Not all youth are alike: Unveiling diverse personas of Indonesian youth in the digital landscape

by Sneha Sampath and Singgih Pangestu

by Sneha Sampath and Singgih Pangestu Nov 27, 2023

Nov 27, 2023 6 min

6 min

Our blog sheds light on the hurdles Indonesian youth encounter in accessing finance and examines how the digital capabilities of different youth personas impact their financial behavior.

“I am comfortable with basic tech, but when it comes to complex financial platforms, I think many youth still get overwhelmed.”—Maya, a university student

“I do not think so. For me, technology is a tool to find the best deals and opportunities. I use it frequently to manage my business finances and explore financial products that offer value.”—Rizky, a young entrepreneur

A brief discussion with two friends we met during the field study uncovers the varying experiences and levels of ease of many Indonesian youth who navigate technology. Youth is one of Indonesia’s largest and most influential groups. As per the BPS-Statistics Indonesia (Badan Pusat Statistik), Indonesia had 65.81 million people aged between 15-29 years in 2022. This represents 23.9% of the country’s population and 23.7% of the labor force.

Indonesia’s youth landscape offers a fascinating contrast that challenges our assumptions. Some may imagine a generation seamlessly navigating e-wallets, stock investments, crypto assets, and an array of digital financial services (DFS), but the truth is far more complex. Indonesia has an estimated 92% mobile phone ownership and 84% internet penetration among youth. As per the Financial Inclusion Insight Indonesia (2020), youth aged between 18-35 years reported higher use of digital financial services (45.5%) than others between 36-50 years (9.8%).

Yet, MSC’s study found that youth faced demand-side and supply-side constraints in their access to finances. These constraints included limited experience with formal financial services, lack of adequate collateral, and being perceived as a higher-risk borrower due to the absence of collateral security.

Indonesia’s digital gambling and crypto challenge

As per recent reports from Indonesia’s Financial Transaction Reports and Analysis Center (Pusat Pelaporan dan Analisis Transaksi Keuangan (PPATK)), online gamblers lost IDR 200 trillion (USD 12.5 billion) between 2017 and 2022. 78% of the 2.7 million online gamblers identified by the PPATK belong to the low-income group. They include youth who struggle to make ends meet on less than IDR 100,000 (USD 6.5) daily.

On the other side, Indonesia’s Commodity Futures Trading Regulatory Agency (Badan Pengawas Perdagangan Berjangka Komoditi or Bappebti) reported that 17 million Indonesians invested in cryptocurrency, a high-risk investment instrument of digital coins. Around 48% of crypto users are people aged between 18 to 35. While cryptocurrency has promised wealth, it has also brought some adverse outcomes and revealed that even young people who are good with technology can get caught up in systems that lead to adverse outcomes. OJK reported that the losses incurred by the public due to cryptocurrency-related scams and illegal robo-trading practices reached IDR 6.5 trillion (USD 400 million) in 2021.

Diversity beneath the surface

The Indonesian government introduced the “one student, one bank account policy” (KEJAR) specifically for young students to ensure access to a bank account. OJK also designed two products, Simpanan Pelajar (SIMPEL) and Tabungan mahasiswa dan pemuda (SiMuda), for providers to implement this policy. Financial literacy and readiness vary among youth. This, coupled with different levels of technological proficiency, hinders some youth when they attempt to open and operate a bank account.

One end of the spectrum has a group of youth who are not entirely tech-savvy. These individuals mostly rely on physical cash transactions, are unsure about digital platforms, and may even invest in traditional assets, such as livestock. They find comfort in the familiarity of physical currency and approach digital platforms cautiously. Conversely, Indonesia also has a group of digitally adept youth who embrace advanced financial practices. Our study testifies to this gap. Youth in Java prefer debit cards (48%) and electronic money (35%) transactions, the highest level across all islands. On the other hand, 93% of Sulawesi youth still prefer to transact in cash.

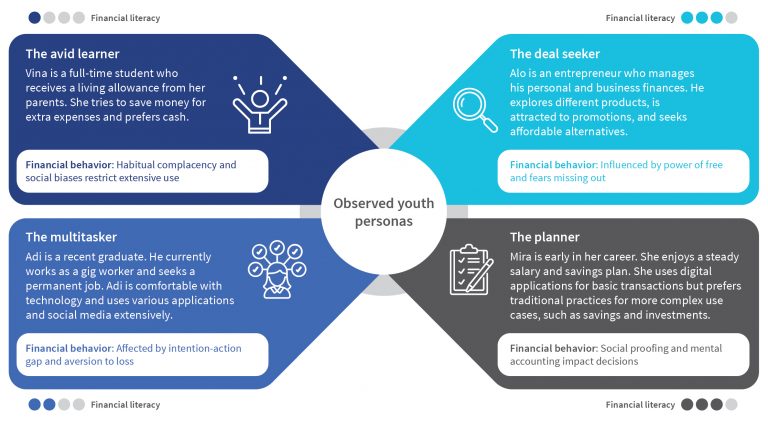

Exploring youth: Meet the four personas

We identified four different personas after in-depth discussions with more than 100 youth in six locations across island groups. Each persona had a unique approach to how they manage finances and embrace digital advancements. These personas embody the diverse characteristics and knowledge that define Indonesian youth.

