Innovation overkill: Why product innovation in financial inclusion isn’t always the right move

by Graham Wright

by Graham Wright Jul 16, 2014

Jul 16, 2014 4 min

4 min

Amid all the renewed talk about product innovation and a client-centric/market-led approach to financial inclusion, the author argues if we have missed important aspects for product innovations.

Amid all the renewed talk about product innovation and a client-centric (or what we at MicroSave have, for over a decade now, called a “market-led”) approach to financial inclusion, I find myself wondering if we have lost sight of two key aspects:

- The differences between market leaders and market followers

- The challenges of advancing through the product development continuum

Market leaders vs. market followers

Corporations (including financial institutions) are, by strategy, either market leaders or market followers – first or later movers. First movers do the product innovation to lead the market. They invest heavily in product development and often have an outstanding in-house capability to conduct market research and create/test innovative products or (as we will discuss below) ways of marketing and communicating existing products.

Later movers watch and copy. They sometimes struggle with the back-office systems (IT, processes etc.), but the “externals” of new products are clear as soon as they are offered in the market (even, sometimes, at the pilot-test stage). Late movers assess if the product innovation is likely to be a success in the market and respond accordingly. Of course, if they do not see the potential of a product early enough they may struggle to counter the entrenched position of first mover market leaders – as we have seen, for example in Kenya, with M-PESA.

Corporations’ product innovation strategies may vary according to geography, depending on their market position and the resources they are willing to invest in any given market. So we may see one bank leading in one market and following in another where they are relatively new entrants – or indeed copying their own across products across borders. Thus Equity Bank has largely transposed its market-leading Kenyan products into the Tanzanian, Ugandan and Rwandan markets. Once it is well established in these markets, one can reasonably expect the bank to use its capabilities to refine its existing products or develop new ones specifically for these newer markets. Market leadership and customer focus is, after all, deeply engrained in Equity Bank’s DNA.

Key takeaway: it does not make any sense at all to expect all organizations to be market leaders and undertake product innovation … indeed many are simply not geared up to be anything other than market followers.

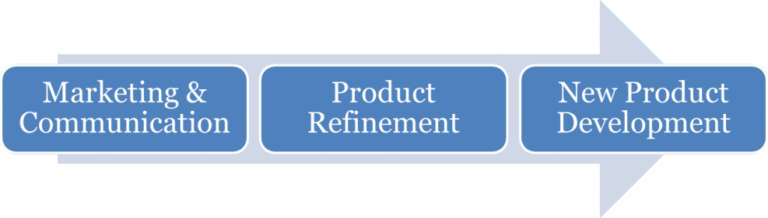

The product development continuum

MicroSave has already posted Key Questions that Should Precede New Product Development in the context of microfinance institutions (broadly defined to encompass banks, MFIs, credit unions, etc.). The same questions apply to mobile network operators (MNOs). At the core of some of these questions is the product development continuum.

Many products suffer from poor take-up because of inadequate or inappropriate marketing and communication. Across the globe, millions of potential clients are not using financial products because they do not know of their existence, or understand adequately how they might be useful. Quality market research can shed light on this, and on many other important issues that drive product uptake – see Market Research: Beyond Product Development. These insights can enable financial institutions to deepen their reach into existing market segments or reach new ones with the same product. And of course, repositioning a product with a new marketing campaign is much easier, quicker and lower cost than developing a new one.

Quality market research can also often provide important insights into minor tweaks to the delivery process or product terms and conditions. When MicroSave started working with Equity Bank (then called Equity Building Society) on product innovation in 2001, it had 109,000 customers. The first rounds of focus group discussions yielded the important insight that customers were confused by the plethora of charges that Equity levied. Within a few days, Equity had consolidated these charges into one single price and rolled out a careful communication strategy to ensure that the entire market was aware of the changes. And thus began a journey that would see Equity Building Society transform into a bank, list on the Nairobi stock exchange and become the dominant bank in Kenya, growing to serve 8.7 million customers by 2014 (see The Market Led Revolution of Equity Bank). The initial step was product refinement – accomplished with minimal fuss, and without even a pilot-test.

The final, most complex and most time and resource consuming step on the product development continuum is new product development. And it is not for the faint-hearted. Nor, as we argued in Who Is The User In “User-Centred Design”? is it something that can be easily outsourced to outsiders with a poor understanding of the marketplace, the regulatory environment, or the internal culture and systems of the financial institution. New product development requires a structured process to manage its inherent risk throughout – as we explored in the report Systematic Product Development. Due to the complexity of the process, it is often easier to follow rather than to lead.

Written by

Leave comments