Credit for low- and moderate-income people in Bangladesh—can new-age banks and FinTechs deliver the regulator’s wish?

by Anik Muntasir Chowdhury, Samveet Sahoo and Sunil Bhat

by Anik Muntasir Chowdhury, Samveet Sahoo and Sunil Bhat Jan 24, 2022

Jan 24, 2022 5 min

5 min

The waves of digitization and technological advancements have led to the opening of MFS accounts for 60% of the population in Bangladesh. The country now boasts more than 1.1 million agents. Despite the widespread use of MFS and internet access, only 9.1% of people access the formal credit system. Digital credit can be a stepping-stone in Bangladesh due to the lower cost of delivering credit through digital means, combined with the mass digital readiness of consumers. Several solutions have emerged from banks, NBFIs, FinTechs, MFSPs, MFIs, and development partners, such as City Bank’s “Nano Loan” product pilot to Prime Bank’s loan product for blue-collar workers. Together, stakeholders are trying to forge partnerships to address problems around access to credit and social development in Bangladesh.

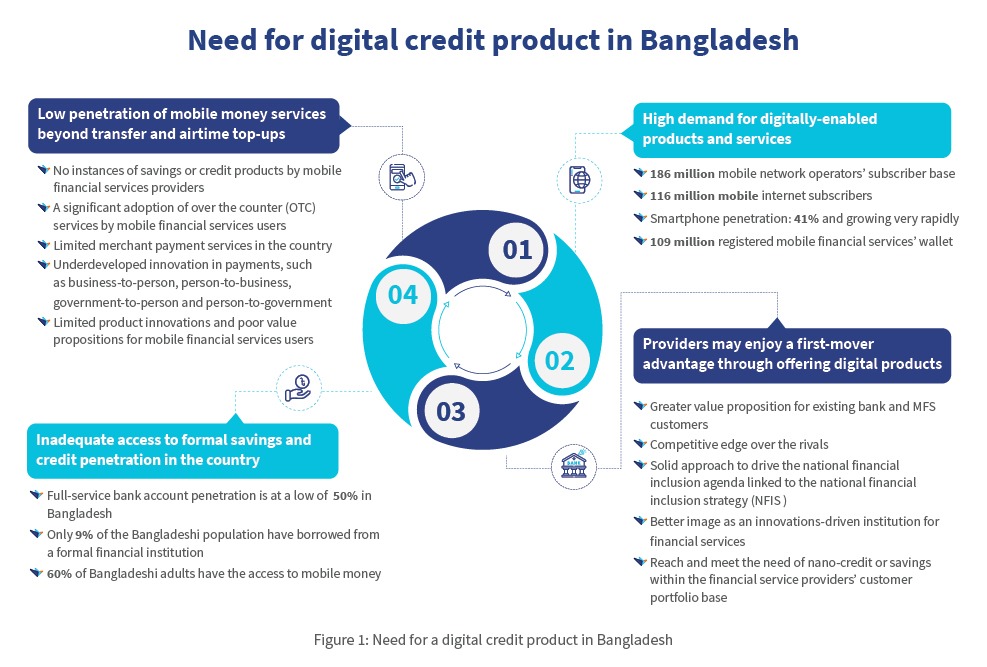

These days, “amake bKash kore dao” in Bangladeshi parlance means “send me money through bKash.” Mobile financial services (MFS) are so prevalent in Bangladesh that the market leader is synonymous with them. Despite the deep reach of MFS, World Bank data suggests access to accounts remains limited to just 50% of the population. However, access to formal credit is minimal: only 9.1% of the population have borrowed from the formal sector, as per the World Bank’s Global Findex database.

