Why cash payments are transforming humanitarian aid delivery

by Brenda Oyugi, Edward Obiko and Endashaw Tesfaye

by Brenda Oyugi, Edward Obiko and Endashaw Tesfaye Apr 1, 2025

Apr 1, 2025 4 min

4 min

In this blog we explore how Cash Voucher Assistance (CVA) is reshaping humanitarian aid and what the future holds for vulnerable communities in the Somali region in Ethiopia.

A two-part blog looking at Cash Voucher Assistance in relief operations in the Somali Region of Ethiopia

Cash transfer programming is increasingly a preferred method of delivering humanitarian aid. Armed with an injection of cash, targets for a humanitarian response can decide how to meet their own needs and respond rapidly when those needs change. What’s more, additional cash in a recovering economy can serve to buoy local businesses, helping to keep local markets healthy when crises become protracted.

Cash transfers empower recipients by allowing them to prioritize their needs: food, shelter, healthcare, or education. This flexibility is critical in diverse and dynamic situations, such as crises where needs can rapidly change.

In addition, Cash Voucher Assistance supports local economies by injecting cash directly into communities, stimulating market activity, and enabling local businesses to thrive. This is particularly important in prolonged crises where traditional aid can undermine local markets. Moreover, cash transfers are often more cost-effective and, logistically simpler and more straightforward to distribute than in-kind aid, reducing overhead costs and ensuring a greater portion of funds directly benefits those in need.

Over the past decade, cash transfer programming globally has seen significant growth within the humanitarian aid sector. By 2016, the UN Secretary-General emphasized that cash transfers should become the primary support method for crisis-affected populations whenever feasible. This recommendation was rooted in the evolving understanding that cash-based interventions often provide more flexible, efficient, and dignified assistance than traditional in-kind aid.

The roots of Cash Voucher Assistance (CVA) trace back to the early 2000s when pilot projects demonstrated their effectiveness in various contexts, including responses to natural disasters and conflicts. By the mid-2010s, numerous large-scale humanitarian organizations had integrated CVA into their standard practices. For instance, in 2015, the UN’s World Food Programme (WFP) reported that CVAs constituted 21% of its food assistance portfolio. Data from the Cash Learning Partnership (CaLP) reveals that by 2018, over USD 5.6 billion was distributed through CVA globally, marking a substantial increase from previous years.

As CVA usage grows, the modes of delivery also evolve. Initially, cash assistance often involved physically disbursing cash to recipients, which posed challenges such as security risks and logistical complexities. However, the proliferation of digital technologies and mobile banking or mobile money has significantly transformed the disbursement landscape. According to CaLP, digital payments are now becoming a preferred method of delivery for the distribution of CVA.

Donors such as the European Union’s humanitarian unit, DG ECHO, are promoting a “Digital by Default” form of humanitarian support distribution while implementing partners such as WFP are piloting digital payment in countries such as Ethiopia and Somalia. For instance, a 2020 pilot in Somalia demonstrated the effectiveness of this shift, with 63% of all such supports transitioning to digital payments by 2022. While the move towards digital payments has enabled greater speed and scale of response; a study conducted in the Horn of Africa has shown that humanitarian agencies are concerned about the time it takes to establish contracts with financial service providers.

Furthermore, a study conducted in Kenya by the Center for Global Development (CGD) and MicroSave Consulting (MSC) Global shows strong support for offering choices in financial service distribution channels where this is feasible. This choice is also advisable to address the demand of last-mile beneficiaries. Today, financial service providers (FSPs) and mobile money platforms are increasingly being used to transfer funds directly to beneficiaries’ accounts using digital payment solutions.

Why digitize payments in humanitarian aid in Ethiopia?

The Ethiopian government has been distributing CVA under the Productive Safety Net Programme (PSNP) since 2005. Notably, it was the first program to use mobile money in mid-2015, after a successful pilot in the Tigray region by the regional bureau office supported by UNICEF (It used the M-BIRR service of Dedebit MFI). Various organizations, including the World Bank, WFP, UNHCR, Islamic Relief, and World Vision, are involved in these humanitarian interventions.

Despite a substantial increase in account ownership in Ethiopia—from 22% in 2014 to over 46% in 2022 —a significant gap remains, particularly in rural areas, where over 75% of the population still struggles with limited access. The gender disparity is also striking, with only 39% of women owning accounts compared to 55% of men. These challenges highlight the urgent need for strategic interventions to further expand account ownership and improve the services provided to beneficiaries.

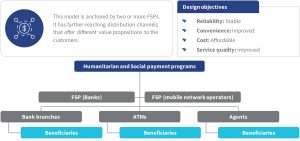

A critical component of advancing digital ways of distributing CVA in Ethiopia includes Financial Service Providers (FSPs) building a trained and appropriately incentivized agent network. This network, combined with a clear business model and the implementation of a master or super-agent model, can effectively reach small agents at a village level to support financial institutions. In a CaLP study, six bulk payment operators in humanitarian intervention2 reflected that such an agent network management structure is key to planning and managing liquidity for bulk disbursement services. This network should also target female agents in regions such as the Somali region, as their involvement can significantly enhance financial inclusion and gender equality.

Based on these findings and the knowledge of Ethiopian financial service providers, the United Nations Capital Development Fund (UNCDF) is leading an initiative to enhance the capabilities of FSPs engaged in humanitarian efforts, focusing on digital payments and agent network services. A comprehensive on-the-ground assessment revealed a gap between the needs of humanitarian aid services and the current capabilities of FSPs. In response, UNCDF, in partnership with MSC, launched a pilot program involving three FSPs—Commercial Bank of Ethiopia, Shebelle Bank, and Cooperative Bank of Oromia—to improve the delivery of CVA in a WFP intervention supporting 65,000 beneficiaries in the Somali region. The project was implemented in partnership with MSC under the Digital Finance for Resilience (DFS4Res) Programme, funded by the European Union and the Organization of African, Caribbean, and Pacific States (OACPS).

Follow us to go into the details of the lessons learned from this project.

Leave comments