How we can tackle dark patterns in India’s digital economy

by Surbhi Sood, Priyal Advani and Srinivas Balakrishnan

by Surbhi Sood, Priyal Advani and Srinivas Balakrishnan Sep 12, 2025

Sep 12, 2025 5 min

5 min

India’s digital boom hides a silent threat: dark patterns. These manipulative designs trick users into hidden fees, data grabs, and unfair choices. Tackling them needs stronger regulation, ethical product design, third-party audits, and empowered users. India can lead globally by building a digital ecosystem that is fast, fair, and trusted.

In the village of Deori in Jharkhand, domestic worker Malti Devi tried to transfer money through a mobile app, but the amount deducted was more than she had expected. She shared, “At the bank, they told me that I must have missed a button or a message about extra charges at the bottom, but I did not see anything like that on my screen.”

Malti Devi’s experience is part of India’s broader digital transformation story. The country’s digital economy has transformed lives. Affordable smartphones and faster networks have enabled 969 million Indians to access the Internet. Millions rely on apps for payments, savings, credit, and investments. These platforms are fast, convenient, and increasingly central to our financial lives.

Yet hidden within this convenience lies a troubling reality called dark patterns, manipulative design choices that trick or pressure users into decisions against their best interest. Dark patterns can compel users to sign up for unwanted services, pay hidden fees, or share more data than they intended. These often-invisible traps erode trust in digital finance.

Key takeaways:

- Dark patterns are designed to confuse, pressurize, or trick users.

- Financial harm and loss of trust are rising in India’s digital economy due to these practices.

- Stronger regulation, ethical product design, and user empowerment are urgently needed.

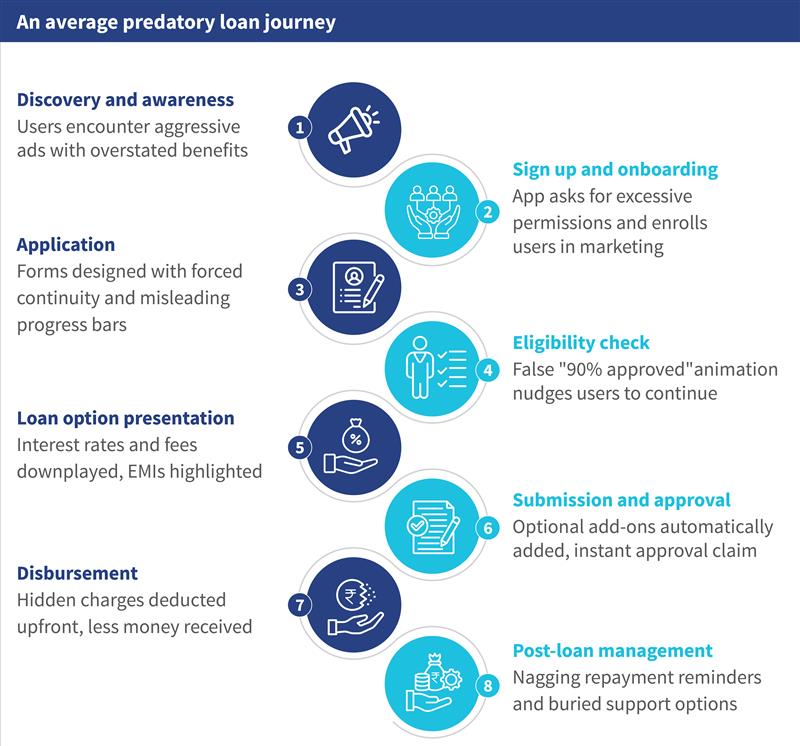

The hidden traps behind the screen

Imagine you open an app in an emergency for quick credit and instead encounter unclear fees, surprise debits, or threatening payment reminders. A woman from Kerala said, “I just needed help, and I ended up paying more than I borrowed.” She is not alone.

Across India, app users report:

- Loan and investment apps pressure customers with pushy notifications (“Your INR 90,000 loan is pending approval”)

- Payment apps hide critical options in fine print.

- Consent for data sharing is buried under layers of confusing screens.