As the economy moves forward, particularly after the COVID-19 pandemic, low- and moderate-income (LMI) people need credit to rebuild their lives and livelihoods. This need for credit has created a demand-supply gap since banks often fail to cater to the credit needs of the LMI segment due to four reasons:

- Lack of documentation—missing paperwork from the applicant and assets for collateral;

- Information asymmetry—difficulty in assessing credit applications due to limited publicly available information and digital footprint;

- LMI is viewed as a low-return segment—banks perceive the LMI segment as an unfavorable business case due to the nominal loan origination fees for small-value loans;

- Highly risk-averse nature of banks—that demand collateral to mitigate risk with little or no customization of the product.

Micro and small enterprises (MSEs) also struggle with a lack of access to credit for similar reasons. They need working capital credit to survive regular business volatility and increase their growth. Both LMI and MSE segments also require loans to withstand economic shocks in response to the pandemic. Digital solutions can emerge as frugal, disruptive, and effective solutions to address the demand-supply gap in credit requirement, given the difficulty of reaching the customers with these loan products.

Bangladesh has a burgeoning digital landscape, but challenges remain

Bangladesh already has a high demand for digitally-enabled products and services. Data from the Bangladesh Telecommunication Regulatory Commission (BRTC)suggests the country has 126 million active internet subscriptions, of which 92% are mobile-based. With growing internet penetration at 60%[1], Bangladeshis are more connected than ever. Approximately 60% of the adult population has active MFS accounts, with more than 1.1 million agents spread across the nation. However, despite this high penetration, MFS use-cases remain limited. As of 2021, 95% of all transaction value is basic cash-in, cash-out, or P2P payments. Only 5% are other use-cases such as utility bills, merchant payments, salary, and government disbursements.

While the unfulfilled need for credit among LMI remains high, banks and MFIs find it less cost-effective to reach the excluded segment. In contrast, 36.8% of people have borrowed money from other informal sources. These other sources can be family, acquaintances, informal lenders, or local samitis (cooperatives) that offer credit. In the absence of any verifiable record of these transactions, those borrowing in the informal sector cannot build a credit history to avail credit from formal financial sources in the future.

Digital credit in Bangladesh, multiple experiments, and an opportunity

As mentioned in the figure below, there are many reasons to explore digital credit in Bangladesh.

In response to this opportunity, a few players ran pilots in 2020. In July 2020, City Bank launched a “Nano Loan” product pilot, collaborating with the leading MFS provider, bKash. Upon completing the pilot, City Bank launched the product targeting LMI users who seek small consumer loans in December, 2021. The product is only available for bKash app users registered using eKYC. Similarly, Prime Bank introduced a nano loan product in 2021 for blue-collar workers. Both banks offered their products through mobile applications.

