Savings before credit: Turning BURO’s borrowers into net depositors

by Graham Wright and Mosharrof Hossain

by Graham Wright and Mosharrof Hossain Jun 2, 2026

Jun 2, 2026 6 min

6 min

In this blog, BURO Bangladesh challenges traditional microfinance institutions, which allow clients open access to their savings. This flexibility has built deep trust over 35 years that empowers clients to achieve financial autonomy and transforms them from net borrowers into net depositors.

Perhaps we were naïve. It never occurred to us that it could be acceptable for microfinance institutions (MFIs) to extract “compulsory savings” and lock them in until the client left the organization. Yet, that was the prevalent model in Bangladesh. Compulsory savings were allegedly necessary because poor people needed the discipline to save. The MFIs’ refusal to give them access until they left was ostensibly to allow them to build up lump sums.

This logic struck us as disingenuous, flawed, and exploitative. The real reason for the compulsory savings was to help raise capital for the MFIs to on-lend to the very people from whom these MFIs were levying the savings. Insisting that the client leave the organization before they had access to their own savings seemed like a recipe for churn.

We set up the BURO model in 1990 explicitly to challenge the norm. We allowed BURO clients to withdraw their savings on demand. We started in Tangail District. Our fieldwork in 2026 revealed that while most MFIs now allow their clients access to their savings, many branch managers still use savings to pay off unpaid loan installments, which undermines trust. In contrast, as a BURO client in Silimpur told us, “We trust BURO. It lets us withdraw our savings whenever we want and gives us the loans we need. We do not need any other organization.”

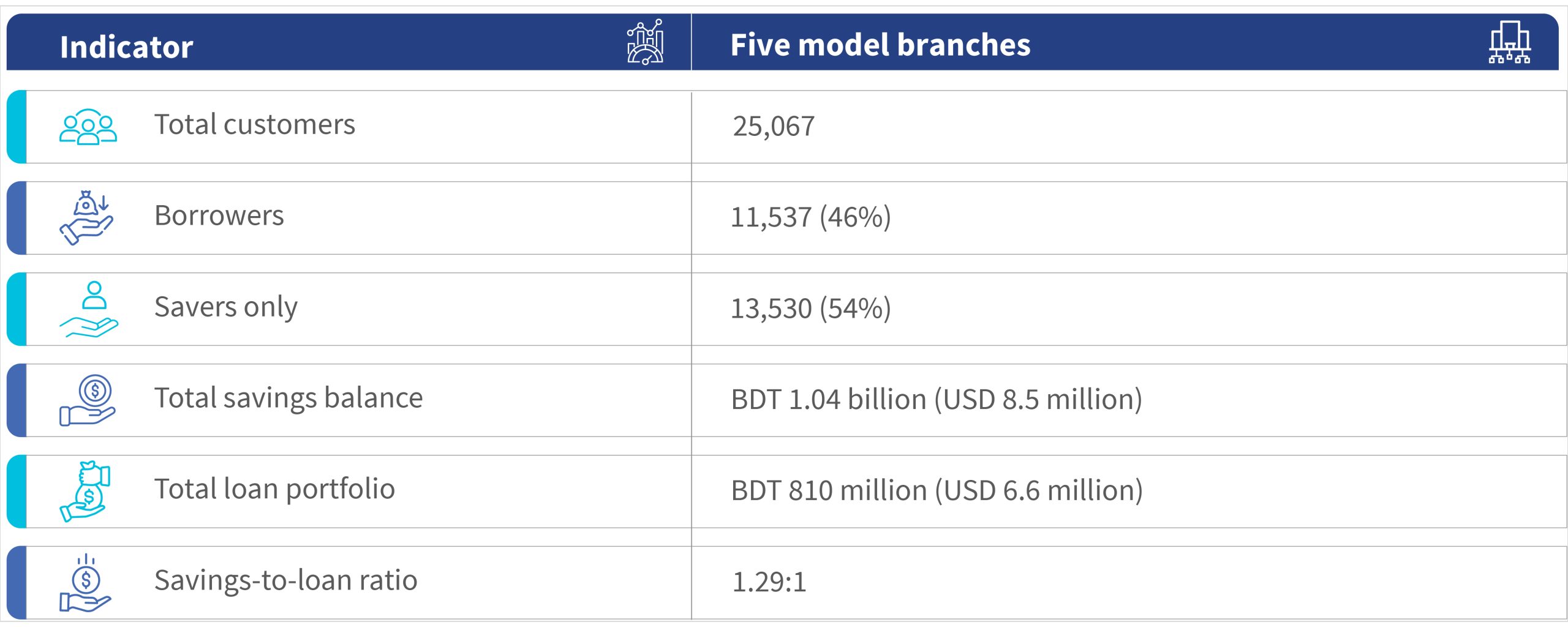

Key outcomes across the five model branches

At the end of 2025, BURO Bangladesh had 3.14 million active clients. Of these, only 2.53 million (80%) are borrowing. Today, a remarkable transition has occurred. All BURO’s original “five model branches” have net deposit balances that attract more deposits than they lend out. BURO’s clients in all five branches display “savings-surplus” behavior.

