Fundfina: A journey to tap a hidden multi-million MSME market in India

by Mitali and Disha Bhavnani

by Mitali and Disha Bhavnani Aug 16, 2021

Aug 16, 2021 6 min

6 min

Fundfina is a digital lending platform providing access to formal credit to micro and small enterprises (MSEs) in India. This blog explores Fundfina’s journey and the positive impact it hopes to create on the MSE sector of the country.

This blog talks about Fundfina, a startup that is part of the Financial Inclusion Lab. The Lab is an accelerator program supported by some of the largest philanthropic organizations across the world, such as the Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation, and Omidyar Network.

“I will never come out of this vicious cycle”, says Rajan Lal, 36, who runs a small kirana shop in Bihar’s Mithapur area. On average, Rajan sees 20-30 customers visit his shop and buy goods worth around INR 3,000 (USD 41) each day. While setting up his business, Rajan did not even consider seeking credit from a formal financial institution because he had always heard that formal institutions only finance bigger businesses. Moreover, since Rajan’s business was new, he lacked sufficient documentation for proving the business’s eligibility for a bank loan. Thus, approaching a bank was out of the question.

Rajan used up all his savings and liquidated the land he inherited to meet the initial cost of setting up his business. During festive seasons, he makes brisk sales and rotates the inventory well. Faster rotation of money and a decent profit help Rajan repay supplier credit in time. However, sales and profit drop during the lean season. This forces Rajan to borrow money to replenish the working capital to keep his business afloat.

To borrow for working capital, Rajan reaches out to friends and informal moneylenders during the lean season. The money lenders charge usurious rates of interest and often demand untimely repayments. Many a time, he is forced to clear off the debt and harassment from one moneylender by taking on a fresh informal loan from another lender. Thus, the cycle of borrowing continues.

The burning question is: Can Rajan come out of this vicious cycle of borrowing?

Dismal access to credit

Rajan’s credit problem is, unfortunately, a norm rather than an exception. India is home to 64 million micro and small enterprises (MSEs) run by people like him. Although MSEs contribute significantly to the economy and employment, several factors obstruct their access to formal financial services. Most MSEs lack any formal or documented financial history. This affects their ability to borrow from formal lending sources or institutions. Moreover, such institutions hesitate to serve this segment due to the high cost of acquisition (CAC) and high operational costs.

Despite the government’s concentrated efforts to increase the number of financing options for MSEs in recent years, the addressable credit gap in the MSE sector is estimated to be INR 30 trillion (USD 401 billion).

Fundfina’s eureka moment

Before founding Fundfina, the five co-founders had known each other for more than a decade—either since their kindergarten days or as a result of working together. But what triggered them to join forces and found Fundfina?

Rahul, one of the co-founders, started a small business and like most of India’s MSE owners, faced an issue with availing formal credit. Intensive documentation, long turnaround time (TAT) in processing and decision making, and the hassle of in-person visits made his entrepreneurial journey tedious and his dreams frustratingly distant. Rahul wanted to overcome such barriers not only for his enterprise but for other MSEs as well and got into discussions with the other co-founders. They saw this as an opportunity to have a positive impact on the lives of millions of such entrepreneurs. And thus, Fundfina was born.

