Choosing An Agent Management Model

by MSC

by MSC Feb 7, 2014

Feb 7, 2014 5 min

5 min

One important question service providers have to ponder prior to entering the market is the agent hierarchy structure. Adopting a model which fits the market will save time, and money, and reduce stress levels for Senior Executives! The three models below illustrate the most common options available for service providers: The Direct Agent Hierarchy Model enables […]

One important question service providers have to ponder prior to entering the market is the agent hierarchy structure. Adopting a model which fits the market will save time, and money, and reduce stress levels for Senior Executives!

The three models below illustrate the most common options available for service providers:

The Direct Agent Hierarchy Model enables the provider to have direct access to agents interfacing with end-user customers. The provider takes responsibility for the operational support and oversight of the agents and ensures overall quality of the agent network. The aspects that service providers control include those which relate to individual agents as well as to the network itself. These attributes pertaining to individual agents that the service providers manage include the agent profile, physical layout of the outlet, stock keeping levels, liquidity, quality of branding etc. The network related aspects pertain to capillarity of spread – for instance, the number of agents in a locality, the factors which determine the presence of an agent in the locality etc.

The Direct Agent Hierarchy Model enables the provider to have direct access to agents interfacing with end-user customers. The provider takes responsibility for the operational support and oversight of the agents and ensures overall quality of the agent network. The aspects that service providers control include those which relate to individual agents as well as to the network itself. These attributes pertaining to individual agents that the service providers manage include the agent profile, physical layout of the outlet, stock keeping levels, liquidity, quality of branding etc. The network related aspects pertain to capillarity of spread – for instance, the number of agents in a locality, the factors which determine the presence of an agent in the locality etc.

Who Uses it: Safaricom’s M-PESA started off with this model, Equity Bank in Kenya currently uses it.

Pros: Banks often favour this model because it gives the provider the most direct control over the network, which can appease regulators, enable the offering of more complex products, and direct the most commissions directly to agents without a middle management taking a cut.

Cons: The major drawback is this model is extremely difficult to scale quickly. Moreover, under this model, service providers could potentially get bogged down with operational issues which are often better managed by, and easily outsourced to, a tier of aggregators or master agents. This level of middle management also often has better market visibility and can more accurately direct where new agencies should be best placed.

The direct agent hierarchy model could potentially be appropriate for smaller markets and providers with gradual growth strategies or limited ambitions (banks just trying to decongest banking branches for existing customers.)

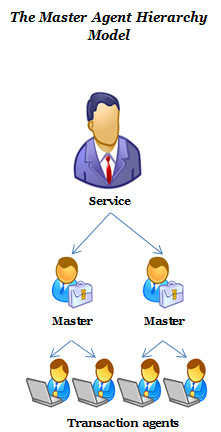

The Master Agent Hierarchy Model, is often incorrectly labelled the “aggregator model”, and is probably the most popular. In this model, the provider appoints a select number of ‘master agents’ who have proven financial and operational muscle to handle recruitment, operational support and management of field level transaction agents. The earnings of master-agents will be a proportion of the earnings of the agents they manage.

The Master Agent Hierarchy Model, is often incorrectly labelled the “aggregator model”, and is probably the most popular. In this model, the provider appoints a select number of ‘master agents’ who have proven financial and operational muscle to handle recruitment, operational support and management of field level transaction agents. The earnings of master-agents will be a proportion of the earnings of the agents they manage.

Who Uses it: Tigo Pesa (Tanzania); Airtel Money (Kenya); bKash (Bangladesh)

Pros: This model is streamlined for growth, and often telecoms just activate the agent network structure they have existing for airtime distribution to also serve as cash-in/cash-out (CICO) agents The model also minimises operational costs to the provider, as the cost is usually taken out of agent commissions.

Cons: However, this also means that the extent of control over the agent network is lower than the direct agent model. There is a management level between the provider and the customer touch point, meaning that monitoring has to be done on more levels, there are more incentives to align, and the ecosystem is one level more complicated for everyone.

The master-agent model is appropriate for the larger, more developed markets where scalability of the agent network is considered a competitive advantage.

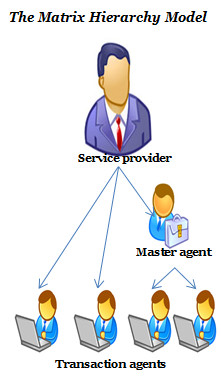

The Matrix Hierarchy Model in its most basic form is a combination of the direct agent and master agent models in a single deployment. Providers manage some strategic agents directly while delegating control of others to master agents. A number of deployments have found the benefit of this structure including Safaricom’s M-PESA.

The Matrix Hierarchy Model in its most basic form is a combination of the direct agent and master agent models in a single deployment. Providers manage some strategic agents directly while delegating control of others to master agents. A number of deployments have found the benefit of this structure including Safaricom’s M-PESA.

Who Uses it: Dutch-Bangla Bank (Bangladesh), MTN Money (Uganda); M-PESA (Kenya & Tanzania)

Pros: With this hybrid model, providers can more incisively choose between quality and quantities of agents in different sub-areas of a country. They can also easily create centres of excellence, where customers can go when they know they need to make a big transaction or do a reversal, and where agents can do with questions, or to do some operational tasks like rebalance.

Cons: It is much harder to clearly define roles and responsibilities so that all operations are covered, yet nothing is unnecessarily redundant. Further, there will likely be different reward systems and KPIs which will have be aligned and managed with sophistication.

The matrix model is suitable for those with a sophisticated head office that can run complex management systems and are planning to offer an array of sophisticated products to different demographics and need a maximum amount of flexibility in their management model. It is also used in embryonic stages of development where the provider is not sure yet which model to choose and so tries a little of the top two.

Needless to say, all the models have their own sets of benefits as well as challenges. As a rule of thumb, I would put my money on the Matrix Hierarchy Model in the initial stages of the agent network roll-out, and then consider introducing other models progressively, if need be. It provides service providers with the benefit of ‘having their cake and eating it’!

Whichever the model providers pick, arriving at that decision quickly is quite critical. The benefit of determining the agent hierarchy model early is that it has a direct correlation to the agent reward structure, taking into consideration the various intermediaries in the food-chain. By extension, the model adopted has the potential to influence all aspects of the business, including but not limited to strategic planning, pricing, process design, user interface, product attributes etc.

Kimathi Githachuri is Head of The Helix Institute of Digital Finance. As an expert in digital financial services, he previously worked as: Head of Mobile Money at Warid Telecom in Uganda (GSMA Sprinter), Mobile Money Channel Development Manager at Airtel Kenya and Area Sales Manager at M-PESA where he helped build the M-PESA network.

Extra Reading:

- For additional discussion of now MNOs structure agent networks see MicroSave Briefing Note # 136 Structuring and Managing Agent Network – I

- For additional discussion of now banks structure agent networks see MicroSave Briefing Note # 137 Structuring and Managing Agent Network – II

Leave comments