Many MSMEs are dying—can we realize the full potential of the digital revolution to save them?

by Graham Wright

by Graham Wright Apr 19, 2021

Apr 19, 2021 6 min

6 min

This blog analyzes the existential crisis that is being faced by MSMEs in the wake of the Covid-19 pandemic and goes further to explore whether exploring the full potential of the digital revolution can save them.

MSMEs are facing an existential crisis. The economic impact of the COVID-19 has been as bad as we had feared … possibly worse.

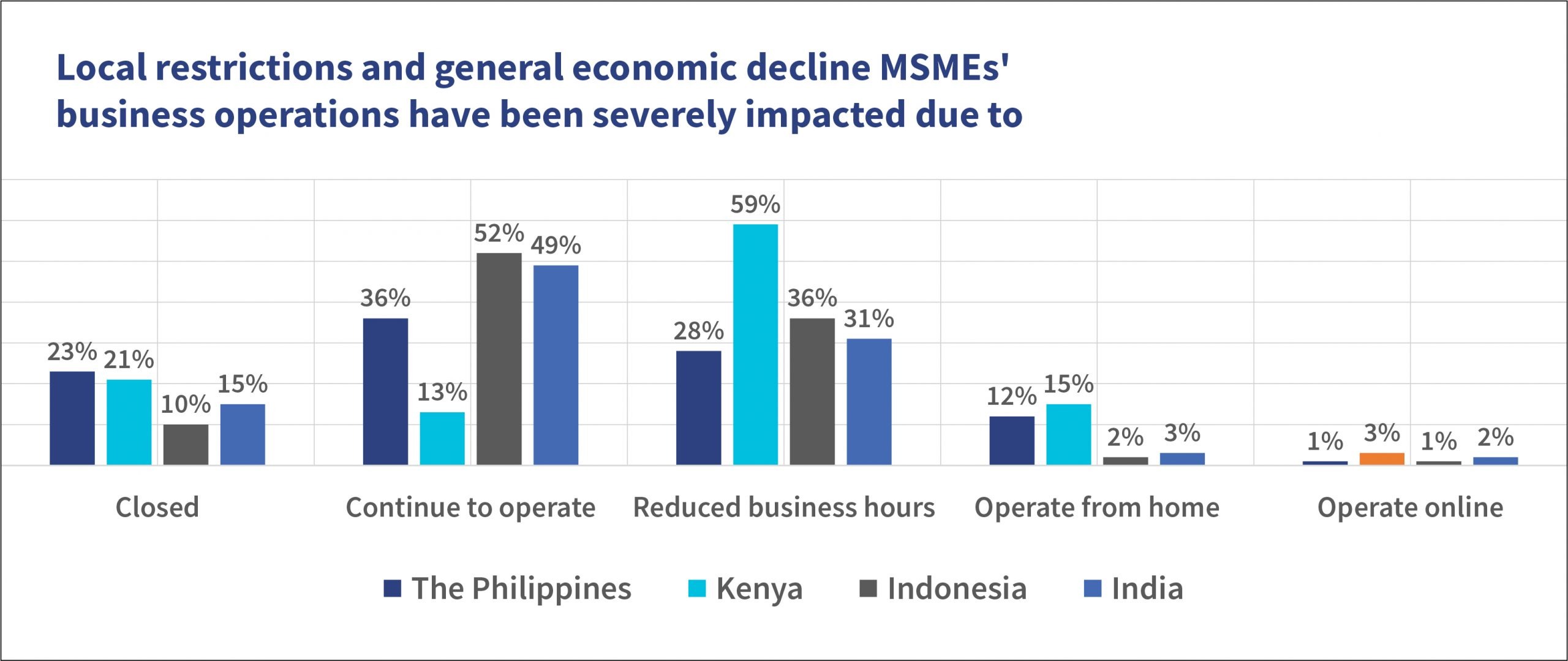

About 17% of businesses surveyed by MSC in India, Indonesia, Kenya, and the Philippines have closed due to local restrictions and low demand for goods and services, while micro and small enterprises (MSEs) in the informal sector fared worse. A recent World Bank report suggests that in Kenya, one-third of household-run MSEs have not been operating for months.

