How can financial institutions provide handholding support for the elderly?

by Devraj Hom Roy and Vishes Jena

by Devraj Hom Roy and Vishes Jena Sep 6, 2022

Sep 6, 2022 6 min

6 min

Bhupen, a young chef from Tripura, India, uses mobile apps for remittances, as well as merchant and bill payments. He has grown fond of digital payments after his coworkers in New Delhi introduced him to payment apps. However, he discovered a different situation when he returned home to Tripura during the second wave of COVID-19. He tried to introduce his elderly father to the mobile-based payments ecosystem after seeing him risk infection to make monthly recurring deposit (RD) payments in the post-office. Bhupen and others highlight the digital revolution brewing in rural Indian households. This blog examines how we can replicate this approach beyond India to extend digital financial services to the elderly and make them digitally self-reliant.

Bhupen, a 23-year-old from Tripura, is a full-time owner and chef at a small eatery in New Delhi. He has earned a reputation as one of the best chefs in the area for budget Chinese takeaways. Bhupen’s job keeps him busy since the cafe is located near a popular corporate office. This leaves him with few opportunities to visit his family back in Tripura.

Bhupen, a 23-year-old from Tripura, is a full-time owner and chef at a small eatery in New Delhi. He has earned a reputation as one of the best chefs in the area for budget Chinese takeaways. Bhupen’s job keeps him busy since the cafe is located near a popular corporate office. This leaves him with few opportunities to visit his family back in Tripura.

An overview of the scenario in Bhupen’s household

During the second wave of COVID-19 in 2021, the offices around Bhupen’s cafe were closed, and his business came to a grinding halt. The crippled economy forced Bhupen to shut shop and move back to Tripura.

Bhupen found himself in a completely different world back in his home state. He realized this when he heard that his father, Bipin, braved the risk of infection and queued up at the local post office to pay his monthly recurring deposit (RD). Bhupen was shocked. After all, Bipin was not a novice smartphone user—he used it to access social media platforms, such as Facebook and Instagram.

For Bhupen, saving monthly deposits is as easy as opening an app and typing the security PIN. Bipin should not have to stand in queue for something that seemed relatively trivial in Bhupen’s world. Despite the gloomy environment of the second wave, Bhupen decided to make the most of his time at home. He prioritized teaching his family a few basic digital use-cases. However, Bhupen could not find a way to make the post-office RD payments in any of the popular payment apps he used.

It did not take long for Bhupen to find a solution. When travel restrictions prevented Bipin from reaching the post office, an opportunity presented itself.

Before proceeding with Bhupen’s story, let us give you some context. In India, it is easy to assume that people must be willing to welcome convenient mobile-based platforms, such as Unified Payments Interface (UPI), or third-party apps like Paytm, or Google Pay, which offer integrated services. This was not true in Bipin’s case.

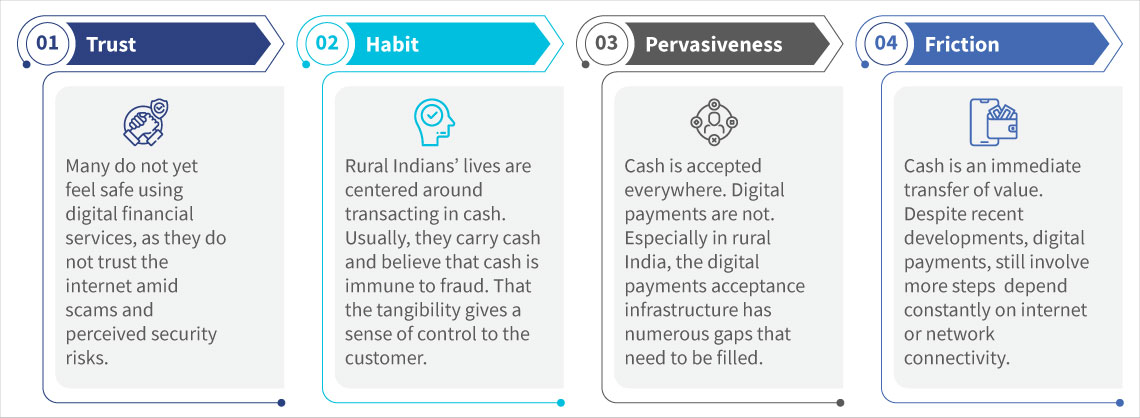

While he knew of the possibility of paying bills and monthly deposits from the comfort of his smartphone, he was risk-averse, did not trust digital financial transactions and lacked operational knowledge of such platforms. As a result, Bipin labeled himself as digitally illiterate. Such hesitation is common among low- and moderate-income (LMI) customers. We can break down the struggles of this customer segment into four key challenges.

