Learnings from Cash Economy for DFS Providers

by Brett Hudson Matthews and Richa Valechha

by Brett Hudson Matthews and Richa Valechha May 17, 2017

May 17, 2017 5 min

5 min

The blog focuses on “Orality” which refers to the modes of thinking, speaking and managing information in societies where technologies of literacy (especially writing and print) are unfamiliar to most people.

Shakuntala is a 48-year old housewife, staying with her husband, two sons, their wives and a grandson in Siswan village, Varanasi. Her husband manages all the household expenses. In his absence, she goes to buy groceries at times. She, however, is solely responsible for purchasing clothes and jewellery for all the family members during the marriage or any other festival. Any purchase she makes, Shakuntala needs to keep an account and has to inform her husband about the expenditure. Although Shakuntala has never attended school, she is adept in counting currencies and doing basic calculations using some very concrete ways – often used by oral people.

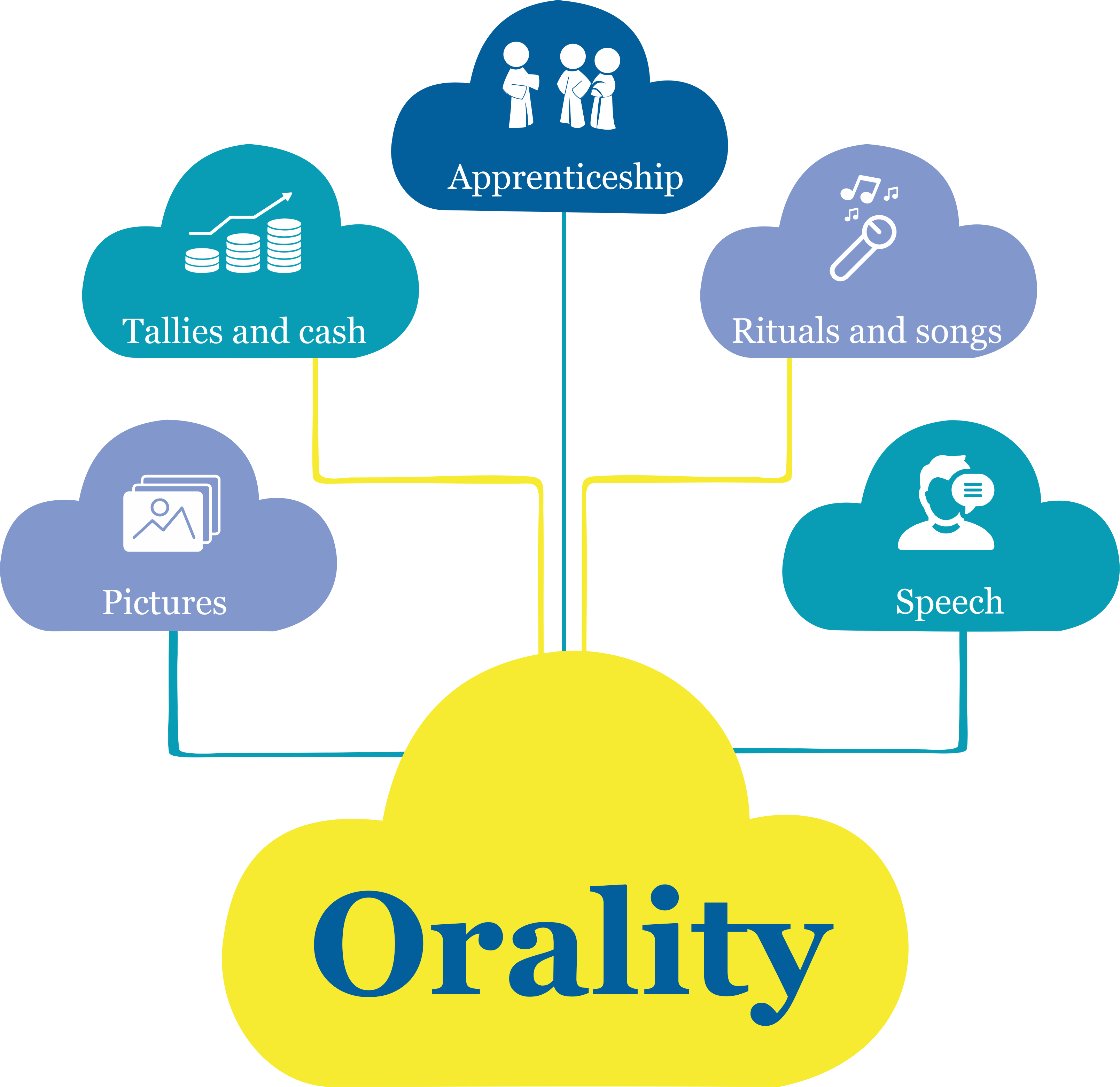

“Orality” refers to the modes of thinking, speaking and managing information in societies where technologies of literacy (especially writing and print) are unfamiliar to most people. Orality encompasses not just speech but a wide range of modes for personal and collective information management that are preferred to text in oral cultures – from pictures, tallies and cash, to apprenticeship, rituals and song.

“Orality” refers to the modes of thinking, speaking and managing information in societies where technologies of literacy (especially writing and print) are unfamiliar to most people. Orality encompasses not just speech but a wide range of modes for personal and collective information management that are preferred to text in oral cultures – from pictures, tallies and cash, to apprenticeship, rituals and song.

There is a very large ‘oral’ population like Shakuntala (either illiterate or innumerate or both) who cannot rely on pen and paper-based calculations. This forces them to mental counting and reduces their speed, especially when dealing with large numbers, as they face difficulty in decoding numeric or arithmetic notation.

