Fintechs for LMI segments – Demystifying myths and delving into realities

by Mohit Saini and Meenal Malik

by Mohit Saini and Meenal Malik Aug 18, 2018

Aug 18, 2018 3 min

3 min

The second blog in the series highlights the potential opportunities present in the LMI market and how the current fintech ecosystem is approaching an inflexion point.

In our previous blog in this series, we presented recent trends in the fintech space in India. In that blog, we also defined the low- and middle-income (LMI) segments and examined the challenges that fintechs and investors face in catering to these segments.

This blog is the second in this series. It provides details on:

a. The opportunities present in the LMI market

b. The willingness of the LMI segments to take up fintech solutions; and

c. The transition of the current fintech ecosystem towards an inflexion point.

|

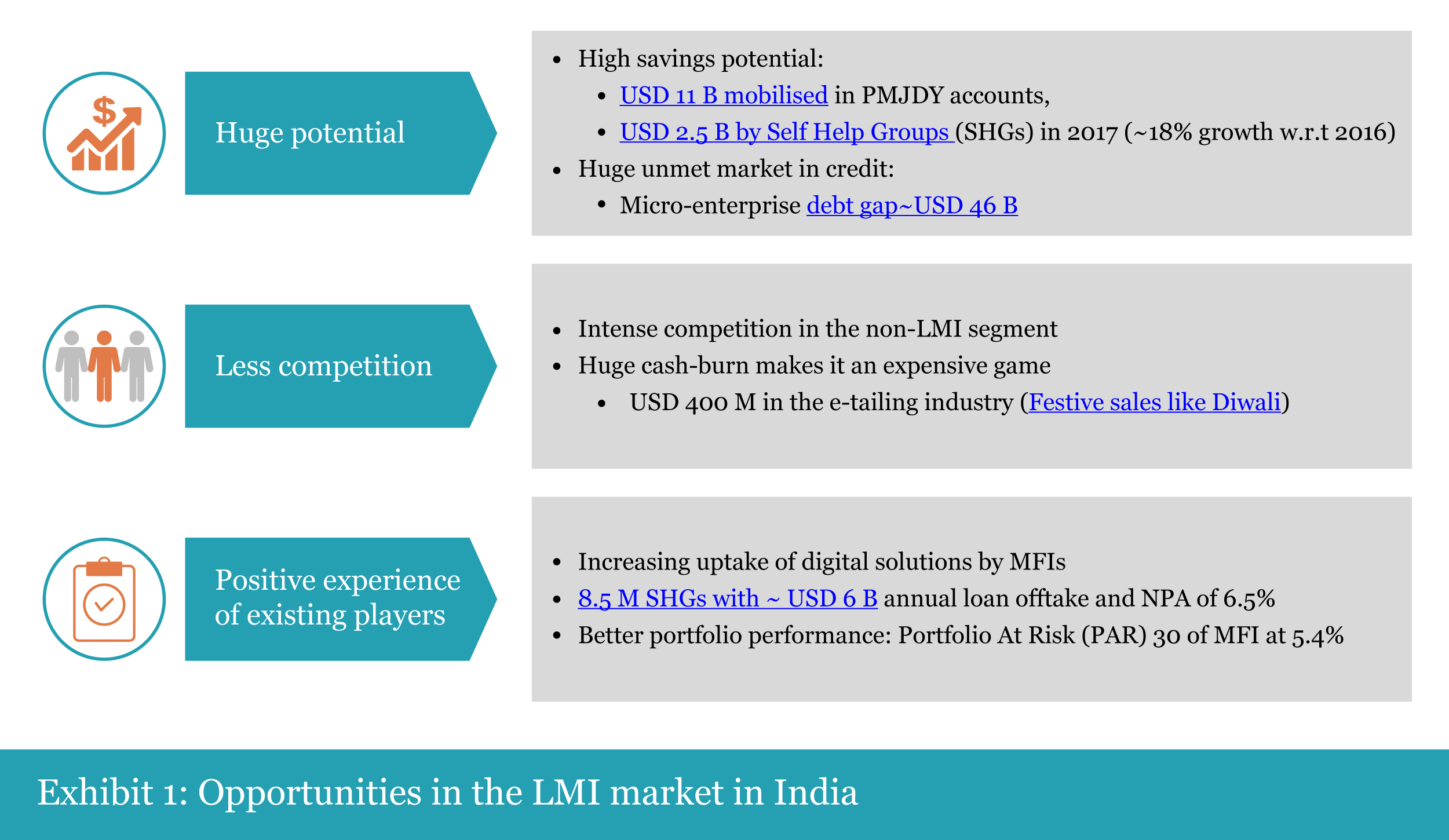

Opportunities present in the LMI market

Various stakeholders we interacted with in this research suggested that irrespective of the challenges pertaining to the LMI market, it offers huge potential. These stakeholders include investors, fintechs, and incumbents. Most of them, however, have been taking a cautious approach and waiting to see a proven business model before venturing into this space. A 2017 Deloitte report suggests that in the medium term, fintech players will consolidate their position in urban areas and metro cities, and will extend to the rural and semi-urban space over next 3-5 years.