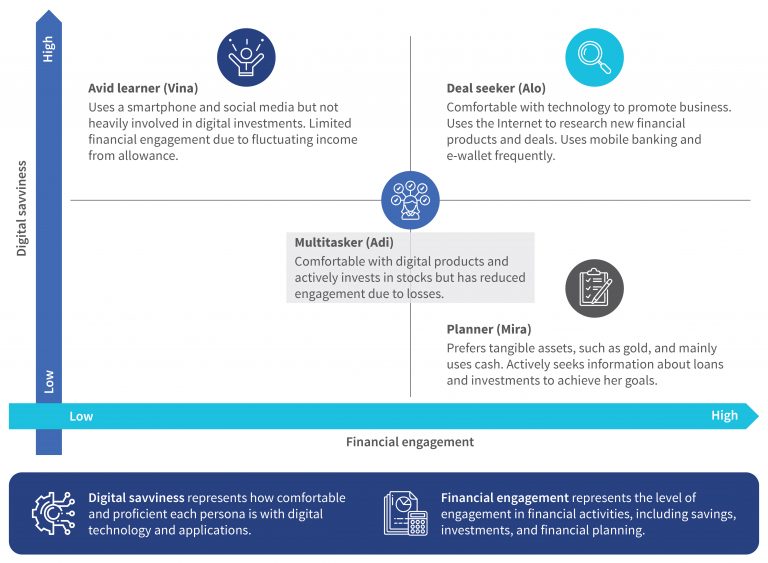

Let us examine where each persona falls within our digital savviness and financial engagement matrix. This matrix helps us understand how comfortable they are with technology and their involvement level in financial activities.

Translating personas into effective policies

Our exploration into the diverse youth personas reveals the complex financial landscape of Indonesian youth. These insights are valuable for policymakers to establish comprehensive policies and interventions based on the personas. The following recommendations can help policymakers serve all youth personas effectively:

- Develop comprehensive digital financial literacy programs tailored to Indonesian youth. Despite increased investment among youth, 78% lack fundamental financial and investment services knowledge, which highlights the necessity for comprehensive financial education. As part of this initiative, policymakers and stakeholders should establish robust monitoring and evaluation mechanisms to track financial literacy progress. MSC underscores the importance of the shift from limited-impact traditional methods to a product-centric learning approach that uses experiential and peer learning delivered in “teachable moments.” Furthermore, we can also use influencers to deliver small financial lessons to youth. Each persona could get tailored features to increase engagement:

- The planner: Develop simplified digital financial education materials that align with traditional practices. Offer personalized financial literacy sessions that focus on tangible asset investments, such as gold. Provide user-friendly digital platforms with easy access to key product information;

- The deal seeker: Create interactive and gamified digital financial literacy content to engage this persona. Offer budgeting and financial planning apps with customization features to cater to their fluctuating income patterns. Collaborate with influencers to promote financial education on social media platforms;

- The avid learner: Establish online courses and webinars that cater to educational goals. Provide youth-centric financial education content on platforms they commonly use. Emphasize the importance of goal-oriented savings and investments in their learning journey;

- The multitasker: Partner with popular tech platforms to deliver bite-sized financial literacy content. Offer educational content through apps they frequently use. Implement referral programs that encourage them to share financial knowledge with peers. Ensure that financial information is easily accessible via digital channels they prefer.

- Strengthen data protection regulations and ensure transparent communication in financial interactions. MSC emphasizes strong data protection to build trust and safeguard personal and financial data. This will benefit all personas who use digital financial services.

- Encourage the use of e-KYC to streamline onboarding processes for youth. Policymakers can tailor this policy for each persona. For example, Mira, the planner who values simplicity and traditional practices, should receive e-KYC through a trusted financial institution with physical branches. Meanwhile, Adi, the multitasker, can benefit from e-KYC integrated into the platform he already uses, such as ride-sharing or delivery apps, to complement his fast-paced lifestyle.

Similarly, financial service providers must use a systematic approach to develop products for youth. MSC had previously identified six aspects of youth-targeted product development. Based on this research that focuses on behaviors and personas, they can also develop tailored products for each persona:

- The planner: Recognize their inclination toward traditional practices and easy product access even for complex financial requirements. This suggests the need for streamlined, user-friendly interfaces in digital platforms. Offer concise “key fact statements” on products to appeal to this group and align with their preference for simplicity. Products, such as gold savings, also resonate better with this youth segment.

- The deal seeker: This group’s pursuit of affordability and value indicates a prime opportunity for financial institutions to provide flexible solutions that cater to fluctuating income patterns. Develop products with features that allow customization to resonate well with this segment, such as adjustable savings goals or repayment schedules.

- The avid learner: Address their preference for goal-oriented savings products. This can involve the development of platforms that allow youth to categorize their savings and visualize progress toward their objectives. Emphasize clear communication through “key fact statements” for engagement with this group.

- The multitasker: Given their comfort with technology, suggest the potential for partnerships with different apps and platforms. Collaborations between financial service providers and popular tech platforms can enhance accessibility and reach, which aligns with this persona’s habits. Referrals and timely introduction to products and services through the right behavioral nudges will also increase uptake and use.

The planner, deal seeker, avid learner, and multitasker personas are not just demographic segments. They provide critical information about Indonesian youth’s varied aspirations and challenges. The right behavioral nudges will help increase product usage and promote financial health among Indonesian youth.

MSC has a dedicated team and strategy to continuously engage with stakeholders who serve the youth sector. This blog bases its findings and recommendations on Youth Finsights 2.0, a survey of 2,182 Indonesian youth aged 15-29. MSC and the financial inclusion youth ambassadors of DOKA conducted this survey for the National Strategy for Financial Inclusion (SNKI), with support from the Asian Development Bank. Here is the final report.

Written by

Sneha Sampath

Manager

Leave comments