Building and sustaining agent networks – Evidence from Indonesia

by Ghiyazuddin Mohammad and Grace Retnowati

by Ghiyazuddin Mohammad and Grace Retnowati Jul 3, 2014

Jul 3, 2014 6 min

6 min

This blog presents the insights to deployments in Indonesia to design, build and implement well- functioning agent networks for delivery of formal financial services to unbanked and under-banked Indonesians.

Indonesia is the world’s fourth most populous democracy with a population of 238 million people. An archipelago with more than 17,500 islands, the country is rich in cultural, ethnic, religious and linguistic diversity. However, access to formal financial products/services still remains elusive for most people. According to World Bank estimates only 20% of Indonesians (above 15 years) have an account with a formal financial institution. The country has relatively lower bank branch and ATM penetration with 10 branches and 36 ATM respectively for every 100,000 adults.

The Government of Indonesia and the regulators (both Bank Indonesia – the central bank, and Otoritas Jasa Keuangan (OJK) – the financial services authority that regulates and supervises financial services activities in banking, capital markets, and non-bank financial industries) recognize this fact. Both have been proactive in efforts to extend financial access to the poor and unbanked sections of the society. Bank Indonesia, the central bank of Indonesia, has recently issued electronic money regulations and OJK is expected to release the branchless banking regulations by the end of the year.

In the light of this, MicroSave conducted a nationwide study on “Building & Sustaining Agent Networks for Branchless Banking/Digital Financial Services”.The research was commissioned by e-MITRA (USAID’s Mobile Money Implementation Unit in Indonesia) and Visa to support the rollout of Digital Financial Services (DFS) in Indonesia. The main objective of the research was to identify support requirements and expectations that agents have for agent management (such as training, support services, marketing, communications, etc.)

In order to ensure diversity among the respondent profiles/businesses, we interviewed various institutions and individuals such as: organized retail (multi-brand) outlets, government entities, wholesalers/distributors, rural banks, cooperatives, SMEs, corporates, individual mom & pop stores, airtime sellers and community leaders.

The highlight results show that the challenges and concerns of Indonesia’s agents are similar to those across the globe, suggesting that the core issues facing agent network managers are similar across many, if not most, markets. We go into further detail on these when The Helix Institute of Digital Finance undertakes the Agent Network Accelerator research in Indonesia at the end of 2014.

Likes and dislikes:

Respondents liked the facility of banking within the neighborhood offered by digital financial services (DFS), which enables the customers to conduct financial transactions within their community. Also, they appreciate the fact that they can transact at a time convenient to them. We have observed that most of the branchless banking/mobile money transactions are conducted outside the banking hours i.e. before 10 AM and after 5 PM. This is because the customers find it convenient to transact outside their work/office hours.

On the other side, the risk of fraud and cash handling figured prominently in dislikes of DFS. This is understandable because – 1. The concept is new and relatively unknown to many Indonesians; and 2. Fraud is indeed a big risk as we have seen in other deployments across the world. Research conducted by The Helix’s Agent Network Accelerator (ANA) survey shows that the risk of fraud remains the biggest agent management issue. We have discussed this extensively in our blogs – “Challenges to Agency Business – Evidence from Tanzania and Uganda (Part- I)” and “Why Rob Agents? Because That’s Where the Money Is”. This highlights the need for effective risk management practices, and more importantly of educating agents and end users about the risk/fraud management. See MicroSave’s “Fraud in Mobile Financial Services” for a comprehensive classification of risks and effective mitigation mechanisms.

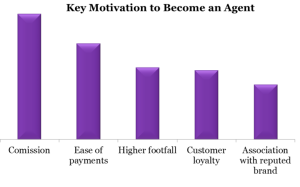

Motivation to become an agent: Commissions remain the key motivator to become an agent.

Increased customer footfalls and customer loyalty also act as important motivators. Respondents feel that they could get more customer walk-ins if they become DFS agents, which could in turn lead to higher cross-selling. They also feel that association with a reputed brand (of bank/MNO) could lead to higher customer loyalty.

Interestingly, ease of payments also figures prominently as the second most important motivator. Our research shows that 99% of the transactions still take place in cash. With huge volume and value, digital payment services provide good potential for deployments in Indonesia.

“My customers can purchase goods and use the system for payment rather than bring loads of cash”- Hamid, a retailer from Kutai Timur, East Kalimantan, Indonesia.

Requirements for Support:

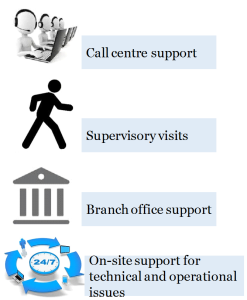

Agents are the first point of contact for the customers. So it is important to provide adequate support to the agent to deal with customers/customer queries. Respondents suggest that the deployment should provide: call center support for agents and customers; supervisory visits; branch office support; and on-site support for technical/operational issues. These services are essential to increase the adoption by agents and customers, especially during the initial stages of deployment.

Our experience of working with other deployments across the world reiterates the importance of having separate helplines for agents and customers. Deployments often provide remote support to frontline agents through call centers. Call centers can also be helpful in addressing queries or grievances that customers may have. They can also be effective means to market the products, introduce special offers and take feedback on services offered. Equity Bank in Kenya recently conducted a huge marketing campaign to launch its m-banking product. Their call center played an important role to measure the effectiveness of various media channels used and provide inputs for future marketing strategy. See MicroSaveBriefing Note #129 on Customer Support for E/M-Banking Users. Other successful deployments such as WING Cambodia, M-Pesa and Eko have a toll free number that customers can call to seek answers for their queries and register complaints if any.

Training Requirement:

Training Requirement:

Agent training is a powerful tool to drive agent performance. Many agents have no/little exposure to selling or offering financial services, and of course, training is an important tool for the management of risk and fraud.

Respondents in the research felt that agents need training on product, technology, cash management, customer education, and regulatory related aspects.

As digital financial services are a relatively new concept in Indonesia, deployments need to focus a lot on training and education initiatives– both for providers’ internal staff and the agents. In addition, specific emphasis needs to be placed on customer education (marketing) in order to educate both agents and customers about the benefits of the service. Regulatory aspects – specifically related to authentication, KYC, fraud detection and money laundering should also be incorporated into agent training. See MicroSave Briefing Note #135: Training E/M-Banking Agents: What is Missing?and#138 Implementing Training for E/M-Banking Agents.

Our research suggests that mobile and internet usage among the respondents is particularly high with 61% of them using mobile for internet browsing. Evidence suggests that 48% of regular internet users in Indonesia use a mobile phone to go online – which, perhaps surprisingly, is the highest among its Southeast Asian neighbors. With 66% of the respondents using smartphone, increasing usage of smart-phones was also prominent during our research. A recent GSMA study shows that global smartphone penetration as a percentage of the population is expected to rise from 19% in 2012 to 32% in 2017. This makes a case for the deployments to develop smart-phone based applications which offer enhanced user experience for the customers and better growth prospects for the deployments. Some of the telco-led deployments already using smart-phone application based interfaces include GCash (the Philippines), Zuum (Brazil) and Dompetku (Indonesia).

The findings of the research provide critical insights to deployments in Indonesia to design, build and implement well- functioning agent networks for delivery of formal financial products/services to unbanked and under-banked Indonesians. Further deployments in Indonesia are uniquely placed with latent demand/huge target market on one side and an opportunity to learn from successes/failures of deployments in other geographies on the other side.

Written by

Leave comments