Figure 1: Rural India’s challenges in adopting digital payments

An average smartphone user’s journey to digital payments

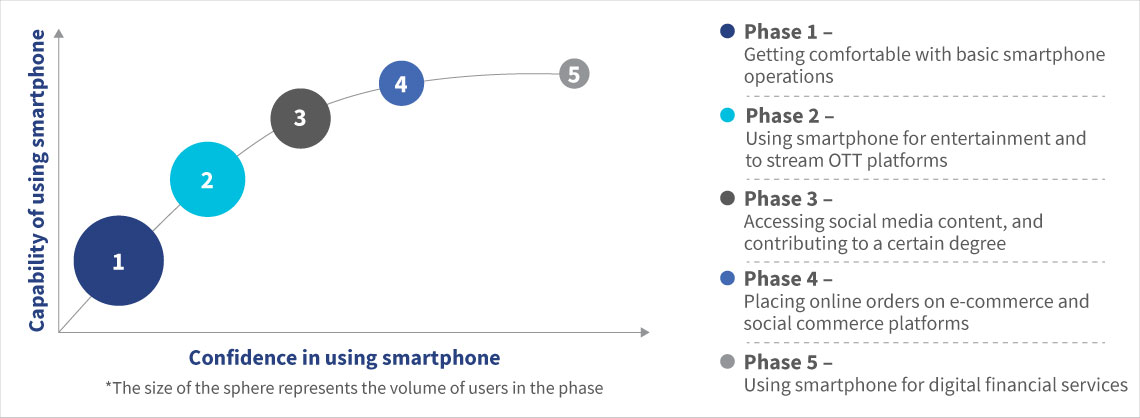

The rate of smartphone penetration in India has increased exponentially. It currently stands at 54% and will reach 96% by 2040. However, smartphone penetration in itself may not translate to an increase in digital payments and digital banking.

If we want every smartphone-equipped Indian to use digital payments, firstly, we need to understand an average smartphone user’s journey. Digital readiness is a continuum, which, when plotted across the axes of capability and confidence in using a smartphone, results in five phases as depicted in the graph below. MSC has seen these five phases replicated across Asia and Africa.

Figure 2: Path of the digitally ready to digital payments

- In phase 1, all users try to get comfortable with basic operations, such as placing calls, exchanging SMSs, installing applications, using WhatsApp, using the camera, and navigating the user interface. Millennial and Gen-Z smartphone users, such as Bhupen, can navigate their smartphones easily. Hence, they quickly transition to phases 2 and 3.

- In phase 2, users adapt to their smartphones for entertainment without incurring any significant additional cognitive load. This is when they start surfing video-streaming platforms, such as YouTube, web-based over-the-top (OTT) entertainment platforms, and music applications.

- In phase 3, users gain more confidence as they sign up on social media platforms, such as Facebook and Instagram, where they consume digital content and contribute to it in various degrees. Most users usually limit their smartphone usage up to this phase. They do not feel comfortable moving beyond this usage level, as they have a higher perceived risk of fraud and fear making unintentional mistakes that would put their money at risk.

- A comparatively smaller portion of users climbs to phase 4, where users can place online orders on e-commerce and social commerce platforms, such as Amazon, Flipkart, and Meesho. While users in this phase can operate their smartphones, they lack the confidence to make digital payments. Hence, while they may place the orders online, many opt for cash-on-delivery. Most netizens in rural India hold back from making digital payments.

- A tiny proportion of users like Bhupen manage to advance to phase 5. Factors, such as social proof, age, assistance from a trusted network, and convenience often propel this journey. This stage is characterized by users first making digital payments wherever possible, followed by advanced digital financial service (DFS) use-cases, such as opting for digital credit, digital savings, and digital insurance through a smartphone.

Bhupen ignites a digital revolution at home

Now, let us get back to Bhupen.

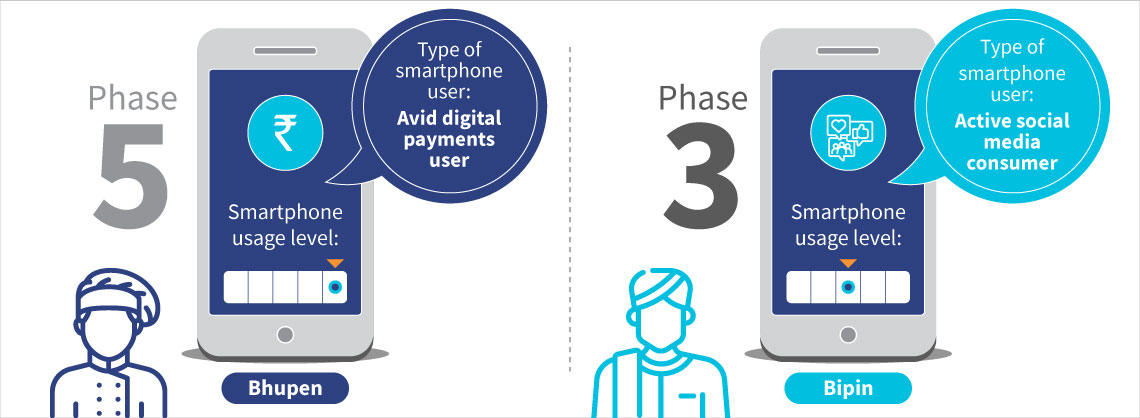

Figure 3: Level of smartphone usage by Bhupen and his father

Figure 3: Level of smartphone usage by Bhupen and his father

Bhupen knew of his father’s digital readiness. Hence, he was optimistic that he would be able to nudge Bipin to use digital payments for his RD deposits.