Based on our analysis, here are the top three reasons that indicate that there exist significant opportunities in the LMI market:

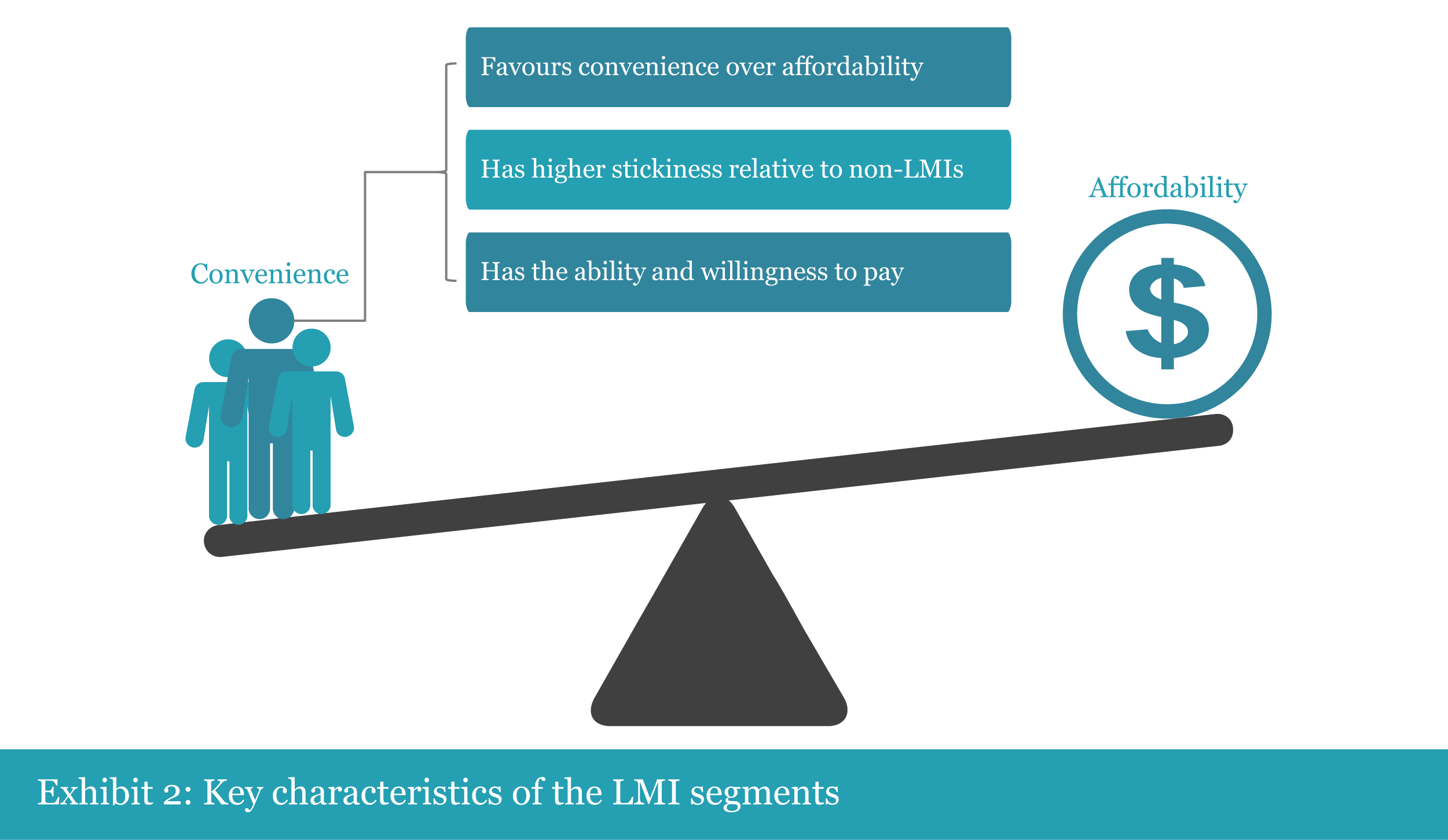

Affordability and willingness to adopt fintech solutions

It is interesting to note a few differences between a non-LMI and an LMI customer. For most non-LMI urban users, the convenience of using fintech solutions is obvious. They mostly decide on the basis of affordability and the economic incentives offered to use such solutions. This is the reason we see a continuous stream of cash-backs offered by fintechs, which lead to a high rate of cash-burn to serve the non-LMI urban market. LMI customers, however, favour convenience over affordability to minimise their opportunity-cost in accessing similar financial services.