Bringing in the change

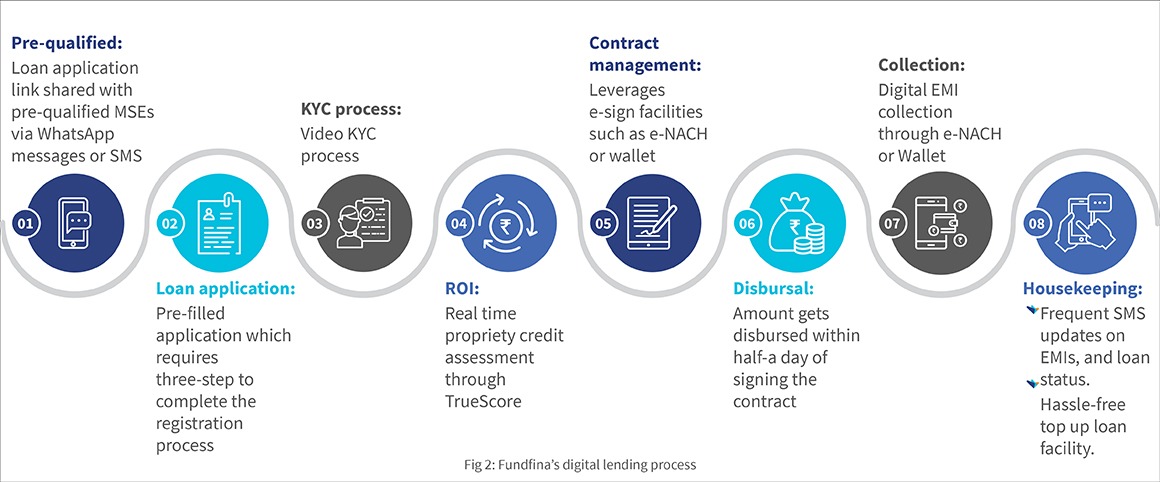

Founded in 2017, Fundfina is a digital lending platform focused on economical MSE financing that rides on alternate data and deep technology employing artificial intelligence and machine learning (AI/ML). The entire process is digital, starting from loan origination to disbursal. It addresses the unmet credit needs of the MSE segment by providing easy, cost-efficient, and technology-driven financing solutions.

Fundfina’s lending model is built on the pillars of accessibility, affordability, and appropriateness.

Accessibility

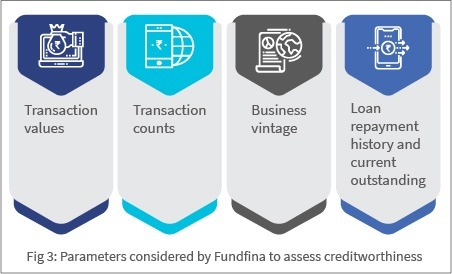

Formal institutions demand several documents, such as income tax returns, GST registration of the business, and previous transaction history, to assess the creditworthiness of MSEs. In contrast, Fundfina uses alternate data through its proprietary tool, TrueScore, to assess MSEs using an additional set of parameters (shown in the figure below).

Affordability

The loan amount and interest rate for each borrower are decided based on their TrueScore assessment score which takes into account the MSE’s repayment capacity. Partner microfinance institutions disburse the loan into the borrower’s mobile wallet or bank account within 12 hours of approval.

Appropriateness

Fundfina understands that there is no one-size-fits-all solution for different MSEs. Hence, it offers a range of customized unsecured financing products, including short-term working capital and long-term financing with a flexible repayment schedule, for each MSE segment. Fundfina understands the volatility involved in running small businesses and, therefore, offers cash-flow-based lending.

TrueScore assesses the amount of credit for which an MSE is eligible based on the business’s repayment capacity. This mitigates delinquency and default rates and enables the borrower to build a strong credit history. The startup also supports MSEs during financial adversities by offering payment holidays and offline agent support through its partner microfinance institutions.

The impact made on the LMI segment

Ninety percent of Fundfina’s customers are small enterprises. The borrowers are from suburban towns and villages, and 80% are sole proprietors typically running unregistered businesses.