Unable to find a way to pay digitally through the payment apps, Bhupen approached Rakesh, the local Grameen Dak Sevak (postperson) and family friend. Rakesh suggested Bipin to open an India Post Payments Bank (IPPB) savings account, which offers digital payment options for popular post office small savings schemes. Rakesh offered doorstep banking services through which Bipin could pay in an assisted mode.

Rakesh used his handheld device to authenticate Bipin’s biometrics and opened a savings account for him. In a few minutes, he completed the electronic KYC without any papers, on-boarded Bipin, and linked the RD to his savings account. With Rakesh’s help, Bipin could now make Aadhaar-enabled payments from his IPPB savings account to the connected RD account through the Aadhaar-enabled Payments System (AePS). The ease of the process, the empathetic Grameen Dak Sevak, and the assisted onboarding mode won Bipin over. Bipin was on his way to phase 5.

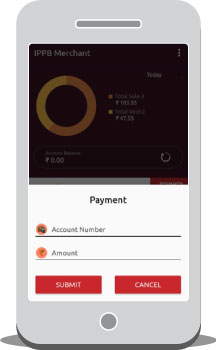

Figure 4: RD collection screen on the IPPB agent application

Was this all that the digital payments ecosystem had to offer to Bipin?

No … Bhupen was convinced his father could move to a self-service payment mode. After all, readiness to use self-service platforms, such as mobile apps, is more likely to lead to repeat use and graduation to more digital use-cases.

After the second wave of the pandemic receded, Bhupen returned to New Delhi as business resumed. One day, as he was about to pay his electricity bills, he started worrying about his parents back home. Bhupen called his father and was in for a pleasant surprise when Bipin revealed that he has had figured out how to pay household bills through the IPPB mobile app. With Rakesh’s support, Bipin downloaded and started using the IPPB mobile banking app. Hence, Bipin paid last month’s RD, electricity bill, direct-to-home (DTH) television bill, and gas bill through the app. Bipin was truly on his way to phase 5 now.

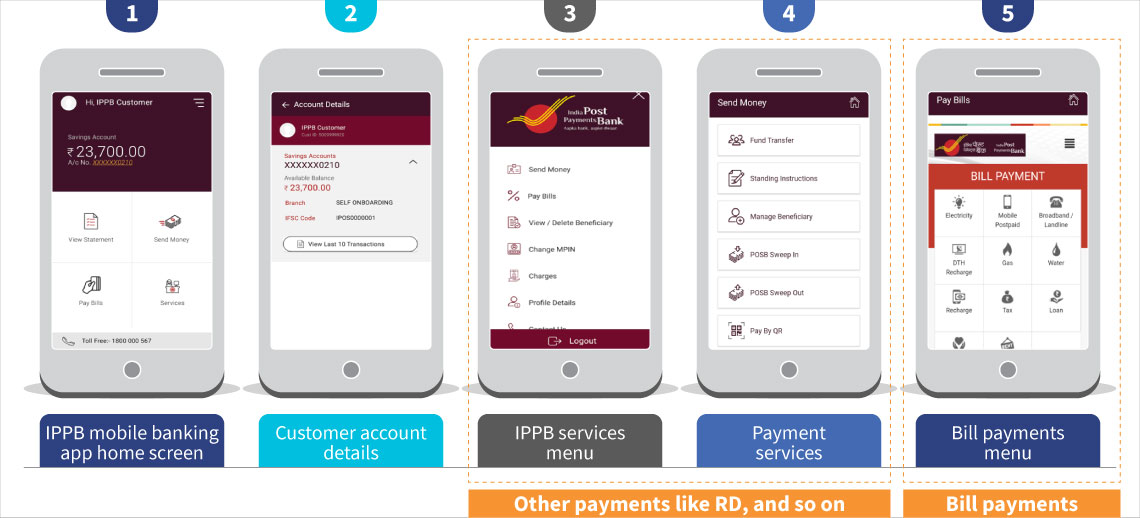

Figure 5: IPPB mobile banking application – services menu

Figure 5: IPPB mobile banking application – services menu

Fast forward to the present date, Bipin pays most of his bills and makes deposits digitally through the IPPB mobile banking app from the comfort of his home. This would not have been possible if Bhupen had not initiated a digital revolution at his home and a helpful postal agent had not handheld his father onto mobile banking. Millennials like Bhupen, ably supported by financial institutions like IPPB, play a crucial role in onboarding middle-aged and senior users onto the digital payments ecosystem.

Watch this short video below to see how IPPB has enabled young Indians like Bhupen to become “mobile-first” and helped them onboard their households onto digital platforms.

Written by

Leave comments