The role of finance in unlocking Kenya’s electric-motorcycle (e-boda) subsector’s growth

by Kamal Chhabra, Jeanne Nganga, Mandira Sharma, Priscilla Okutoyi and Kim Kariuki

by Kamal Chhabra, Jeanne Nganga, Mandira Sharma, Priscilla Okutoyi and Kim Kariuki May 24, 2024

May 24, 2024 5 min

5 min

This blog explores the role of finance to unlock Kenya’s electric motorcycle (e-boda) subsector’s growth. It gives an in-depth analysis of the barriers to e-mobility adoption in Kenya and highlights our recommendations to overcome these challenges.

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

As time went on, the war in Ukraine and other macroeconomic factors further challenged Martin’s situation. Today, the prevailing inflation, high interest rates, and rapid currency devaluation in Kenya make it difficult for Martin to operate. He struggles to make timely repayments against his loan and run his motorbike due to fluctuating fuel prices. He also cannot upgrade his aging boda due to higher financing and replacement costs.

In contrast, Joseph entered the transport business in late 2023 and bought an e-boda from a leading e-mobility provider. His transition was smooth. He could save USD 6 daily on fuel costs—more than 50% of his earnings. Moreover, the superior quality of the current fleets made his maintenance costs negligible. His transition immediately increased his daily profit and boosted his resilience after the period of economic turbulence.

Today, Joseph travels about 80 kilometers on a fully charged battery and pays USD 1.42 to swap out his battery at charging stations. These stations have been rapidly growing across the city. Joseph is an ardent supporter of e-bodas. He has persuaded others within his chama to transition despite challenges, such as high upfront costs, costly credit terms, limited charging stations, and persistent fears around the perceived unreliability of e-bodas.

Martin is among Africa’s 27 million boda operators—a sector poised to grow by 50% by 2050. This growth would result in increased traffic congestion and more traffic accidents, such as injuries and fatalities. The sub-sector with the exception of e-bodas would also contribute to higher emissions and poor air quality. In comparison to the globe, the growth of Africa’s global electric vehicle (EV) market share has been slow. EVs are expected to contribute less than 2% of the global market by 2029. Despite the small market share occupied by Africa, there has been recommendable growth within each country. For instance, around 40 e-boda startups have emerged in Kenya and raised USD 52 million—a first for the continent. Each e-boda provider offers unique products, distribution, and payment models to capture the internal combustion engine market. Yet e-mobility adoption remaings slow despite interventions focused on awareness, quality, finance, technology, infrastructure, and policies, as revealed in MSC’s interviews with industry players. Our teams spoke to representatives from organizations, such as ARC Ride, Auto Truck East Africa Limited, Knights Energy, and KIRI EV.

Finance as a driver of uptake

Improvement in access to finance on both the demand and supply sides is pivotal to drive e-bodas’ uptake. Until recently, financial service providers were unwilling to finance the purchase of e-bodas due to their unfamiliarity with the segment and the unproven nature of the solutions. However, this has been changing due to the emergence of quality solutions, tracking, and lock-out technology.

M-KOPA, Mogo, Watu, and Fortune Credit are public examples of organizations that lead the charge with innovative business-to-business (B2B) and business-to-consumer (B2C) payment and financing models. Yet the cost of financing remains elevated despite these efforts. In February 2024, the Central Bank of Kenya reported that commercial interest rates were as high as 15.88%—the highest in the past five years.