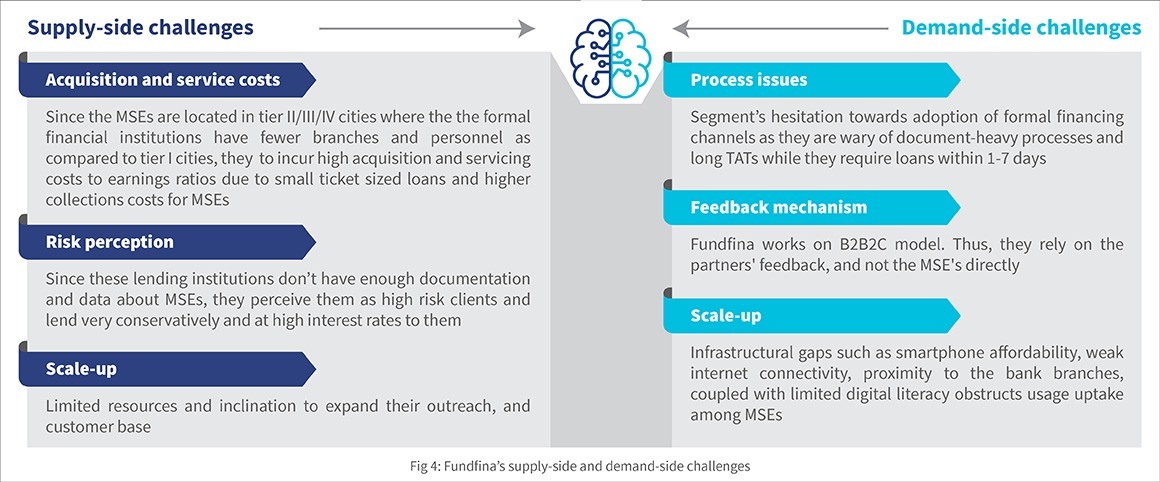

The roadblocks: Fundfina’s path to success has not been easy

Fundfina addresses these challenges as described below:

Addressing supply-side challenges:

- Reduced CAC through partnerships with hyperlocal players: Fundfina has been partnering with several MFIs and on-ground institutions. Under this B2B2C model, the onus to collect repayment is on the partner MFI, which reduces the overall cost of acquisition and serving the customers.

- Risk Mitigation: Fundfina does not lend on their loan books. The partnership-based model helps to mitigate the delinquency risk from the borrowers, and thus reduce operational costs.

- Revenue stream: Besides their supplier lending partners, the startup also commercializes its proprietary tool “TrueScore” by sharing application programming interfaces (APIs) that can be used by other FinTechs. Their “Lending-as-a-service” APIs help FinTechs and other lending enterprises to offer quick and flexible credit to MSEs. The stack automates the entire lending process from application submission to credit disbursement. This provides a convenient yet robust lending tool for their partner institutions and generates additional revenue for the Fundfina team.

Addressing demand-side challenges:

- Handholding support: Fundfina leverages the knowledge and market intelligence of its partners’ field staff to add new-to-credit customers to its list and to get feedback from the end-client MSEs on the current offerings. The phygital approach ensures adequate handholding support is extended to

- Curated lending products: Fundfina offers need-based customized financial products. This helps MSEs understand and appreciate the convenience that formal financing offers, and simultaneously spreads positive word of mouth for the startup. With this, the startup continues to actively explore new avenues to boost its business, even as it keeps existing customer segments engaged.

Support from the FI Lab

Fundfina’s passion to serve the MSE segment inspired them to seek a nuanced understanding of the MSEs’ pain points and expectations, and to continue building customized and impactful solutions for them.

To fulfill this objective, the FI Lab through CIIE.CO and MSC provided mentoring support, and boot camp sessions on relevant business topics. MSC, leveraging its Market Insights for Innovations and Design (MI4ID) approach, gathered insights around the perspective of MSEs on Fundfina’s current financial product offerings and also identified tweaks to make the offerings relevant. The support also helped Fundfina to understand the segment-specific behavior, biases towards digital financial products, and their readiness to adopt them.

The road ahead: Scaling responsibly

Over the next five years, Fundfina plans to reach 10 million micro-merchants and a portfolio of USD 1 billion. Fundfina aspires to become a one-stop-shop for micro-merchants that goes beyond credit and offers a suite of financial and tech-based products in insurance, current and savings accounts, expense management, and inventory tracking, among others. The road ahead for the Fundfina team may be long, winding, and occasionally treacherous but the team is ready for the ride! This will surely help millions of Rajans and their MSEs to continue to plug the gaps in India’s growth story.

This blog post is part of a series that covers promising FinTechs that make a difference to underserved communities. These start-ups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

Written by

Mitali

Manager

Leave comments