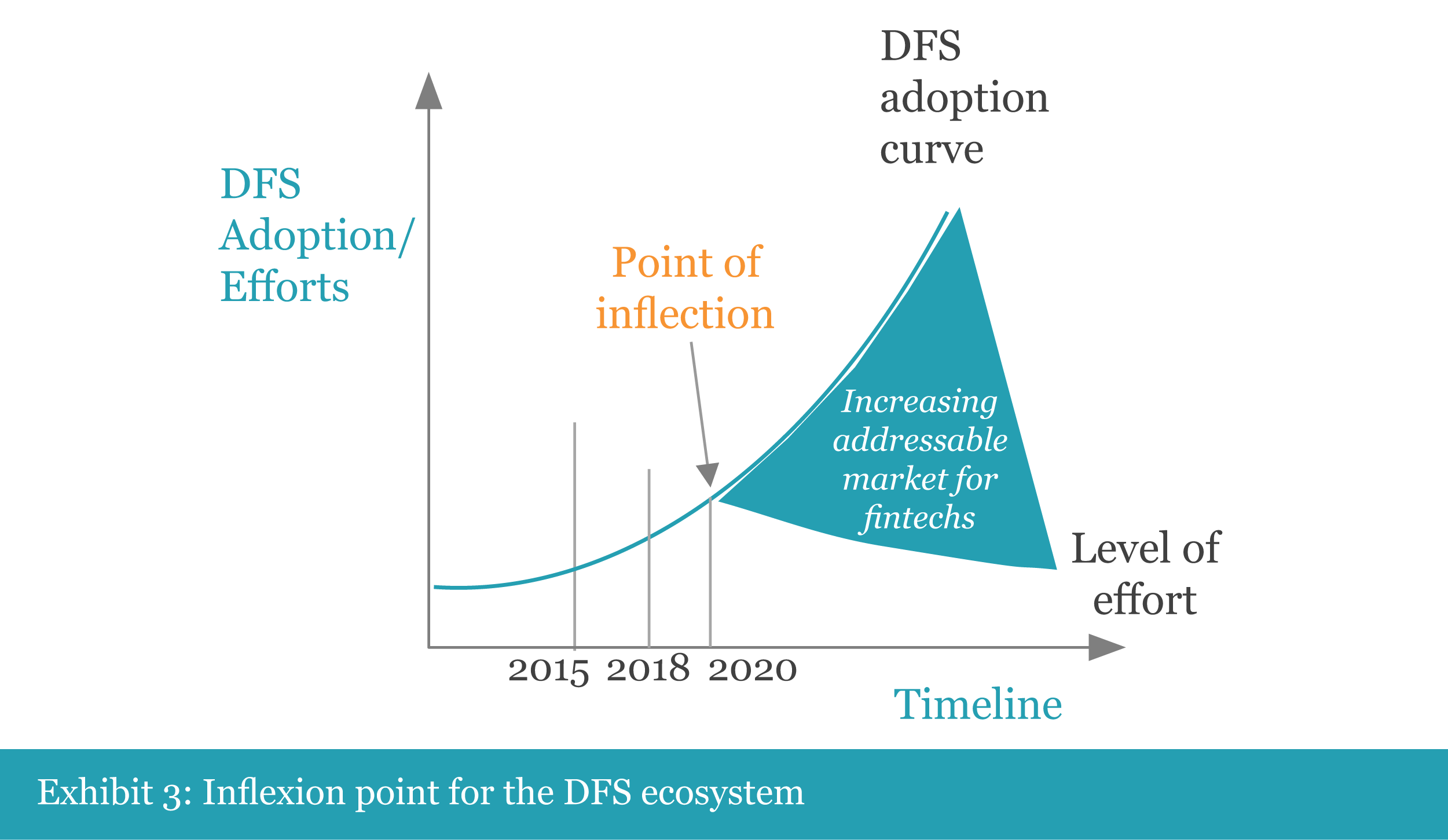

The ecosystem is transitioning towards an inflexion point

Our analysis indicates that the LMI market in the country will be ripe for fintech solutions by 2020. The adjoining graph suggests that the digital financial services (DFS) market is heading towards an inflexion point.

At this point, the level of efforts required to promote DFS would be less than the cost of providing the services. This is spurred by various technological innovations, such as IndiaStack and other open APIs, reduction in data cost, and fast adoption of smartphones.

An enabling ecosystem largely drives such a transition.

The graph below shows four developments that have played a critical role in building such an ecosystem:

These insights suggest that the LMI segments indeed present opportunities for fintechs and financial service providers like microfinance institutions (MFIs) and public sector banks (PSBs). As the ecosystem becomes more conducive for fintechs in the coming years, the time is ideal for them to shift their attention towards the LMI market. In our next blog in this series, we present some potential ways in which players in the ecosystem can serve the LMI market and unleash the untapped potential of this segment.

Written by

Mohit Saini

Senior Analyst

Leave comments