Decoding agriculture market linkages for FPOs: Lessons from the field

by TVS Ravi Kumar, Mukesh Kumar and Rajnish Kumar

by TVS Ravi Kumar, Mukesh Kumar and Rajnish Kumar Nov 21, 2023

Nov 21, 2023 6 min

6 min

India’s farmers have had a long history of struggle. For decades, they have battled a multitude of agricultural challenges, such as fragmented landholding, numerous intermediaries, and low value addition. In response, the country has actively promoted farmer producer organizations (FPOs) as a solution. FPOs intend to address these serious issues through the aggregation of demand for high-quality inputs, credit, and technologies and the aggregation of outputs to improve smallholder farmers’ market access. Yet despite these efforts, major processors and output purchasing companies hesitate to engage directly with FPOs. This blog explains the options available for FPOs to trade with institutional buyers and the on-ground issues FPOs must overcome to establish better market linkages.

India’s farmers have had a long history of struggle. For decades, they have battled a multitude of agricultural challenges, such as fragmented landholding, numerous intermediaries, and low value addition. In response, the country has actively promoted farmer producer organizations (FPOs) as a solution. FPOs intend to address these serious issues through the aggregation of demand for high-quality inputs, credit, and technologies and the aggregation of outputs to improve smallholder farmers’ market access.

Yet despite these efforts, major processors and output purchasing companies hesitate to engage directly with FPOs. This blog explains the options available for FPOs to trade with institutional buyers and the on-ground issues FPOs must overcome to establish better market linkages. We limit the discussion to cereals and grains, which constitute most of India’s agricultural production.

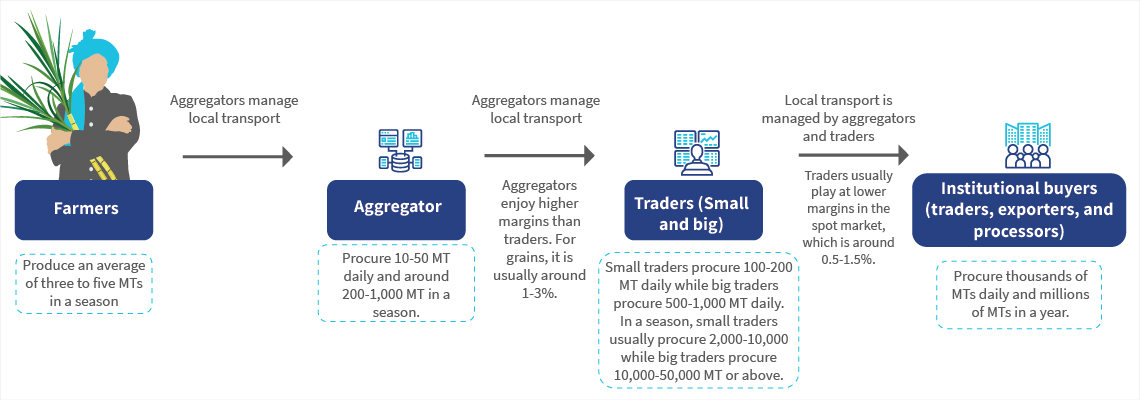

Agriculture value chain participants

We have used Bihar’s maize supply chain as an example to depict the commodities’ journey from farmers to end processors. In Bihar, farmers typically have an average landholding of only 0.38 hectares, which produces around 2-5 metric tons (MTs) of maize per season. Farmers sell more than 90% of the total produce in Bihar directly at the farm gate to village-level aggregators. These aggregators, in turn, sell the produce to small traders, who then supply it to large traders. The major processors and trading firms serve as the primary buyers for these large traders. They collectively procure millions of metric tons of maize from Bihar each year.

The intermediaries, such as aggregators and traders, are critical in the conversion of small amounts of 2 to 5 MTs into hundreds of thousands of MTs as required by the large buyers within a short period of 30-45 days. Throughout this process, the material is graded into different qualities, which allows the buyer to buy the desired grade. The following provides a generalized representation of participants in the commodity value chain.