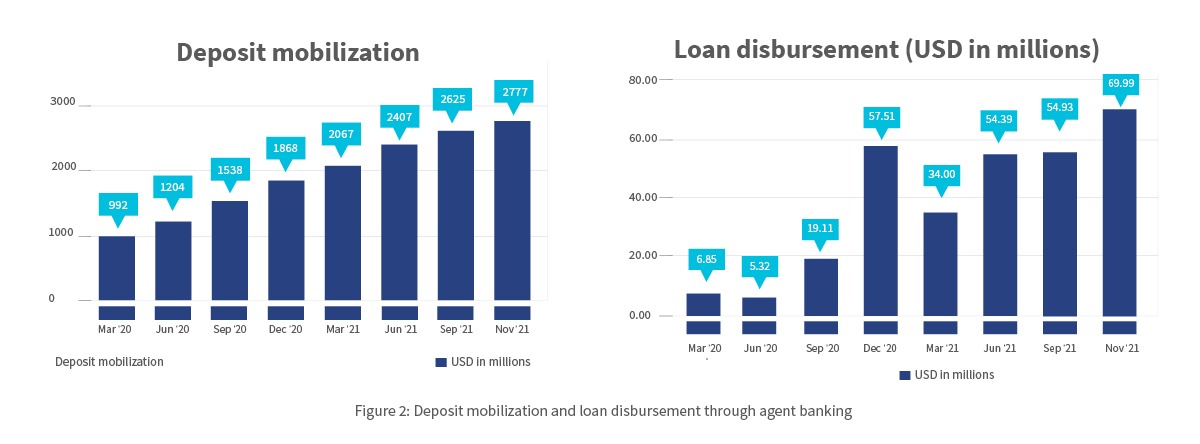

Besides the app-based lending channel, agent banking is another established avenue for providing credit to the underbanked segments, especially in rural and semi-urban areas. The rapidly emerging agent banking network provides robust distribution across the country. The agents themselves are capable advocates for financial products, including credit. The agent banking business collected deposits up to USD 2.59 billion across all accounts as of November, 2021, with a low credit-to-deposit ratio of only 2.52%. This shows an immense opportunity for future growth.

Do we have an enabling ecosystem?

Digital credit promises to deliver small-value credit at a lower cost.

Bangladesh Bank allowed banks to issue loans to the cottage, micro, small and medium enterprises (CMSMEs) under the government’s BDT-200-billion (USD 2.36 billion) stimulus package. This directive from the central bank highlights that 80% of the market consists of cottage, micro, and small enterprises, many of which need credit. The directive seeks to reduce banks’ risk of lending to CMSMEs as the government subsidizes 5% of the 9% interest rate.

Financial service providers have an opportunity to serve other LMI segments, such as students, readymade garment workers, and farmers. While Bangladesh Bank successfully launched eKYC guidelines for opening bank accounts, it is yet to make the loan application process easier. Earlier, MSC assessed the eKYC pilot in 2019 and highlighted opportunities to reduce the complexity of paper-based loan applications from 14-plus to two pages.

Furthermore, the digitalization of loan applications and assessment could significantly increase the probability of loan application approval among MSMEs. But concerns persist around accepting third-party data, proof of address, proof of identity, guarantor details, and nominees as part of the application process for digital borrowers. Bangladesh Bank’s forthcoming directive on digital credit operations may address these issues.

Digital onboarding, supported by eKYC and technologies, such as artificial intelligence and machine learning, could further simplify the loan application process and facilitate subsequent stages of loan operations.

Bangladesh Bank has also explored new channels to deliver financial services, such as neo banks. Bank Asia is one of the early adopters interested in forming a neo bank, the first in Bangladesh. In contrast to conventional banks that attach accounts to physical branches even if customers opt for internet banking, neo banks do not attach accounts to branches. When neo banking platforms gain momentum, they can potentially start offering small-ticket lending, such as retail and micro-credit, with minimal bureaucratic processes.

The road ahead

The market demand for credit remains high in Bangladesh. The country now has some of the building blocks to enable digital credit. However, any new product or platform requires careful regulatory assessment to protect consumers from potential predatory practices. The Bangladesh Bank will need to prioritize consumer protection and enable a responsible and responsive digital credit system. They must learn proactively from other markets like Kenya. Bangladesh Bank has already taken the first step by establishing the Regulatory FinTech Facilitation Office (RFFO) in 2019. The RFFO allows providers to test innovative ideas before they take them to the mass market.

The digitalization of credit should be a means to lower cost and make credit instant, automated, and remote. These three attributes differentiate digital from traditional credit, making it an easily scalable solution for LMIs and CMSMEs.

In Bangladesh, digital credit is no longer a question of “if” nor a question of “when.” Still, now more prominently than ever, it is a question of “how fast and how much” to suit the requirements of LMIs and CMSMEs.

Banks, NBFIs, FinTechs, MFS providers, MFIs, and development partners are all scrambling to forge partnerships and scope out opportunities to improve Bangladesh’s access to credit. MSC supports several leading banks, FinTechs, and development partners to usher in nano-credit. It will not be surprising if “nano” becomes the next buzzword from 2022, a decade after MFS became a household name.

[1] BTRC considers an internet subscription as active for customers who have accessed the internet at least once in the past 90 days. The mobile internet penetration covers all subscribers including multiple subscriptions.

Leave comments