Declining income and rising expenses is a double whammy for enterprises in such trying times. On the demand side, the income of businesses declined due to reduced footfall, lower customer demand, and reduced purchasing power of customers. At the household level, MSME owners have had to pay for increased household expenses for basic goods, electricity, and the education of children. On the supply side, the factors contributing to the decline in income included disruptions in the supply chain and limited operating hours for the businesses impacted by the lockdowns and restrictions on movement.

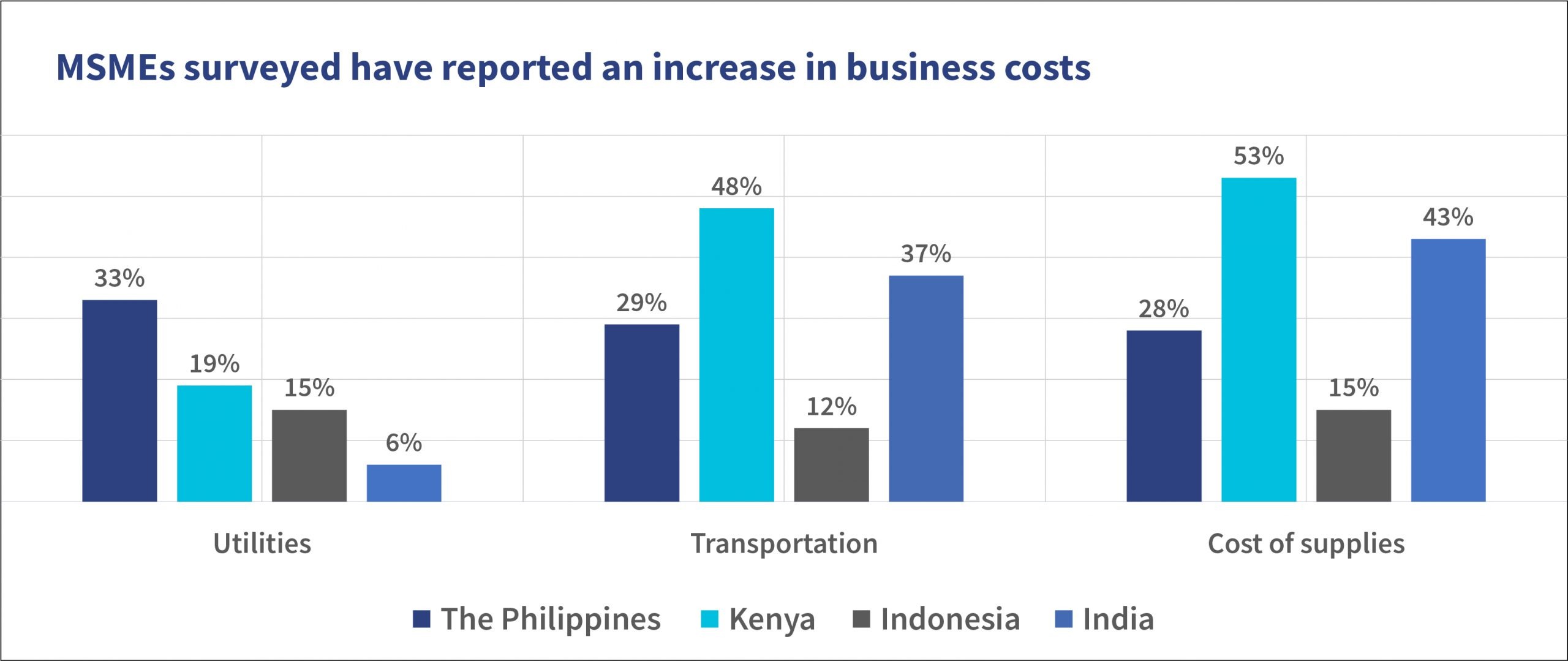

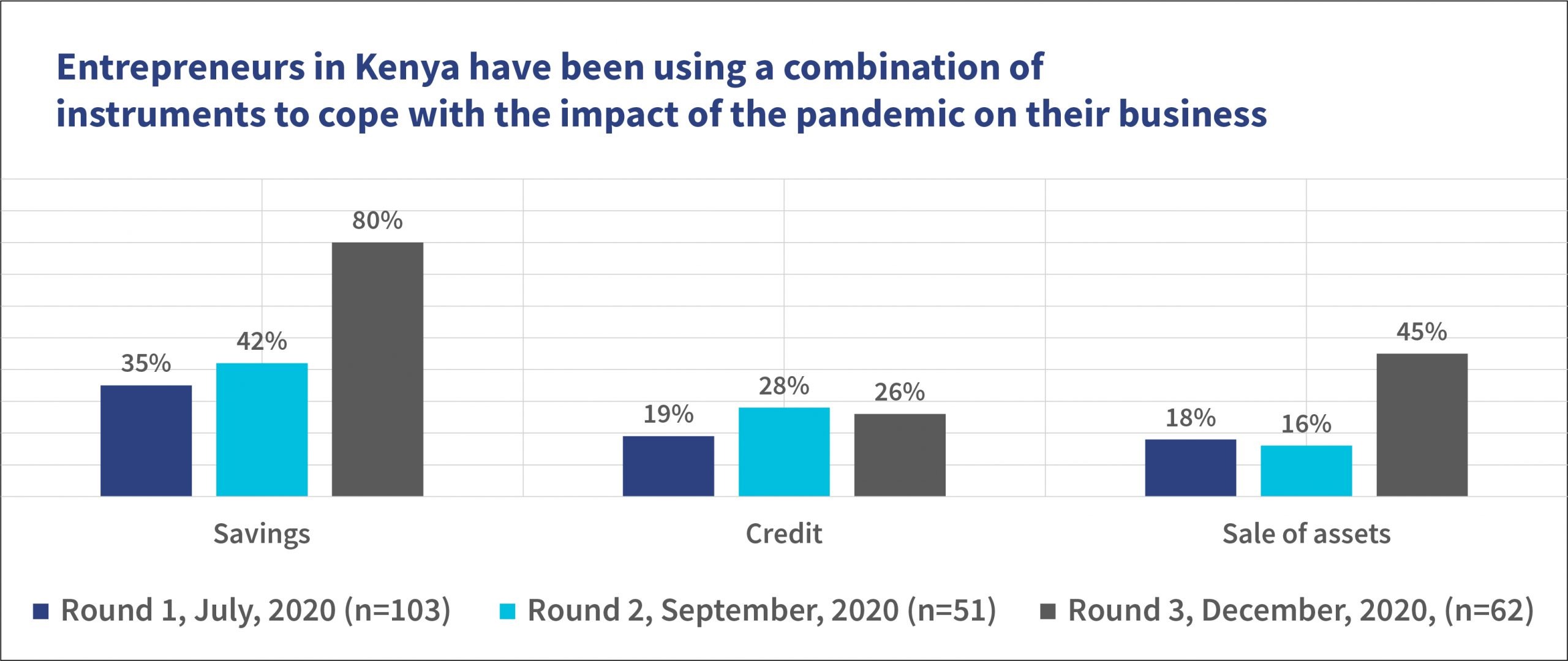

Entrepreneurs have experienced severe challenges related to cash flow. This was due to three key issues—limited access to goods on supplier credit, most sales being conducted on credit, which resulted in increasing receivables, and the rising cost of supplies. MSMEs have resorted to running down their life savings, borrowing from their social networks, and even selling off business and household assets to meet their cash flow requirements.

In Kenya, with other expenses gradually stabilizing, repayment of loans has emerged as the biggest challenge for entrepreneurs. They have been struggling to repay new loans taken during the pandemic or pay penalties on old loans, or both, due to delays in installments.

MSMEs have struggled to borrow from formal financial institutions as they encounter more stringent terms, such as higher costs of credit and requests for physical collateral. Financial service providers are also reluctant to offer loans, let alone discounted interest rates as the pandemic devastated their cash-flows. But many MSMEs need credit to be able to revive their business, restock, and survive the crisis. In December, 2020, 50% of the respondents reported that they applied for the loan compared to 39% of MSMEs in September, 2020.

This situation is not unique for entrepreneurs in Kenya and is replicated worldwide—as seen from studies by MSC and the World Bank. Both the studies note that local enterprises now have limited access to cash and credit for business. In the absence of credit for MSMEs, they will be unable to restart their businesses or reach their previous scale—as their efforts to respond to the pandemic have eaten into much of their working capital.

How has the inclusive finance sector responded to these challenges?