What avenues do FPOs have to engage with large institutional buyers?

FPOs often act as substitutes for aggregators and small traders. A primary motivation behind FPOs’ formation is to bypass intermediaries and establish direct trading channels with food processors and other significant institutional firms. In this section, we have listed different trading approaches FPOs can take to deal with large buyers:

1. Daily supply based on daily prices: FPOs can engage in daily commodity trading if they receive prices every morning. Large institutional buyers typically have designated locations, such as warehouses, for delivery during the harvesting season. Under this method, the FPO receives daily prices from the buyer, factors in operational expenses, and determines the procurement price for the day. Interested farmers make deals with the FPO, which procures and delivers the produce to the buyer’s delivery center. This process minimizes FPOs’ price risk as it treats each day’s material as an independent trade. However, operational efficiency is crucial to maintain sufficient margins. For example, the FPO should plan the procurement quantity from farmers in a way that it can fill the trucks deployed. If the trucks’ space is not filled, the produce’s transport cost will increase and eat into the margins. Similarly, the quality should be good enough to ensure the trucks are accepted with no deductions at the buyers’ warehouse.

2. Large quantity trades with fixed terms (“sauda”): Another method involves the execution of large trades at a single price point within a limited delivery period, commonly referred to as “sauda.” Large institutional buyers widely adopt this method. It entails an agreed-upon quantity, price, and quality to be delivered within a fixed time. While this method allows for slightly better prices and provides a fixed price over a specific duration, it comes with risks. FPOs must meet their commitments to avoid fines or jeopardizing future trades, which makes operational maturity crucial.

