handling and conflict-resolution methods. The operators have to balance the two aspects to acquire and retain customers.

Photo 3. An operator conducts a transaction during group meeting

- The high mobilization of agents helps extend their reach instead of depending on walk-in customers

Although cooperatives have an office premise, in this case, cooperative members seldom transact over the counter. Transactions usually occur during group meetings. Thus operators should proactively seize opportunities by attending various group gatherings to achieve the transaction target.

Although most agents are mobile, we also equip the premises with BRILink branding and signage to gain walk-in customers from the surrounding neighborhood. Our observations showed that WhatsApp and Facebook are popular among community members. Thus, we designed an e-flyer for circulation online to gain customers and spread awareness. The flyer advertised that the cooperative now offers certain financial services.

- Liquidity and rebalancing become constant issues when agents start operations.

Considering the account is under the cooperative, topping up the working capital requires approval from the cooperative head. The distance between the agent and the nearest bank or ATM also hinders the agent from regular rebalancing. This additional layer of the process affects timely transactions. Operators sometimes pause their business and turn down potential transactions when they rebalance liquidity.

“With only IDR 3 million capital, I struggle to plan the right times and frequency for rebalancing. I usually go to the nearest bank up to five times a month for rebalancing and spend around IDR 10,000 per visit. Sometimes, I ran out of balance when the bank is already closed, so I had to use my money to conduct transactions.” —WDA agent in Karawang

Photo 4. E-flyer for circulation through WhatsApp group and road signage at BRILink Bantul

However, when the number of transactions grows, operators become familiar with the rebalancing issues and start forecasting the cash-in-hand and the amount of money in the account to prevent a cash deficit.

- Increasing the volume of transactions means a growing amount of capital is needed to operate the business.

After operators found ways to cope with rebalancing issues, they indicated that the cooperative struggled to inject more capital into the agency business due to a lack of cash. The agent in Tangerang, for example, started with IDR 3.5 million, but after a few months of operations, the amount increased to IDR ~10—15 million. However, this amount remains insufficient to cater to large transactions, and agents must rebalance it frequently to ensure sufficient cash-in-hand and floating balance. Although the provider offers an agent lending product, only high-performing agents can access the loan. Therefore, flexible, short-term financing options can help new agents scale up their operations.

“We started with a small amount of capital because the cooperative wanted to see how this new business ran. We feared investing many of our members’ savings in something unproven. We will monitor the number of transactions and increase the amount of capital gradually when it is needed.” —A cooperative leader in Bantul

- Financial product cross-selling is possible thanks to the network of cooperative members.

The provider could promote and sell financial products, such as savings and insurance, to the group members through the network and members of cooperatives. For example, in Karawang, a top-rated product is savings for children that target cooperative members who enroll their children into PAUD (early childhood education center). In Tangerang, intensive socialization and promotion led to a new batch of customers for the employee social security insurance (BPJS Ketenagakerjaan). As the transaction and the customer base grows, agents can serve as referrals for their cooperative members who need microloan product (KUR – Kredit Usaha Rakyat) applications. Agents will receive an incentive for every successful loan application.

Way forward

Linking agent banking to women’s cooperatives helps them expand their capacity by building their trust and confidence in digital financial services. The women’s cooperative members can use their voice and show their agency in making financial decisions through banking services “closer home,” transacting in their reliable cooperative community. The concerted effort to deploy women as banking agents has helped bridge the rural gender divide in financial inclusion. Female banking agents can now serve more women in their locality, overcoming some of the social and cultural hindrances that prevent women from performing financial transactions.

Nevertheless, Women Digital Ambassadors need to build profitable and sustainable businesses urgently. In the days ahead, alongside mentoring and coaching for women to run the business well, providers should use gender-intentional approaches to design products and services suitable for women’s needs and context, especially in rural areas. This combination of practices can yield positive outcomes to achieve the target of 90% financial inclusion for Indonesian women by 2024.

Written by

Leave comments