Customer Protection in Indian Digital Financial Services: Part 2: Transparency and Privacy

by Soumya Harsh Pandey and Graham Wright

by Soumya Harsh Pandey and Graham Wright Mar 16, 2016

Mar 16, 2016 4 min

4 min

The part of the two blog series examines the transparency and privacy in Indian digital financial services

MicroSave’s study for the Omidyar Network on customer protection, risk and financial capability in India sought to understand the extent to which customer protection practices were embedded into DFS offerings in India. The research examined the effectiveness of these customer protection practices and the ease with which customers and agents could access them. In the first blog of this series, we examined Customer Recourse. This blog looks at Transparency and Privacy

2. Transparency

Communication with customers is typically verbal in nature

Our research showed that in most deployments, a well-developed customer support system in the form of regular interactions (SMS/voice) and monitoring visits by supervisors/managers to agents for optimising customer service is missing.

Furthermore, most customer communication is verbal. A small proportion of customers are not even provided information, either at the beginning or during the course of operation of their account. Some of the reasons for this were: agent did not have time; agent did not take interest; customers did not ask; and the agent explained initially, but they could not understand.

High dependence on agents both for terms and conditions of service, as well as for recourse options, makes customers highly vulnerable to agent-perpetrated fraud. Since most of the communication is verbal, the customers would not even know whether they are being defrauded or not.

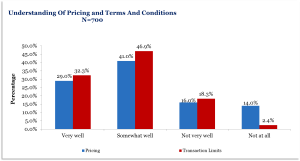

Around 2/3rd of the customers do not fully understand the terms and conditions of DFS service that they are using. Lack of awareness of service among customers is the largest stated barrier for DFS growth, according to MicroSave’s recent ANA India Survey.

Around 2/3rd of the customers do not fully understand the terms and conditions of DFS service that they are using. Lack of awareness of service among customers is the largest stated barrier for DFS growth, according to MicroSave’s recent ANA India Survey.

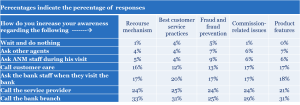

Communication Between Agents, Agent Network Managers, and Banks Needs to Improve

Communication Between Agents, Agent Network Managers, and Banks Needs to Improve

After the initial agency agreements, there is no active communication between the agent network managers (ANMs), banks and agents. The table below suggests that some agents try to reach out to the most responsive option, but a few just do not make any effort to reach out. This suggests that an active dialogue between agents and service providers is missing, and details are communicated only on the basis of a specific request from the agent.

Agents point out that lack of support for them in running the agency is one of the reasons why they do not recommend DFS/bank agency as a business to others.

Agents point out that lack of support for them in running the agency is one of the reasons why they do not recommend DFS/bank agency as a business to others.

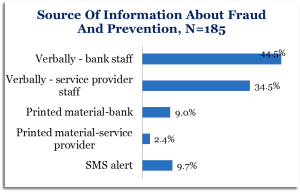

The current system of providing fraud and risk-related information to the agents is ad hoc, and only 63% of agents are provided information on frauds. In most cases, the information about risks is verbal and, thus, informal.

Proper formal communication about the terms and conditions of service is also not complete. Only 68% of all active agents reported having received documents with terms and conditions of service. Poor communication both at the customer as well as at the agent level means that the situation will facilitate external frauds as DFS grows and matures in India.

Proper formal communication about the terms and conditions of service is also not complete. Only 68% of all active agents reported having received documents with terms and conditions of service. Poor communication both at the customer as well as at the agent level means that the situation will facilitate external frauds as DFS grows and matures in India.

Moreover, coupled with low awareness levels about recourse among customers and high dependency on the agent for information and recourse, most customers, ANMs, and banks will not even know about risks/frauds until they have become big.

3. Privacy: Customers

Experienced customers (who have had an account for more than one year) are more aware of the means to protect their account information. More than one-third of all customers interviewed highlighted that they do not share their PIN. But, once again, agents are the most important source of information about methods to protect accounts.

Experienced customers (who have had an account for more than one year) are more aware of the means to protect their account information. More than one-third of all customers interviewed highlighted that they do not share their PIN. But, once again, agents are the most important source of information about methods to protect accounts.

As highlighted earlier, one of the major risks is transaction data security. However, MicroSave’s qualitative study shows that most transactions are assisted by the agent who thus has access to account details.

CGAP notes that assisted transactions are common particularly with elderly customers and in rural areas where literacy levels are low.

3. Privacy: Agents

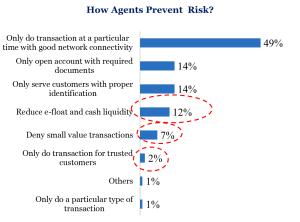

Agents are very proactive in protecting their personal and account information and do not share personal account-related information with others.

Though these are good practices, there are a number of ways in which fraud can happen, about which they are not aware and thus do not know about its prevention. (See Survival of the Fittest: The Evolution of Frauds in Uganda’s Mobile Money Market (Parts 1 and 2)).

In the same way that operational issues often lead to service denial (“Real and Perceived Risk in Indian Digital Financial Services”), the precautionary measures adopted by agents also often result in service denial to customers in different forms. As highlighted before in a variety of MicroSave and CGAP publications, this service denial undermines trust in digital financial services.

There is a clear need for significant improvements in the communication of both DFS products and how to use them in India. Not all agents will be able to do this, as it involves fundamentally different skills than conducting transactions, but many will be able to do so, given their existing (remarkably – almost alarmingly ― trusting) relationships with customers. Agents who really can only perform basic transactions to service existing products, should be supplemented with sales agents charged with clearly explaining products and how to use them.

Written by

Soumya Harsh Pandey

Senior Manager

Leave comments