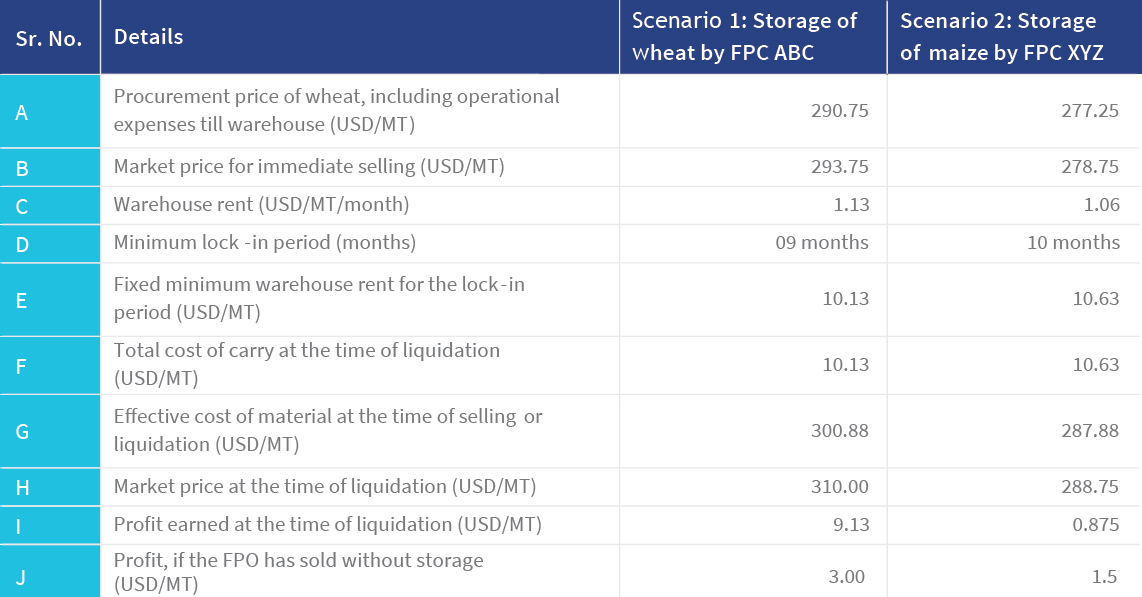

3. Storage of commodities to sell in the future: The usage of accredited warehouses for storage with the intention of future sales is often suggested to secure higher prices. However, our practical experience reveals that this approach is also the most precarious. Commodities’ storage introduces additional expenses, which include costs of carry or storage, susceptibility to market price volatility, shrinkage or storage losses, and heightened financing requirements. Professional warehouses always come with a mandatory minimum lock-in period, which significantly increases costs. This may result in FPOs achieving minimal profit margins despite price appreciation. Market price risks, influenced by global supply chains and external factors, further compound the challenges.

A comparative analysis in the table below illustrates two scenarios: In Scenario 1, FPO ABC stored wheat for nine months, and in Scenario 2, FPO XYZ stored maize for 10 months. While FPO ABC realized a profit of USD 3/MT, FPO XYZ’s profit was only USD 0.87/MT. Notably, despite the maize price appreciation, FPO XYZ experienced a reduction in profit margins due to associated storage costs. Both FPOs had internal financing. If external credit was involved, the interest rate during the storage period would have further eroded the FPOs’ profit margin.

Despite these risks, storage remains an important avenue for market linkage in regions without a significant presence of large buyers. This requires the produce to be transported to distant locations for sale to a large institutional buyer. FPOs must constantly check the arbitrage in prices available and the various costs associated with storage.

4. Delivery to distant locations or interstate transport: Large buyers often offer better rates closer to their processing units, which may be located far from the FPOs or in other states. FPOs must transport produce to these distant locations in such cases. The main risk involves quality checks at the designated delivery location. If the quality does not meet expectations, the price received may decrease, or the material could be rejected. This would lead to distress sales in unfamiliar geographies. A reliable network with transport agencies is crucial to tap into this opportunity.

What challenges must FPOs overcome to establish efficient market linkages?

MSC has highlighted the internal weaknesses that FPOs must overcome in other blogs. In the following section, we list specific operational areas that FPOs must strengthen to meet the challenges presented by the markets:

- Ensuring ruthless quality control: FPOs need to compete with aggregators and small traders through efficient procurement of the right quality at the right price. Educating farmer members in advance is crucial. Although the FPO belongs to them, it cannot compromise on the prevailing quality standards in the market. The price the FPO offers for a specific quality must align with market practices.

- Identification of different buyers for different quality: As social organizations, FPOs are obligated to buy different grades from their member farmers. Therefore, FPOs must identify various buyers for different quality grades. The FPO, Aaranyak Agri-Producer Company Limited (AAPCL), Purnea, has built relationships with many maize buyers. These include poultry feed manufacturers, who require higher quality produce; starch manufacturers, who are fine with slightly lower quality maize; and local producers of industrial ethanol, who are not quality conscious.

- Creation of suitable structures to scale: FPOs struggle to scale up as they face operational challenges, such as maintenance of procurement quality, arrangement of cost-effective logistics, and proper documentation for procurement and sales. Traditional field staff may not be a sufficient operational structure for scaling. JEEViKA-promoted FPOs have addressed this through a network of agriculture entrepreneurs (AEs). These AEs are educated youth in the villages and provide aggregation services to FPOs on a commission basis, which is linked to the quantity and quality of procurement. For example, Aaranyak FPC in Purnea collaborates with 12-14 AEs every season. This has helped the FPO increase annual maize procurement from 1,200 MT in 2020 to 4,150 MT in 2023. This approach has proven effective to enhance the FPO operations’ scale.

In conclusion, the complexities of market linkages for farmer producer organizations (FPOs) in India reveal both challenges and opportunities. We must appreciate and respect the current market structure and rules as the nation actively promotes FPOs to surmount structural issues in agriculture marketing. FPOs must overcome challenges, such as quality control, identification of diverse buyers, and creation of scalable structures, to thrive in the evolving agricultural landscape.

Leave comments