Government subsidy in microinsurance: A necessary trend?

by Sunil Bhat and Premasis Mukherjee

by Sunil Bhat and Premasis Mukherjee Jun 12, 2014

Jun 12, 2014 4 min

4 min

Here the author gives a primer into government subsidy insurance programmes of various kinds, targeted at the lower income people. And questions if it is instrumental for microinsurance growth?

For quite some time, the world of microinsurance has been debating the role of government (more specifically government subsidy) in the growth of microinsurance. While commercial microinsurance – where the client pays a premium for their policies underwritten by an insurer – paved the way for innovative and efficient ways of delivering insurance services to the low-income people, these programmes have rarely achieved impressive outreach.

Meanwhile, governments have entered the sector with subsidized insurance programmes of various kinds, targeted at the lower income people. Though these government-subsidized insurance schemes often look similar to social security schemes, they are different fundamentally. While in traditional social security schemes, the government underwrites the risks and pays for the services, in this new generation of programmes the government pays the full (or a part of) premium, while the risk is underwritten by insurance companies.

Many argue that these schemes are not “microinsurance” in true spirit since often either client voluntarily subscribe to them, or do they pay the premium (or full premium) … and in some cases both! However, these schemes occupy a significant position in any discourse about the sector, since both of them are similar in function – they cover insurable risks of low-income people. Interestingly, these schemes do not fall under the purview of ILO’s definition but qualify as microinsurance in the definition coined by IAIS.

ILO Definition of Microinsurance:

Microinsurance is the protection of low-income people against specific perils in exchange for regular premium payments proportionate to the likelihood and cost of risk involved.

IAIS (International Association of Insurance Supervisors) Definition of Microinsurance:

Microinsurance is insurance that is accessed by low-income populations, provided by a variety of different entities but run in accordance with generally accepted insurance practices.

During the “Landscape of Microinsurance in Asia and Oceania” study, MicroSave came across many such schemes and were challenged to distinguish them from commercial microinsurance. We realized they are fast closing the gap with commercial microinsurance and hence it was unwise to let them fall outside the purview of the study. We landscaped these government subsidized microinsurance schemes as “social microinsurance” in the study, an idea we found limited buyers that time.

We are pleased to see that this idea has recently been endorsed by Michael McCord, a global veteran and leader in the field of microinsurance . While he argued in favor of government support in health insurance, we believe the logic can be extended in case of agricultural insurance, too. This learning is based on our recent project on weather index insurance in five Asian countries.

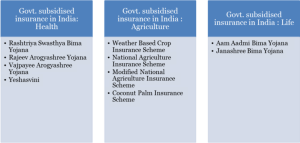

In the traditional agriculture insurance programme, viz. National Agriculture Insurance Scheme (NAIS) of India, the Government supported insurance companies in both ways: a) claims subsidy and b) premium subsidy. This resulted in a startlingly poor financial performance with a 640% claims ratio (for every INR100 of premium collected, NAIS paid INR640 as claims!!). The reasons for such high claims ratios might be poor design and/or non-actuarial pricing. However, without the government support, the insurance companies would never have come forward to offer this product (except maybe the public insurer AIC).

Based on the recommendations of a study by the World Bank and GFDRR in April 2011, the Indian Government modified the NAIS and called it mNAIS (modified NAIS). Under the mNAIS programme, the government provides an only premium subsidy, and the insurer has to bear the responsibility for claims. Since the underwriting risk is now carried by the insurer, they take extra care in the pricing and management of the scheme. The government’s role also helps the scheme non-financially, as it has now mandated all recipients of subsidized crop loan to avail the mNAIS facility, which has, in turn, helped the scheme achieve impressive outreach. The percentage of loanee to non-loanee farmers in India is 98%, which shows the role the government mandate played in creating the outreach.

Government subsidy is also extended to index-based agricultural insurance programmes of India (in addition to the traditional insurance schemes). Index insurance settles claims on the basis of measuring some proxy indicator (such as temperature, rainfall, wind speed, humidity etc.) in contrast to measuring the actual yield itself. India is the global leader in weather index insurance running the largest weather-based crop insurance scheme (WBCIS). Again, one of the main factors for success has been government support. Under this scheme, the farmer pays just one third the premium, and the remaining two-thirds are shared by the state and central governments. This way the premium ‘burden’ on the farmer is less, making them more willing to purchase the insurance product. There is an abundance of such full or part subsidized schemes in India. China, Georgia, Indonesia, Jordan, Kazakhstan, Nepal, Pakistan, Philippines, Thailand, and Vietnam are some other Asian countries with strong government subsidized microinsurance (or “social microinsurance programmes”).

In Asia, social microinsurance has an outreach of nearly 1.7 billion as compared to a little over 170 million insured through commercial microinsurance. This differential in outreach is a clear indication that government subsidy is instrumental and, quite probably, necessary in the growth of microinsurance, at least until the programme stabilizes (becomes sustainable and arrives at claim ratios of less than 100%). The government essentially plays the role of a market maker until the social microinsurance products are perfected, their delivery innovated and the outreach scaled up. However, the important question here would be when should the Government stop subsidizing these programmes … and, indeed, will it ever be able to do this considering the political compulsions! Perhaps part of the answer lies in a gradual phasing out of the subsidies as poorer populations experience benefits accruing to them and insurers make their products and delivery channels more robust.

Written by

Leave comments