Why should financial institutions focus on youth?

by Doreen Ahimbisibwe, Olivia Obiero and Thomas Bariti

by Doreen Ahimbisibwe, Olivia Obiero and Thomas Bariti Sep 4, 2020

Sep 4, 2020 3 min

3 min

Financial Service Providers (FSPs) have embraced the drive to promote financial inclusion. However, many feel that the investment made in reaching out to these segments may not be commensurate with the benefits they stand to gain. In this blog, we discuss how FSPs can determine whether it is worth serving certain segments and we specifically focus on the business case to serve the youth.

The median age of Africa’s population is 19.5 years. In 2019. almost 60% of the population of Africa was under the age of 25, making it the world’s youngest continent. For this blog, we use the definition provided by the African Youth Charter for youth as any individual between 15-35 years of age.

The median age of Africa’s population is 19.5 years. In 2019. almost 60% of the population of Africa was under the age of 25, making it the world’s youngest continent. For this blog, we use the definition provided by the African Youth Charter for youth as any individual between 15-35 years of age.

Like other segments, young Africans need financial services. As per estimates by the ILO, of the 38.1% estimated total working poor in sub-Saharan Africa, young people account for 23.5%. Even though the unemployment rate of the youth in Africa is quite high, young poor workers and even the unemployed can benefit from financial services. However, 80% of youth remain financially excluded. According to the ILO and the MasterCard Foundation, Sub-Saharan Africa has the second-lowest level of formal account holders after the Middle-East and North Africa (MENA) region. Financial service providers (FSPs) struggle to serve youth profitably and sustainably because they make small, infrequent savings and have a high-risk credit profile.

Only those FSPs that are socially oriented and interested in the economic empowerment of youth or choose to focus on youth as a niche market make the effort to design and deliver youth-focused financial services. However, both youth and FSPs can benefit from each other. This is because FSPs can create a business case to serve young people and reduce costs by encouraging account usage, cross-selling products, and using technology-driven models.

Financial needs of youth

To successfully serve young people, FSPs should make a concerted effort to understand youth as a unique segment. MSC’s experience highlights that youth have personal and business-related needs. Personal needs primarily relate to lifecycle events, such as education and marriage. On the other hand, business-related needs include starting and running a business, business expansion, or capital assets acquisition, or all three. Like other segments, youth often require lump sums to meet their business-related needs since these cause the greatest financial pressure. In most cases, the youth resort to either savings or credit to generate lump sums.

Since formal financial services are not tailored to their needs, most young people rely on coping mechanisms. These include borrowing from parents or relatives and informal groups, such as Village Savings and Loans Associations (VSLAs). However, these mechanisms are limited in their nature and may not provide adequate lump sums that the youth need to raise. According to a MasterCard Foundation report, the needs for financial services become more complex as the youth become older and get more income streams. Thus, the need for FSPs to be adequately positioned to meet these needs through the years.

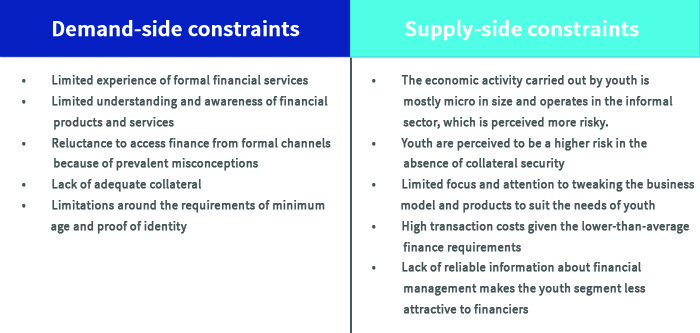

Demand- and supply-side constraints

Although the needs for the financial services for youth are not radically different from the needs of other segments, the level of financial exclusion is higher due to a combination of factors. The key constraints on both demand and supply sides that are specific to the ability of young people to access finance are as follows:

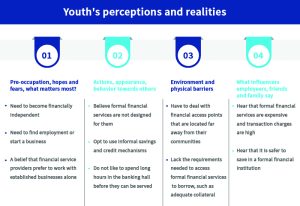

Figure 1: Youth perceptions

The perceptions and reality of youth

While the youth segment is by no means homogeneous, the perceptions and realities of young people differ significantly from other segments. The table below outlines the key differences.

Understanding these perceptions and realities enables the FSPs to serve the youth better. In the next section, we demonstrate through a business case on serving the youth by financial institutions.

The business case for financial institutions to serve the youth

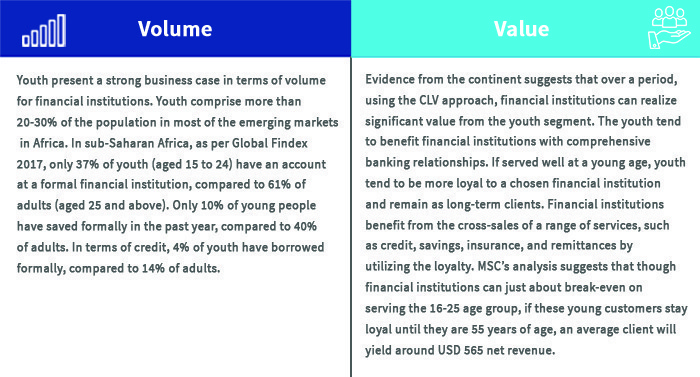

The business case for financial institutions to expand financial services to the youth is based on a combination of factors related to volume and value.

Most of the sub-Saharan African markets currently lack any market leader in this space. This offers enormous potential for formal financial institutions to develop a brand as a financial partner for youth. An institution entering the youth segment will have a first-mover advantage.

In the next blog, we highlight how financial institutions may develop and deliver appropriate products and services that suit the needs of the youth.

Leave comments