Digital platforms: Catalysts for growth and sustainability among Bangladesh’s microentrepreneurs: Part 1

by Md Farista Andalib, Samveet Sahoo and Ihsan Mahboob Hoq

by Md Farista Andalib, Samveet Sahoo and Ihsan Mahboob Hoq Oct 25, 2024

Oct 25, 2024 4 min

4 min

Bangladesh’s 9 million microenterprises drive the informal economy, contributing 56% of employment and 25% of GDP. Digital platforms like Truck Lagbe, WE, and ShopUp provide these businesses with market access, efficiency tools, and growth opportunities, improving profitability and resilience. Engaging with 400 microentrepreneurs across diverse sectors and regions reveals digital platforms’ impact on business performance and the support needed for broader inclusion and resilience.

Around 9 million microenterprises form the backbone of the informal economic sector in Bangladesh’s vibrant and rapidly growing economy. These small-scale businesses are vital to the country’s economic landscape and span diverse economic activities, such as agribusiness, food processing, retail trade, social selling, and transport and logistics. They constitute 56% of total employment and contribute 25% to the GDP.

The advent of digital platforms has ushered in new avenues for these entrepreneurs. Platforms, such as Truck Lagbe, Women and E-commerce (WE), Chaldal, Pandamart, and ShopUp, among others, provide tools and resources that can enhance their livelihoods. In this two-part blog series, we delve into digital platforms’ impact on Bangladesh’s largely informal microentrepreneur segment and highlight their role in improving profitability, access to financial services, and overall business growth and resilience.

Digital platforms provide easier access to new markets, customers, and essential business tools to empower Bangladeshi microentrepreneurs and enhance their profitability and resilience. Furthermore, digital tools can significantly improve microentrepreneurs’ efficiency, reduce operational costs, and facilitate access to broader markets, which helps increase income and overall business performance.

We engaged with 400 microentrepreneurs from retail trade, social selling, and transport and logistics sectors. These conversations uncovered the status of microenterprises that participate in digital platforms, the impact of exclusion from these platforms, and the support required to fill the gaps in the platforms to help microenterprises make their businesses more resilient. We met microentrepreneurs from urban centers, such as Dhaka, Khulna, and Chattogram, alongside rural areas, including Manikganj, Munshiganj, Pabna, and Sirajganj. We also connected with female microentrepreneurs to understand how digital platforms affect various types of microenterprises.

Financial benefits and increased profitability and sustainability

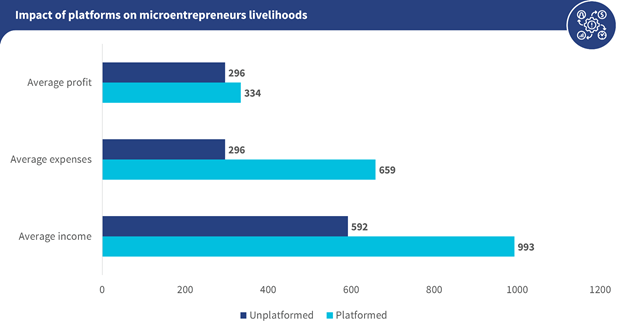

The study findings suggest microentrepreneurs who use digital platforms experience significant financial benefits compared to their non-platformed counterparts. On average, platformed microentrepreneurs see their incomes rise from USD 592 to USD 993, and their profits increase from USD 296 to USD 334. While platformed microentrepreneurs incur higher operating expenses, the substantial increase in revenue compensates for these expenses and leads to improved profitability and sustainability.

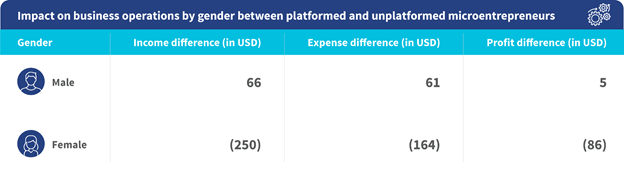

The study also showed notable gender and regional dissimilarities in earnings and expenditures. Male microentrepreneurs who use digital platforms tend to report higher expenses and earn higher profits than the unplatformed. Interestingly, the same trend was not seen for female microentrepreneurs, which indicates that being platformed does not correlate strongly with improved financial outcomes for women. Urban platformed microentrepreneurs exhibit higher expenditures and profits than their rural counterparts, which indicates that urban areas have higher business value.

Overall, digital platforms benefit users by improving business performance. More attention is needed to address barriers that hinder female micro entrepreneurs’ profitability. If digital platforms can help women overcome these obstacles, they can make these entrepreneurs’ business models more sustainable and inclusive, ultimately contributing to greater economic empowerment for all.

