Why do financial institutions shy away from financing farmers in India?

by Shweta Menon, Mohit Saini and Anil Gupta

by Shweta Menon, Mohit Saini and Anil Gupta Jul 15, 2020

Jul 15, 2020 4 min

4 min

This blog, the first in a three-part series, highlights the skewed penetration of formal financing for farmers in India. It also examines the challenges that financial institutions face while offering credit to small and marginal farmers in the country.

Despite an increase in penetration of agricultural credit, most SMFs continue to remain excluded

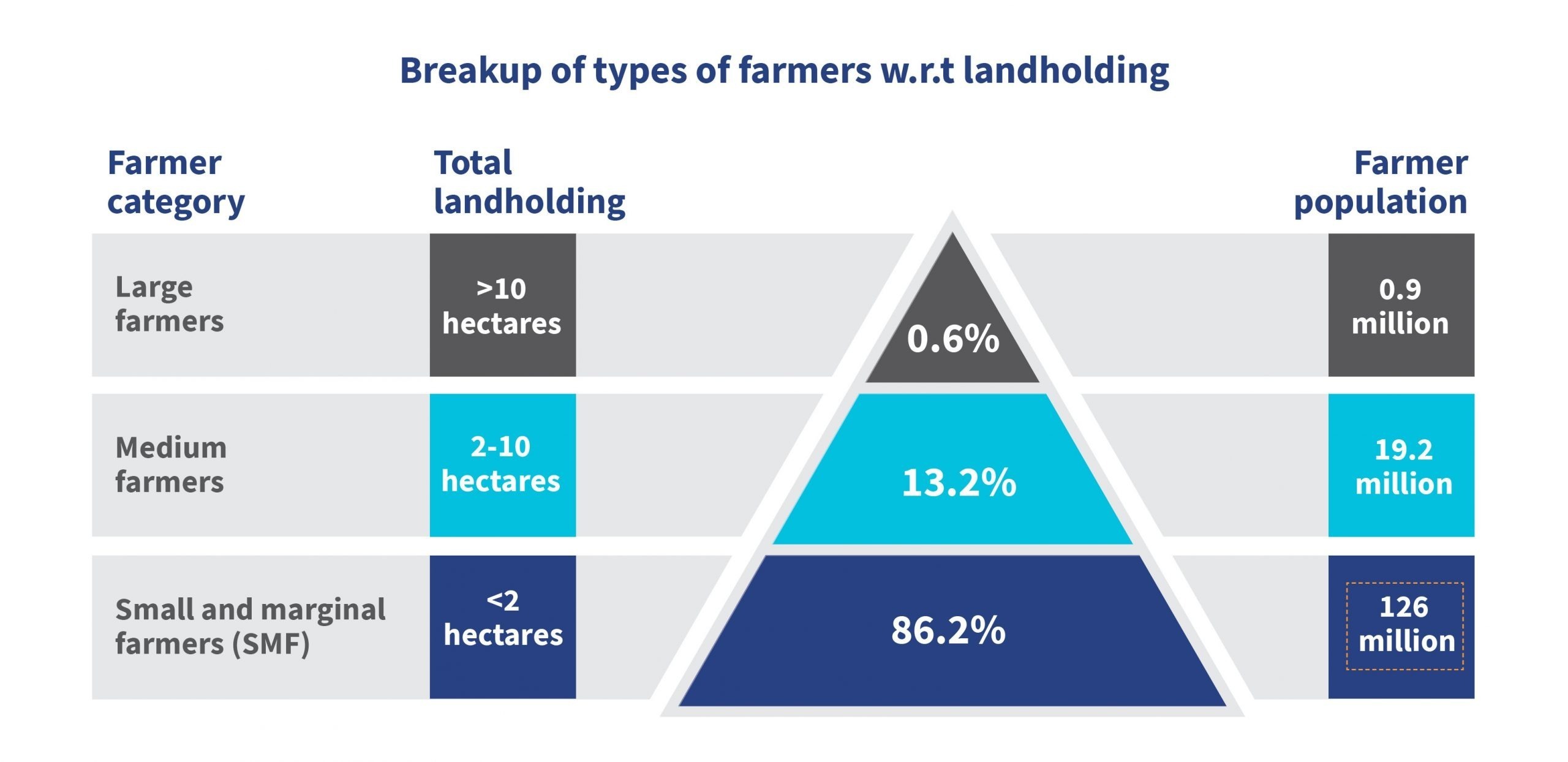

While agriculture remains a key economic activity in India, employing close to 55% of the population, most farmers find it challenging to access finance. Farmers rely on both formal, as well as informal, sources[1] to fulfill their needs for activities such as purchasing inputs, machinery, and improving the quality of their land. During the course of MSC’s study, farmers in India were divided into three categories based on the size of their landholdings. These categories included small and marginal farmers owning less than 2 hectares of land, medium farmers owning between 2 and 10 hectares of land, and large farmers owning more than 10 hectares of land.