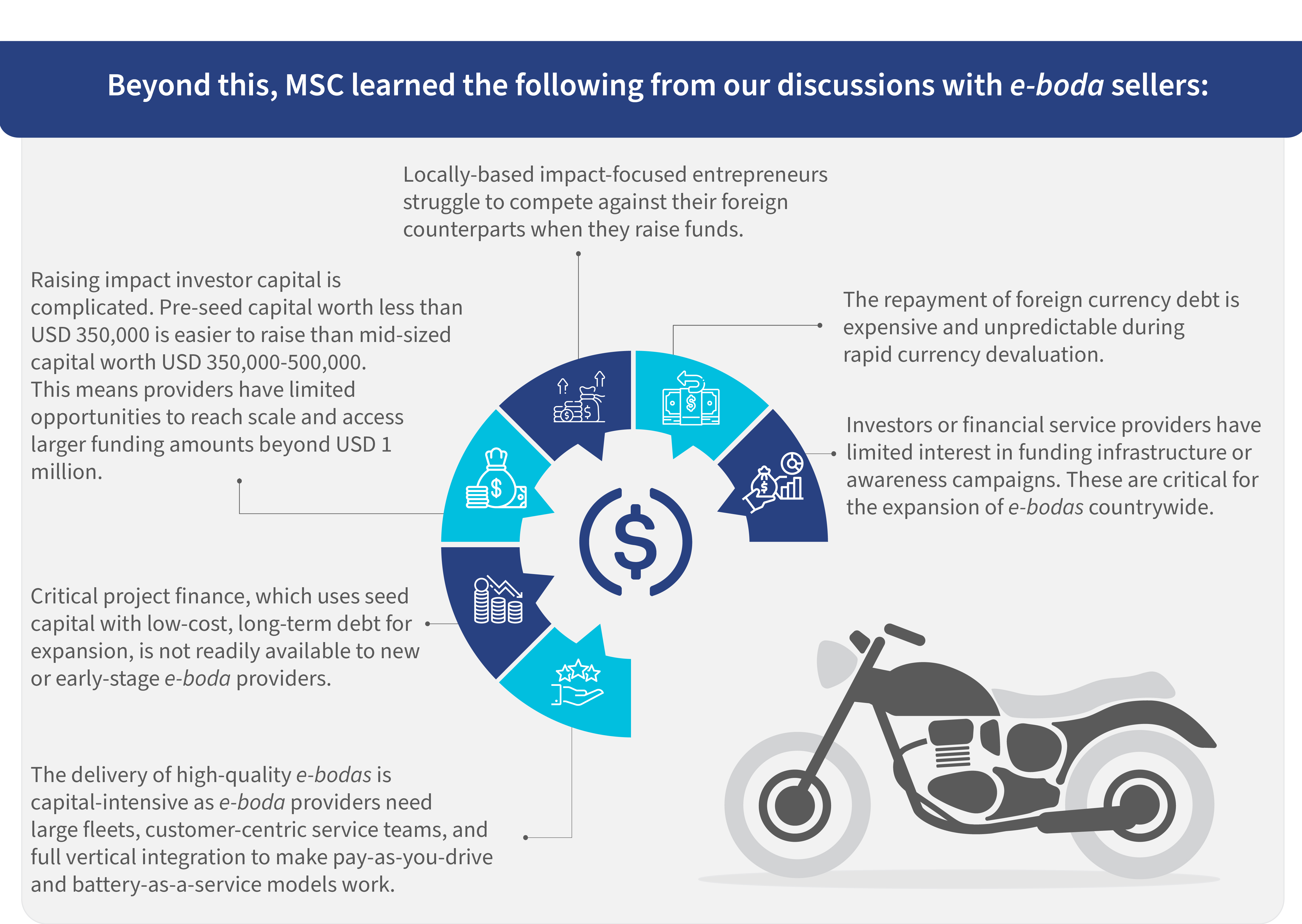

Beyond this, MSC learned the following from our discussions with e-boda sellers:

MSC’s recommendations to address financing challenges

Based on our assessment of the financing challenges, MSC recommends the following solutions to unlock financing constraints:

1. Use blended financing solutions. These solutions can crowd in funds from state and non-state resources at cheaper rates to reduce adopters’ borrowing costs. These solutions also increase working capital facilities for credit providers, minimize risks associated with foreign currency volatility, and inject liquidity into providers’ operations.

SDG-focused patient capital providers, such as international investors or donors, can be involved to provide this cheaper capital to local financing entities. MSC worked on the EVOLVE RSP Project, which provided partial credit guarantees and concessional loans to promote two- and three-wheelers in India. Africa can replicate this approach.

2. Use green financing instruments to build infrastructure and help popularize e-bodas countrywide. The Kenya Green Bond Programme and the county green finance assessment program by FSD Kenya exemplify how debt instruments can support real economic growth in a climate-responsive manner.

Moreover, funds from these instruments can meet the growth needs of mid-sized e-boda providers, promote quality assurance, and enhance market awareness. These can also drive industry innovation, support technology advancements, and offer results-based incentives to spur growth and promote inclusivity in a male-dominated sector that has barred women’s participation due to cultural and safety concerns.

3. Develop digital solutions that support credit appraisal, disbursement, and repayments. These solutions can also support product tracking, reverse logistics, and lock-out technologies in case of default. Digital products can drive accessibility, affordability, and convenience among nano-entrepreneurs while they incentivize climate-smart behavior adoption if combined with innovative climate financing solutions, such as carbon credits.

A telematics device in each vehicle can reduce finance risks when asset finance instruments are used. These devices track performance, calculate carbon credits, and estimate potential revenues generated.

Despite challenges, Kenya’s e-boda subsector is poised to take off rapidly. This subsector provides significant opportunities for economic growth and environmental benefits as it reduces greenhouse gas emissions. However, the subsector’s success hinges on the availability of innovative financial instruments.

Joseph’s experience showcases the progress made in the delivery of demand-side financing solutions and the economic benefits that accrue to nano-entrepreneurs. The critical role of innovative financing cannot be overstated. Solutions, such as blended finance, green finance, and digital solutions, are vital to lower entry costs, enhance e-boda businesses’ viability, and provide sustainable mobility. This is critical if Kenya intends to successfully introduce more than 1 million e-bodas by 2030.

External contributors include the following industry experts:

- ARC Ride: James Waweru (Sales Manager)

- Auto Truck East Africa Limited: Kenneth Guantai (Founder and CEO)

- Knights Energy: Francis Romano (CEO)

- KIRI EV: Christopher Maara (Founder)

Written by

Kamal Chhabra

Senior manager

Jeanne Nganga

Associate, Banking, Financial Services, and Insurance

Priscilla Okutoyi

Manager, Banking, Financial Services, and Insurance

Leave comments