Access to formal financial services

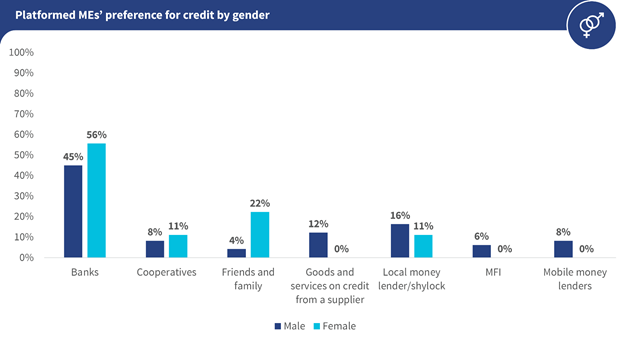

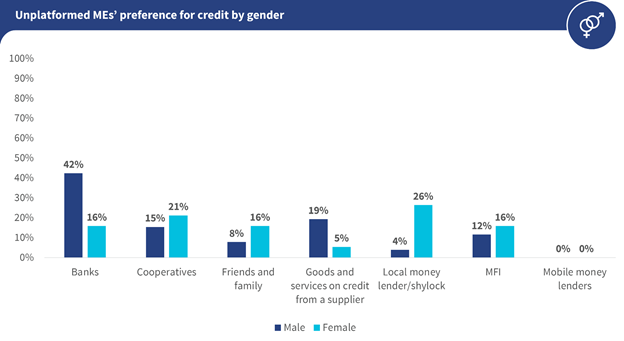

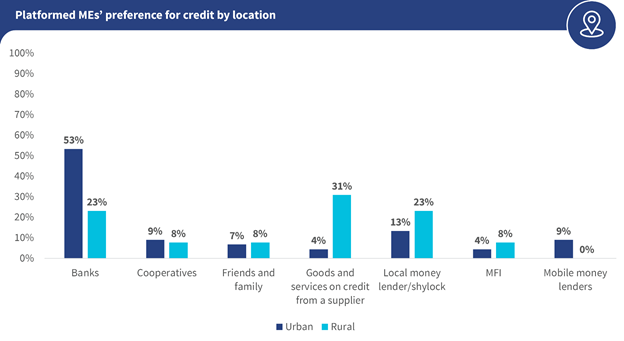

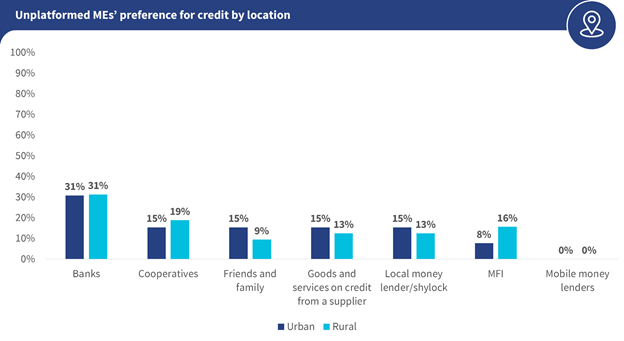

Credit preferences among microentrepreneurs in Bangladesh vary based on their gender and platform usage. Women (56%) on digital platforms often prefer formal financial institutions like banks. In contrast, men (45%) explore a broader range of credit sources, which include informal sources, such as suppliers and mobile moneylenders. On the other hand, unplatformed women enterprises (68%) rely heavily on informal credit sources. In urban areas, platformed entrepreneurs (57%) prioritize formal banking, while their rural counterparts (69%) lean toward informal sources. Interestingly, unplatformed urban (61%) and rural entrepreneurs (47%) rely similarly on informal credit. Bridging these gaps can empower microentrepreneurs and foster inclusive economic growth.

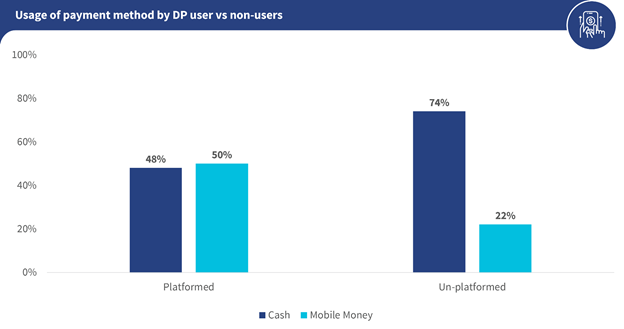

Microentrepreneurs are more inclined to use cash

Microentrepreneurs exhibit diverse payment preferences influenced by their digital platform usage. Those who have reduced their use of digital platforms tend to rely on cash for business transactions. In contrast, microentrepreneurs who have increased their use of digital platforms or remained consistent in their platform usage generally prefer mobile money services, such as bKash or Rocket, for their payments.

This trend varies by location and gender. Rural microentrepreneurs tend to use cash, while their urban counterparts often favor mobile money. Gender also plays a role, as female microentrepreneurs typically prefer mobile money, whereas male microentrepreneurs lean toward cash. An important reason for the preference for mobile money among female microentrepreneurs is their involvement in social selling, where customers often make payments through mobile money.

Cash remains the dominant choice for transactions for microentrepreneurs who do not use digital platforms, regardless of gender or location. However, urban microentrepreneurs have a slightly higher preference for cash over their rural peers. Given these insights, stakeholders have a significant opportunity to enhance the adoption of digital payments among microentrepreneurs and aid their inclusion in a more formal economy.

In the next part of this two-part blog series, we will look at the factors that influence platform adoption for different sectors of microentrepreneurs, women-owned microentrepreneurs’ unique motivation to onboard digital platforms, the social and economic impact of digital platforms on microentrepreneurs, and ways to increase digital platform adoption for them. Read the next part here.

Leave comments