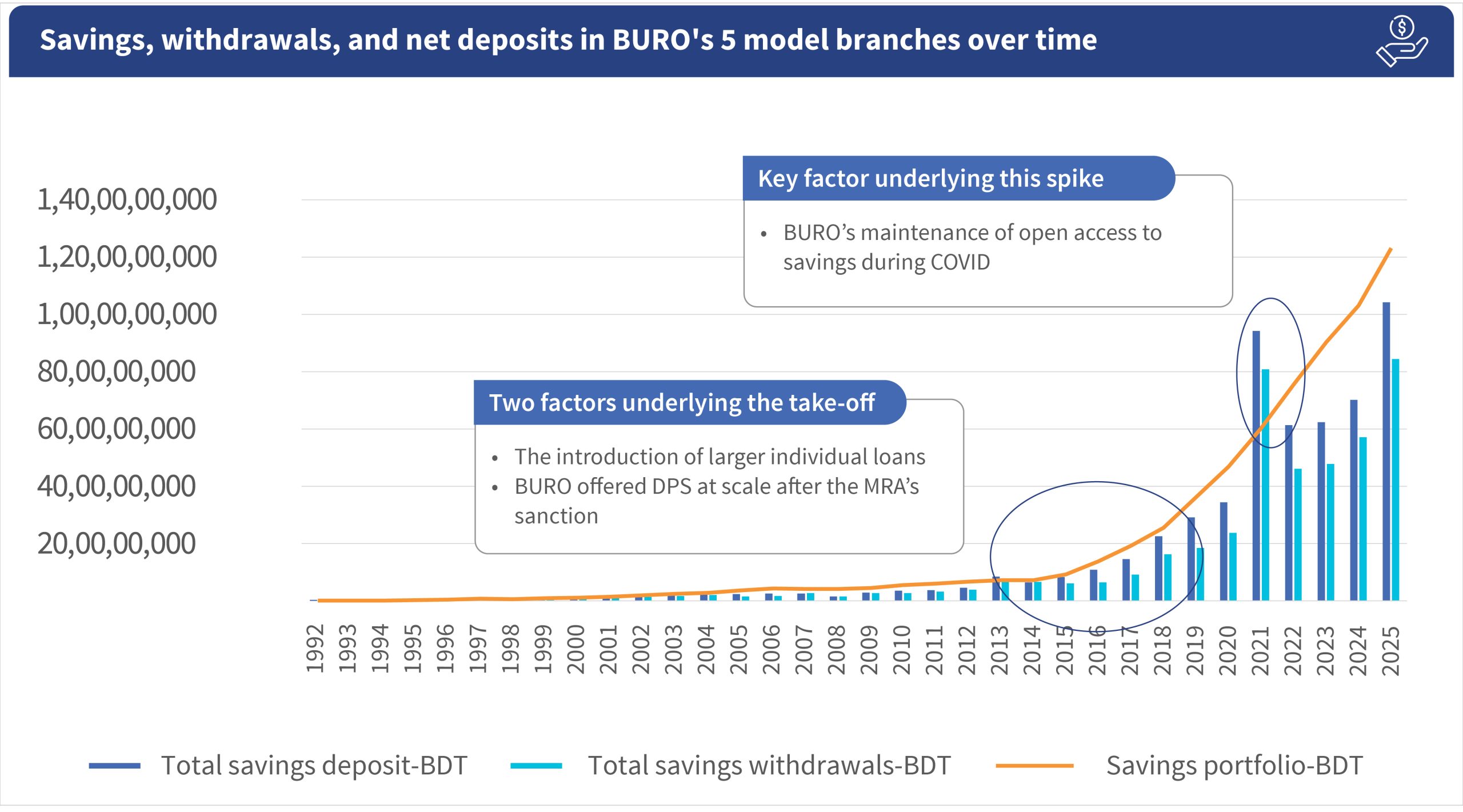

Analysis of savings, withdrawals, and net deposits in the five model branches shows a remarkable pattern. Over time, clients came to trust BURO, and people continued to deposit, even during floods. This trend accelerated and took off around 2013-14, when BURO began offering its services to small entrepreneurs and salaried workers. Both categories required larger loans but were also able to save larger amounts.

Throughout, BURO has offered its Deposit Pension Scheme (DPS). The DPS is a contractual savings product with interest rates of 10%, 8%, or 7% per annum, with a commitment of 10, 5, or 3 years. Unlike most other MFIs that offer this product, BURO allows its clients to cash out these funds early with limited penalties if they have an emergency and need funds urgently. These popular products were sanctioned for full-scale rollout by the Microcredit Authority (MRA) in 2014 and promoted by BURO thereafter. These remain the BURO clients’ preferred way of building useful lump sums of money.

