Optimizing agent network distribution

by Mohak Srivastava, Karthick Morchan and Akhand Tiwari

by Mohak Srivastava, Karthick Morchan and Akhand Tiwari Jul 31, 2019

Jul 31, 2019 6 min

6 min

Agent optimization is a universal challenge. MSC’s geospatial mapping in two blocks of India sheds light on how agents can be placed optimally.

In the not-so-distant past, India suffered from a severe lack of banking facilities. This was especially true for rural areas, where less than 10%[1] of villages had a brick-and-mortar branch. In 1989, the Reserve Bank of India (RBI) implemented a service area approach as part of its Lead Bank scheme, which was reviewed later in 2004. The introduction of Business Correspondent (BC) agents in 2004 further supplemented the approach (see Appendix).

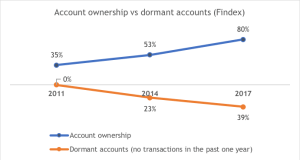

Today, less than 15%[2] of villages in India have a brick-and-mortar bank branch. In most rural areas, a network of 543,472 BC agents primarily drives banking operations and is integral to the business strategy to achieve financial inclusion. However, despite a growth in the number of accounts, the number of dormant accounts in the country increased by 16 percentage points from 2014 to 2017. Hence, optimizing the performance and availability of BC agents becomes important to enable meaningful financial inclusion that goes beyond focusing on access and looks at the use and quality of access.

We undertook this study to optimize agent networks in two blocks—administrative subdivisions that fall under districts—in two aspirational districts in the country. Based on our analysis, a number of trends emerge in the country, which requires specific action plans to enhance financial inclusion:

1. A national-level study is required to understand the true impact of the Sub-Service Area approach for financial inclusion (see Appendix) and to identify the underserved or unserved areas in the country.

2. Efforts are needed to strengthen the supporting infrastructure, which will enable the smooth functioning of existing agents. An example of such a method is agent segmentation, wherein agents are classified into two types. The first type comprises relatively sophisticated sales agents who are usually exclusive to specific financial service providers and are dedicated solely to the agency business. These agents sell products, on-board customers, and conduct transactions of larger value.

The second type comprises basic service agents. These agents are usually non-exclusive, which means they offer services on behalf of a range of financial service providers. They are also non-dedicated, which means that the agency business for them is a marginal, add-on to

another core business, typically in retail. This second category of agents is responsible for conducting typically smaller cash-in and cash-out (CICO) transactions. The sales agents can act as rebalancing points for service agents, which can help solve the problems related to liquidity that agents potentially face.

- Agent segmentation is even more important in areas with underdeveloped agent networks. Segmentation will optimize the spread of agents and ensure maximum population coverage while maintaining agent viability.

- Potential service agents should ideally be already engaged in other businesses in the area. PDS shops, CSCs, and post offices are examples of such potential agents, as identified by MSC’s analysis. Policymakers may wish to develop a framework to identify businesses, establishments, or persons as potential agent types, as proposed in reports published by Helix Institute of Digital Finance and GSMA.

Navapur block in Nandurbar, Maharashtra and Kursakatta block, Araria, Bihar. We mapped the geographical locations of all agent points, bank branches, and post offices and conducted geospatial analysis to understand the current penetration of banking services in the respective blocks. We also mapped non-banking infrastructure setups of the government to explore their potential as an alternative to expand the current outreach of financial services. These included primary health centers, panchayat offices, Public Distribution System (PDS) shops, Common Service Centers (CSCs), and commercial establishments like grocery stores, mobile recharge shops, and computer centers. The sections below provide details of the key findings from both blocks.

In all, nine BC agents are present in Navapur, who cater to a population of 367,443, out of which 85% live in a rural area. Furthermore, most agents are located in clusters around the more urbane establishments in the block. Several BC agents operate from inside a bank branch, which undermines the entire objective of creating such agents in the first place. Hence, it was not surprising to find that for 30% of the total population and 52% of the rural population within Navapur block, the nearest agent was located more than five kilometers away.

Low population densities[3] and an undulating and difficult-to-access terrain are possible contributors to the meager presence of BC agents in the block. The effectiveness of the service area approach in the district, therefore, has been severely undermined. Moreover, the selection of agents in new locations depends on the constraints of access and viability. In such a scenario, non-dedicated agents become the best option to ensure a sustained and well-spread-out presence of agents in the block.

Kursakatta, on the other hand, has 28 BC agents who cater to a population of 149,231. The network of BC agents in this block is well established, with a majority of the villages lying within a two-km radius of existing agents. However, we found disparities in the replenishment of cash reserves by the BC agents. Given that the block has only two bank branches, almost half of the BC agents in the block have to travel more than five kms to reach their nearest rebalancing point. Optimizing agent performance becomes necessary in this case by reducing the loss of person-hours, which currently occurs due to the long trips to bank branches. At this point, we must consider the ANA India Report-2017, which revealed that 74% of BC agents across India face challenges in the rebalancing process, with long travel time being the major barrier.

The agent mapping study sought to understand the current landscape of financial services in the two blocks, potential new agent locations if any, and potential agent types. We conducted the geospatial analysis required for this study by using QGIS and collected the data by using ODK Collect and GPS Essentials mobile apps. Deep-dive analytics such as this reveals much more granular and contextualized data than what macro- or country-level data can yield. Information from such studies will enable policymakers, regulators, and development agencies to make better, evidence-based decisions to direct their resources towards holistic financial inclusion, especially in underserved areas.

Interactive online maps that illustrate the current financial landscape of the two blocks covered in this study can be found here—Navapur and Kursakatta. The “Map & Tools” option in the top-right corner of the link lets you select different features, and visualize and generate insights.

Appendix

Service Area Approach: The approach came into effect to address the lack of banking facilities in the country and to allow people in rural areas to gain access to formal financial services. Under this approach, a designated public sector bank, including regional rural banks, should cover 15-25 villages for their planned and orderly development. The proximity to a branch and contiguity of villages are the main criteria to allocate villages to each bank branch. All 600,000 villages across the country have been mapped according to the service area approach. Every bank branch needs to have at least one fixed-point banking outlet that caters to 1,000 to 1,500 households, which is called a Sub Service Area (SSA).

Business Correspondents (BCs): BCs are banking agents who provide basic services like cash-in cash-out (CICO), account opening, funds transfer, and balance inquiries. BCs enable a bank to expand its outreach and offer a limited range of banking services at a low cost.

_______________________________________________________________________________________________

[1] India has 649,481 villages as per Census 2011, of which 593,615 are inhabited. As of 2012, 75,801 bank branches operated in rural areas. Hence, assuming no village has more than one branch, brick-and-mortar branches cover, at best, 7.8% of inhabited and 8.5% of total villages. The real figures will be even lower if, for example, a single village has two or more branches.

[2] Between 2013-2014 and 2016-2017, 8,588 new banks opened in rural areas. Hence, the total number of banks that operate in rural areas became 84,389. The rest of the calculations remain the same.

[3] The population density of Nandurbar is 277 per sq.km., which is much lower than the population density of its parent state, Maharashtra, at 365 per sq.km.

Leave comments