A significant finding from this study was the disparity in access to formal and informal finance that was prevalent in the three farmer categories. Our analysis indicates that, despite the Government of India’s policy to encourage agricultural lending, only approximately 29% of farmers enjoy access to credit from formal sources. Of the SMFs, who comprise 86.2% of the total farmer population, approximately half were unable to borrow from either formal or informal sources. Of those SMFs that do borrow, 59% or 36 million accessed formal credit while 41% relied on informal credit.

Banks are reluctant to offer credit to SMFs

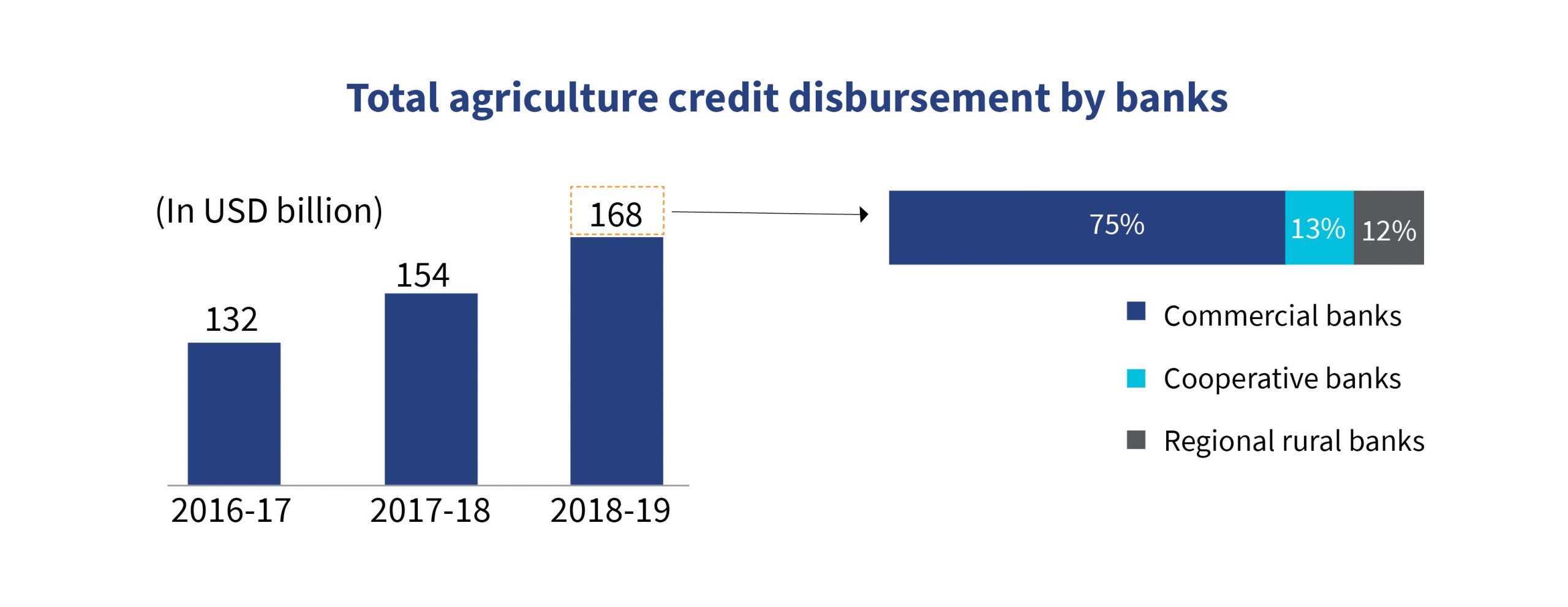

Agricultural credit disbursed by banks increased by 27% from 2016-17 to 2018-19 as a result of mandated priority sector lending (PSL) policies of the Reserve Bank of India (RBI). In 2018-19, banks disbursed agriculture credit worth USD 168 billion, three-fourths of which came from commercial banks with the remainder disbursed in equal proportion by cooperative banks and regional rural banks. All these banks disbursed nearly 50% of their credit to large farmers and were unable to meet their mandated PSL criteria of disbursing 8% of their credit to SMFs.