To better understand both the opportunities and limitations faced by oral people in using financial services, we conducted research in different villages across three states in India – Uttar Pradesh, Punjab and Bihar. We observed that oral people get maximum exposure to numbers when they start participating in cash economy (household or personal monetisation) since this is the time when they begin to apply basic concepts of mathematics, such as addition, subtraction, multiplication and division. This helps them in money management, business and household expense management, and largely governs their financial behaviour.

Our research findings help us strengthen this observation. We have considered three parameters to evaluate the numeracy capabilities of the oral segment:

1) schooling,

2) age, and

3) gender

Basic mathematical problems based on real-life situations were asked to the oral respondents. In the first attempt, they had to calculate the problem mentally. In case the respondents gave incorrect answers or were unable to solve this problem, they were given a stack of cash to help them solve this problem. We constructed a simple indicator with a range of 0-7 (1 point for each right answer calculated mentally).

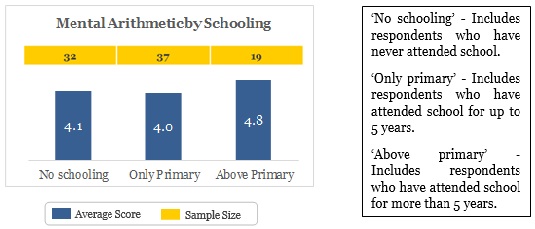

The average score was 4.2 for the sample. Neo-numerate respondents (5.0) scored substantially better than innumerate ones (3.9).

We found little correlation between mental numeracy skills and schooling. There were respondents like Shakuntala, who have never attended school but were prompt and accurate in answering questions related to basic addition, subtraction, multiplication and division. These respondents however faced problems when our team asked questions testing complex calculations, including interest rates1 and division.2

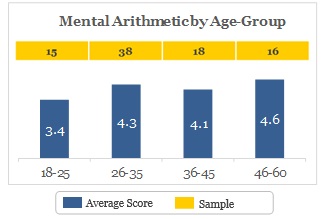

Older respondents (especially in the age bracket of 46-60 years) outscored younger ones. The question on long division was a bit complex in nature and involved some application of estimation. A direct relationship was observed among the percentage of people answering it correctly and their age-group, i.e. a high percentage of people in the higher age-group answered the question correctly.

On average, young people in the sample had weaker mental calculating skills than unschooled people, and the 16 respondents aged over 45 had mental calculating skills that were equal to those of the 19 respondents who had completed one or more years of post-primary schooling.

Females scored better than expected (3.9 out of 7) as most of them managed their household expenses and were exposed to conducting basic calculations.

Females scored better than expected (3.9 out of 7) as most of them managed their household expenses and were exposed to conducting basic calculations.

What does it tell us?

Individuals who are more actively involved in the economy (either earning money outside their home or actively managing household expenses) have less trouble dealing with numbers. Continual practice sustains or can even enhance their cognitive capabilities. For example, a labourer who paints houses must calculate input costs per square feet. A vegetable vendor must calculate price-per-quantity of different vegetables bought and sold (including spoilage) and all-in profit margin. A housewife who handles household expenses must buy groceries for the family, pay electricity bills and calculate/track total household income and expenditure. Thus, through the frequent necessity of processing numbers, costs and cash, people become quick in calculations.

Like Shakuntala, Ramesh is an oral person. He was asked a question on subtraction: You are in the market on Saturday morning, and you wish to buy a bag of rice from the shop that costs ₹780. How much change should you get from ₹1,000?

He did a mental calculation and arrived at the answer ₹320. Since he was unable to give the correct answer at the first attempt, he was handed ₹5,025 and asked to recalculate. Within a minute he did the calculation with the help of the currency and answered ₹220, correcting himself. When asked how he calculated the first time, Ramesh explained that while calculating mentally he subtracted using two steps: (i) ₹1000 from ₹700 and (ii) ₹100 from ₹80, thus arriving at ₹300 and ₹20 respectively and then he added these two numbers. He was not able to comprehend that ₹780 was a number closer to ₹800 and hence the approximate answer should have been slightly larger than ₹200.

In our field work, we found that cash was being used by oral adults as a kind of simple calculator, which gave them access to ways to calculate larger numbers than they could otherwise reach. The paper rupee banknote offers oral individuals many clues to skills that support microenterprise and household management. For example, cash involves:3

- standardised nominal values, with standardised relationships between them, which refer and evoke the Indo-Arabic number system at the base of the financial system;

- an explicit formal zero and place value;

- denomination values that operate in the useful reference range of the local economy and facilitate rapid large-number counting and processing; and

- a highly developed and established ecosystem of institutions and cultural practices and habits.

This means that the cash economy has become an informal school and reference points for mental numeracy. In this ‘school’, the incentives to pay attention in class are very high.

Does DFS solution provide learning for the oral segment as cash does?

In India, as in many countries, the cash economy appears to be more accessible to the oral segment than the financial system and economically active individuals respond by acquiring surprisingly advanced mental numeracy skills. However, their inability to read arithmetic notation restricts them from directly accessing financial services as they may still have to depend on their literate counterparts. With the advent of technology and mobile wallets being introduced, people today have access to easy and convenient banking services. Since these wallets are highly text-intensive and filled with abstract icons, their usage is limited to the literate segment and does not extend to the oral segment.

An understanding into orality in India does provide a great understanding of why some of the digital innovations (digital wallets, payment interfaces) did not achieve mass scale adoption. In the same line, it triggers the thought that digital interfaces need to be carefully designed, considering the behaviour of oral people.

1Question on interest rate: What is 100% of INR 1,000?

2Question on division: If you have to set a goal of saving ₹50,000 in 5 years. How much do you have to save each month to reach your goal?

3Matthews, Brett Hudson (2016). Oral Financial Numeracy, My Oral Village Inc., Toronto, p. 26.

Leave comments