MSC’s recent research shows dark patterns have multiplied, which has left ordinary users to shoulder the consequences. Global studies find that two-thirds of online services use at least one such tactic. In the UK, misleading subscriptions cost families nearly GBP 688 million (USD 928 million) annually. In India, numbers are less visible, but given the ubiquity of dark patterns, the impact is massive on both consumers and providers worldwide, who, according to MSC, lose more than USD 231 billion due to eroded trust and early exits.

India’s regulatory gaps

The Reserve Bank of India (RBI) has cracked down on illegal lending apps, while the Ministry of Consumer Affairs has acted against unfair trade. Yet gaps persist:

- Many dark patterns, such as pre-ticked consent boxes, hidden fees, and hard-to-find opt-outs, escape regulation;

- Enforcement remains fragmented across the IT Act, the DPDP Act, and consumer legislation.

- Excessive reliance on self-regulation (“companies audit themselves”) allows manipulation to outrun oversight.

Another MSC research highlights the need for stronger enforcement, clear multilingual design standards, and rules that actually help users rather than just satisfy compliance checklists.

What India needs to do

Regulators must act first to build a safer digital ecosystem. Their oversight should extend beyond lending apps to cover payment and investment platforms. Independent audits of disclosures and consent flows must be mandatory, while national design standards for user interfaces should establish clear and enforceable rules.

Meanwhile, accountability should not rely solely on self-certification. Instead, third-party audits can signal compliance and rebuild user confidence. Once, financial literacy campaigns taught people how to calculate interest; they must now equip citizens to recognize manipulative design. Laws across the IT Act, the DPDP Act, and consumer protection frameworks must also be harmonized to eliminate overlapping jurisdictions and resultant loopholes.

Service providers have their own role to play. They must embed ethics into the design process to ensure that it is as easy to exit a service as it is to sign up. Regular sludge audits, conducted with independent oversight, should identify and eliminate manipulative practices, with findings shared publicly. Every digital screen where financial decisions are made must offer users clear grievance resolution mechanisms so that help is only a click away. Most importantly, product and design teams must receive training in digital ethics to move away from growth strategies that prioritize downloads and clicks at any cost.

Consumers are also not powerless. They can report suspicious apps and manipulative practices through the RBI’s Sachet portal or the National Consumer Helpline. Before customers download or make a transaction, they can consult independent reviews on platforms, such as Consumer VOICE India, and share their experiences to alert others. Most importantly, customers must pause before they react to urgent prompts for loans, investments, or subscriptions designed to push them into hasty decisions.

Policymakers and development agencies can strengthen these efforts by legally recognizing dark patterns. They should define and prohibit dark patterns within consumer protection and data privacy statutes. India also needs its own multilingual design standards that are tested locally and updated regularly to keep pace with evolving manipulation tactics. At the same time, the country needs to encourage innovation that works against manipulation, such as AI and machine learning tools that can detect dark patterns in real time.

The technology and design community can potentially drive a cultural shift. They can codesign workshops with NGOs and consumer groups to test financial platforms for manipulation and feed evidence back into regulatory reforms. The community should also promote ethical innovation, which would allow India to lead in FinTech and stand out as a global champion of fair and transparent digital design.

A collective response

Dark patterns thrive in opacity, which exploits gaps in awareness and regulation. A focused collective response from regulators, industry, civil society, and consumers is required to tackle them. This will ensure that users can trust the innovation.

If India can combine stronger oversight, clearer design standards, and empowered users, it can build a digital ecosystem that protects the most vulnerable while sustaining growth. In doing so, India has the chance to set a global benchmark for a financial system that is fast, convenient, fair, and fundamentally ethical.

MSC in action

MSC (MicroSave Consulting) works with FinTechs, regulators, and user groups to develop ethics-based design toolkits and run pilot audits of app interfaces. This is to help promote India’s leadership in trusted digital finance. Explore our wealth of research on digital trust and dark patterns here.

A collective response and path forward

Dark patterns thrive on user confusion and regulatory ambiguity. To tackle them is everyone’s job: regulators to set rules, providers to act responsibly, civil society to watch and advise, and users to speak up.

India’s digital financial ecosystem should be innovative and ethical. The country can protect its most vulnerable, strengthen the whole sector, and set a global standard for fairness and integrity through transparency, accountability, and empathy in design.

Leave comments