In India, the RBI mandates banks that are unable to attain their PSL target to either purchase priority sector loans from other banks or contribute to the Rural Infrastructure Development Fund (RIDF)[2]. As more and more banks struggle to meet their PSL targets, the sale of priority sector lending certificates (PSLCs) has gained traction. PSLCs help banks fulfill their shortfall by trading the certificates from the seller to the buyer bank for a fee. Private and foreign banks, which often lack a presence in rural areas and find it costly to lend to PSL target segments, have emerged as the predominant buyers; while public sector banks, rural regional banks, and small finance banks have emerged as the major sellers of PSLCs. As per RBI data, the trading volume of PSLCs increased by 78% to USD 44 billion in FY 2019, up from USD 26.5 billion the previous year. The sale of PSLCs for SMFs grew 62% to USD 15 billion in FY 2019 as compared to FY 2018.

Our interactions with banks during the study highlighted that their reluctance to offer credit to SMFs is driven by the following reasons:

- High cost of service: Banks find it costly to serve SMFs with low ticket-size transactions, and difficult to reach out to them as the farms and farmers are located in remote areas. Banks also perceive an inherent risk of default associated with lending to SMFs.

- Limited mechanisms to assess SMFs creditworthiness: Banks have limited access to farmers’ financial information such as cash flows and credit history. Most farmers have either had no or negligible experience banking with formal financial institutions. Further, banks are unable to verify whether the information provided by SMFs, such as income from other sources, is reliable for financing decisions.

- Uncertainty in the policy environment: Banks hesitate to serve SMFs due to the farm loan waivers offered by state governments. Since the government assumes the liability of the farmer and repays the bank in the case of default, banks feel that such loan waivers reduce the credit discipline of farmers and create a moral hazard. Loan waivers coupled with banks’ perceptions of high non-performing assets in agricultural lending make financial institutions reluctant to serve SMFs.

Banks would be remiss to disregard the potential opportunity to offer credit to 90 million SMFs, which represent a relatively untapped segment in India. Although the challenges cited above are, in part, driven by costs and the policy environment, many hurdles could be overcome with access to reliable farm-level data. This creates an opportunity for technological interventions in the agriculture sector that could improve banks’ abilities to obtain and verify farmer data resulting in greater access to finance for SMFs. In our next blog, we unpack the AgTech landscape in India and focus on technological innovations across the Agri value chain.

About the blog series

This is the first blog in a three-blog series for a study entitled the “Role of tech-enabled formal financing in agriculture in India” conducted by MSC (MicroSave Consulting) and ThinkAg, with support from the Rabo Foundation.

The second blog covers the AgTech landscape in India and highlights three key challenges limiting their growth. The third blog focuses on partnerships between AgTechs and financial institutions and offers recommendations on improving the AgTech ecosystem in India.

About the study

MSC (MicroSave Consulting) and ThinkAg studied the AgTech landscape in India focusing on innovations in financing small and marginal farmers (SMF). The study, conducted in June 2019, looked at technology-led solutions in the AgTech space and examined how financial institutions could adopt such solutions to finance SMFs. We consulted over 50 stakeholders for the study representing AgTechs, financial institutions, investors, donors, input suppliers, agri-corporates, industry experts, and incubator managers. In May 2020, the results of the study were disseminated via a webinar organized by the World Bank.

[1] Farmers rely on both formal, as well as informal sources to fulfill needs and requirements for activities such as purchasing inputs, machinery, and improving the quality of their land, among others.

[2] RIDF was set up by the Government of India to provide loans to state governments and state-owned corporations to finance rural infrastructure projects. The fund is maintained by National Bank for Agriculture and Rural Development (NABARD).

Leave comments