The response from the inclusive finance sector to this crisis has been largely traditional—and, as a consequence, we risk losing an important opportunity to “build back better”.

Governments and donors remain largely focused on traditional solutions, such as supporting microfinance institutions and credit guarantee initiatives that are managed largely by traditional banks. For example, in December, 2020, the Government of Kenya launched the credit guarantee scheme (CGS) by allocating an initial seed capital of KES 3 billion (˜USD 30 million). This approach may be necessary and relatively easy in the short run, but we should think more strategically.

We should not let this crisis go to waste. It provides us the opportunity to accelerate several interrelated transitions to allow MSMEs and the financial institutions that serve them to realize the full potential of the digital revolution.

- Formalize informal enterprises

Most micro- and many small enterprises remain informal and thus do not qualify for the stimulus packages of governments. The fallout from COVID-19 could provide the push needed for these enterprises to register and formalize. Using COVID-specific cash transfers, access to government procurement as well as credit facilities, and support for digitization as incentives, governments may encourage informal enterprises to formalize. Countries could introduce a low-touch and paper-lite registration for informal enterprises to allow them to qualify for support in the event of a disaster. Such a system would have to recognize the disincentives to formalization, in particular the entrepreneurs’ fear of falling into the tax net, and set reasonable levels of revenue for enterprises as a threshold to be taxed.

- Digitize MSME operations

The pandemic pushed some MSMEs to increase their use of digital marketing and payment channels. While the change has been more pronounced in some countries, such as India and Indonesia, it was significantly incremental in others, such as in the Philippines and Uganda. Nonetheless, formalization and the growing range of technology available to support enterprises would allow them to manage their business more effectively and create a digital footprint upon which financial service providers can make informed lending decisions. MSC’s analysis has shown, unsurprisingly, that different merchants, for example, are at different stages of readiness to make this transition.

Governments, donor agencies, and the private sector will need to work together to enhance the digital capability and the uptake and usage of digital marketing and payment systems. This collaboration will require mobile money and other digital payment providers to revisit their pricing and commission systems for both cash-in/cash-out (CICO) agents and merchants. These changes are essential to encourage the move to keep money digital and to maximize digital payments. CICO agents and merchants will need to be equipped and incentivized to utilize their position as community influencers to become agents of change. The agents and merchants are uniquely positioned to do this at the key “teachable moments” when their customers come to transact.

- Facilitate the digital transformation of traditional financial service providers

As an integral part of seizing the opportunity provided by COVID-19 to accelerate the digital revolution, financial institutions (including MFIs) must implement digital transformation. This will allow them to deliver faster and cheaper services, equip them to serve MSME customers better, and allow microfinance institutions to utilize their strengths to continue to serve rural and urban markets.

Part of these changes will be through partnerships between traditional incumbents and fintechs to help achieve the objectives of digital transformation. Governments and donor agencies should set up a lab, a community of practice, and earmarked funds that financial institutions can avail of on a matching fund basis to encourage digital transformation. Forward-thinking microfinance investment vehicles should help their investee organizations with the required matching funds to protect their investments.

- Re-engineer digital credit to focus on enterprise rather than consumer lending

Digital credit providers have the potential to play a leadership role in the response to the pandemic. They could offer rapid loans based on alternative data, particularly if they could access the credit guarantee schemes provided by a range of agencies across the globe. Yet currently, many of the burgeoning digital credit operations, particularly in Africa, are focused on the consumer rather than enterprise lending. This needs to change.

The unintended consequences of aggressive push marketing, unacceptable collection practices, borrowing for sports betting, and negative listing on credit bureaus have been profoundly negative. MSC has already made a range of recommendations on how digital credit providers can make their products more user-friendly and thus profitable. However, to realize the full potential of digital credit, providers will have to both rethink their applications, user interfaces and experience (UI/UX), algorithms, and make use of the digitization of MSMEs we advocate in point 2 above. The regulators must ensure that fintechs have a level and fair playing field and build adequate provisions to protect the end-users.

We do not want to pretend that this transformation will be easy. It will require collaboration and a huge effort from governments, donors, the private sector, and fintechs. Yet it can potentially change—at a fundamental level—how enterprises conduct their business, how they access financial services, and how well they can respond to the next crisis.

Written by

Leave comments