COVID -19 drove the 2021 spike in both savings deposits and withdrawals. Initially, BURO saw an outflow of funds, but this was soon replaced by a surge of deposits as clients understood that BURO would maintain uninterrupted access to their savings. When many banks and MFIs closed for extended periods during the pandemic, some clients withdrew from those institutions and shifted their savings to BURO.

Catalytic changes over time

In 1990, Bangladesh was still poor and conservative, and Tangail was no different, Microcredit had significant scope to provide working capital to enhance businesses. BURO’s small loans helped destitute households stand on their own feet and build a future. People took loans to rehabilitate broken or idle handlooms and purchase stock for small kiosk shops, for chicken and goat rearing, and to buy fertilizer for fields leased from rich landowners. As one old member put it, “Before, everyone was poor and we needed loans. Now, we have our own chicken and rice fields. We have money in our hands, so we can save.” As one long-term BURO client observed, “Before, we used to save BDT 10 (USD 0.08) per week, and now, we can save BDT 500 (USD 4.10).” We met one BURO client whose first loan was BDT 10,000 (USD 81.50) and now runs a successful business selling plastic sandals – she now borrows BDT 200,000 (USD 1,636) each time.

When we first started working in Tangail, we found no households with members working overseas. However, in the last 15 years or so, this has become much more common. During our fieldwork, we visited many villages where a substantial number of households had sent male members out to the Middle East or Malaysia. These men remitted money regularly, often through BURO itself. This allowed their spouses or mothers to save relatively substantial amounts with BURO on a regular basis. One old woman noted, “Many people in the village have sent their husbands or sons abroad for work. They do not need to rely on loans anymore and can rely on their savings.”

However, according to Heintz et al. (2017), 65% of Bangladeshi women still run enterprises from their homesteads, with 47% that generate income and 18% that reduce expenditure. We often heard that once they had saved an adequately large lump sum, they used it to buy cows or electric autorickshaws. “Before, women did not work. Now we all work and contribute. We do not need to depend on our husbands anymore.”

This extraordinary evolution should remind us all how important it is to assess the impact of microfinance over a long period of time. It should also remind us that low-income people need a range of financial services beyond credit.

So what to make of this remarkable story?

We have four hypotheses – all open to debate, but all help explain the data and are substantiated by the discussions we held with BURO’s clients.

- BURO’s presence and long history in Tangail, especially the five model branches, established 35 years ago, have created deep trust. This is amplified by other MFIs that:

(a) Refuse to allow withdrawals from savings accounts while loans are outstanding;

(b) Net-off delayed loan installments against savings accounts without the member’s permission; and

(c) Do not permit early breaking of contractual savings accounts.

As a result, people have moved to BURO as their (typically sole) provider of choice – and have developed a collective savings behavior, preferring to save with BURO over investing in land or larger houses. The flexibility BURO offers is highly valued and encourages people to save. This allows them to respond to needs or opportunities instantly, something they could not do if their money were tied up in land or buildings. Our blog, “Trust is the product: Why Tangail’s savers choose certainty over returns”, explores this dynamic at length - The DPS is a highly valued mechanism, and not (as we had originally envisaged) as a specific goal-focused savings mechanism, but as a way of setting money aside to build up lump sums. Decisions on what exactly these lump sums will be used for are typically made when the DPS matures and pays out. We explore this dynamic in greater detail in our blog, “When saving feels like freedom: Security, daughters’ futures, and financial confidence over time.”

- Access to credit and savings services has significant long-term impacts. It first enables households to build enterprises or send (typically male) relatives abroad to earn and remit money home. Households now have much more disposable income, which they often choose to save. Women, who frequently manage their households in the absence of men, have taken on greater responsibility and developed their own businesses. “Beyond borrowing: How women in Tangail make sophisticated investments” discusses the implications of this shift.

- BURO loans and savings services have often financed or enabled the education of both male and female children, and intergenerational impacts are now visible. These children, now adults, are educated and thus (a) can secure overseas work or salary-paying jobs, and (b) are unwilling to work in the fields and thus seek opportunities abroad or set up their own enterprises. Our blog, “Migration as a household investment and why finance arrives too late,” discusses this trend.

In the end …

What began in 1990 as a principled rejection of compulsory, inaccessible savings has evolved into something far more profound. In Tangail’s five model branches, clients are now net savers, not net borrowers. This transformation was driven by trust, flexibility, entrepreneurship, migration, education, and time. The clients’ voices confirm what the data reveals. When people are treated as capable financial decision-makers rather than passive recipients of discipline, they do not withdraw money but start to save more. In the long arc of development finance, BURO’s experience suggests that access, autonomy, and trust may be the most catalytic financial products of all.

Written by

Leave comments