Winter is coming: Managing the digital onslaught

by Zeituna Mustafa and Christine Gachui

by Zeituna Mustafa and Christine Gachui Sep 11, 2018

Sep 11, 2018 3 min

3 min

This blog discusses how the incumbents can bring about a digital transformation to utilise the disruptive power of technology and innovation.

In the previous blog of this series, we discussed the changing nature of the financial services industry. We talked about how digital disruption has had an impact on traditional financial institutions. In this blog, we discuss how the incumbents can bring about a digital transformation to utilize the disruptive power of technology and innovation.

Traditional financial institutions need to undergo digital transformation urgently. This need is urgent because a significant number of these incumbent financial institutions face an existential crisis. Incumbent financial service providers (FSPs) need to acknowledge digital disruption, overcome institutional complacency, and embrace digital transformation if they wish to remain relevant in the rapid evolution of the financial sector.

Picture this: a typical East African traditional bank takes a month to process a working capital loan for an enterprise. On the other hand, an enterprise finance-focused FinTech disburses a customized solution to the enterprise within 24 hours in the form of an invoice discounting product, a factoring product, and an investment finance solution, among others.

Or this: In Kenya, businesses use more than a third of digital credits. This proportion is set to increase significantly as providers nurture and grow their higher value customers with good credit records, and as digitally-transformed incumbents such as Equity Bank extend their lending. These loans are processed and delivered in a matter of seconds. This is likely to leave analog incumbents serving just the lower value, harder-to-reach rural customers, and struggling to break even.

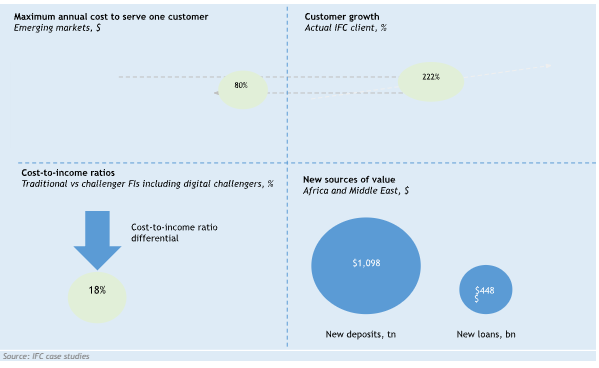

There is still a significant confusion around the business case of digital transformation. Most financial institutions think that digital transformation is a cost. It is important to realize that digital transformation is an investment to future-proof the institution. The International Finance Corporation (IFC) identifies the impact of digital transformation as 1) a reduction in the cost per customer, 2) customer growth, 3) cost-to-income differentials, and 4) new sources of value.

Digital transformation requires a strategic focus on user-centric design, alternative data analytics, personalized experience, robust technologies, and fully automated processes. Against this backdrop, a significant number of FSPs are underprepared and ill-equipped to make use of digital financial services to retain their market share.

From an institutional perspective, financial institutions need to have a clear strategy that defines their digital vision and mission. Most financial institutions end up believing that being digital means offering products through the digital channel. However, they fail to understand that being digital implies offering the right combination of: 1) digital solutions or tools, 2) digital delivery, 3) riding on digital technology, and 4) providing seamless user experience.

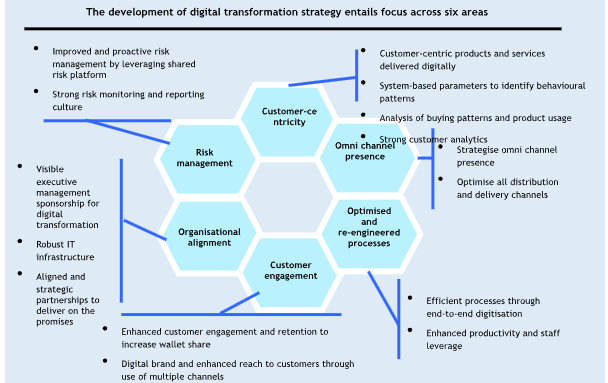

An institution’s digital transformation strategy is anchored on the use of technology to: 1) enhance its business model, 2) expand its scope to offer financial services to other segments than those it traditionally served, 3) increase its scale and outreach, 4) enhance efficiencies of operations, and 5) manage risks effectively. The key pillars of digital transformation strategy design include six areas:

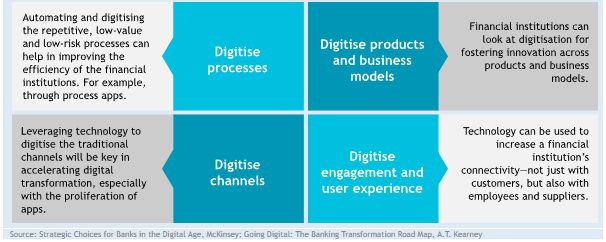

There is no formula on the steps to follow. However, to transform digitally, a financial institution may define an appropriate plan choosing from the four steps as illustrated below.

In the next blog, we explain these steps in detail along with the requirements for a digital transformation.

Written by

Leave comments