Our new report looks at how digital platforms are reshaping microenterprises in Bangladesh across the retail, transportation, and social commerce sectors. These platforms emerged as major income sources for transporters and social sellers, while retailers relied on them most during the pandemic. Retailers prioritize buy-now-pay-later options; transporters depend on auto companies, while social sellers increasingly use platforms to establish connections with formal credit. Convenience features, such as doorstep delivery, return-trip support, analytics, and fair policies, strengthen loyalty. We explore these dynamics in more detail in the full report.

Blog

Building blocks of AgriStack – Crop sown registry

The agricultural sector in India provides livelihood support to approximately 42% of the population and accounts for 18% of the country’s GDP. With approximately 58% of India’s land dedicated to farming, it is a laborious task to track what is being grown. As per the Agriculture Census, India had nearly 146 million operational landholdings during 2015–16, each of which must be tracked to record what is planted in each cropping season.

Conventional systems of crop survey, which include Girdwari, rely on manual record-keeping methods. This system faces multiple challenges, such as approximations, memory lapses, and damaged paperwork. The Village Revenue Officials (VROs) conduct Girdawari. They record crop details, reviews, and update land records, which include ownership information and revenue assessment. Additionally, as part of the crop survey, they follow a sampling method based on grid selection by the statistics department, with grids varying based on irrigated and non-irrigated areas.

While Girdwari remains essential for administrative purposes, it has significant limitations in terms of accuracy, timeliness, and standardization. Digital records of seasonal crop sowing in agricultural plots across the country are necessary to overcome these limitations. The crop sown registry under AgriStack provides a continuous recording system that records information at different stages of cultivation. The registry maintains a historical, plot-level record of key details, such as when, where, and what crops are planted in each cropping season. It creates a detailed record of plot-level agricultural activity.

This registry serves as a national database of all crops grown in the country. It lists their scientific and regional names and assigns each a unique crop ID. At present, crop data collected by states often differ in terminology and classification. For example, the same variety of paddy or maize may be known by several local names across districts, a variation that is reflected in state-level records as well.

The Crop Registry addresses this issue through a standardized taxonomy that ensures consistent and accurate crop records. Beyond standardization, the registry supports the discovery of new varieties and hybrids. New crops that emerge through local innovation or research can be added to the database with relevant metadata. This database ensures that India’s agricultural data ecosystem remains current and inclusive.

Once these crop taxonomies are standardized, the system can improve production forecasting, crop insurance pricing, and credit access. It also enables early warning systems for crop failure. Together, these improvements enhance interoperability across digital platforms and support better coordination among stakeholders.

Built on this foundation, the Digital Crop Survey (DCS) application established the crop sown registry. The objective of the DCS is to obtain an accurate view of all crops grown on all land parcels nationwide. The application uses geofencing and AI-based image processing technology to ensure the legitimacy and reliability of data collected. This approach reshapes how farmers, government agencies, and businesses interact with agricultural data. The crop sown registry offers greater flexibility than earlier registries.

The registry also updates every crop season cycle based on the crops sown by the farmers on their plots. For every surveyed farm plot, it captures details, such as farmer ID, farm ID, village local governance code (LGD), year, cropping season, crop ID, sown area, date of sowing, and geotags.

The Government of India has developed a central reference application to conduct the DCS. States can either use the reference application or modify their existing applications to meet the technical requirements. The DCS application uses farmer and farmland data from the revenue records, along with geo-referenced village maps, to generate maps of owner plots and record crop sown information at the plot level. The village maps and farmland plot information are integrated directly into the crop survey system before each season. Once integrated with the farmer registry and the geo-referenced village map registry, it retrieves farmer details, farmland data, and geo-coordinates directly.

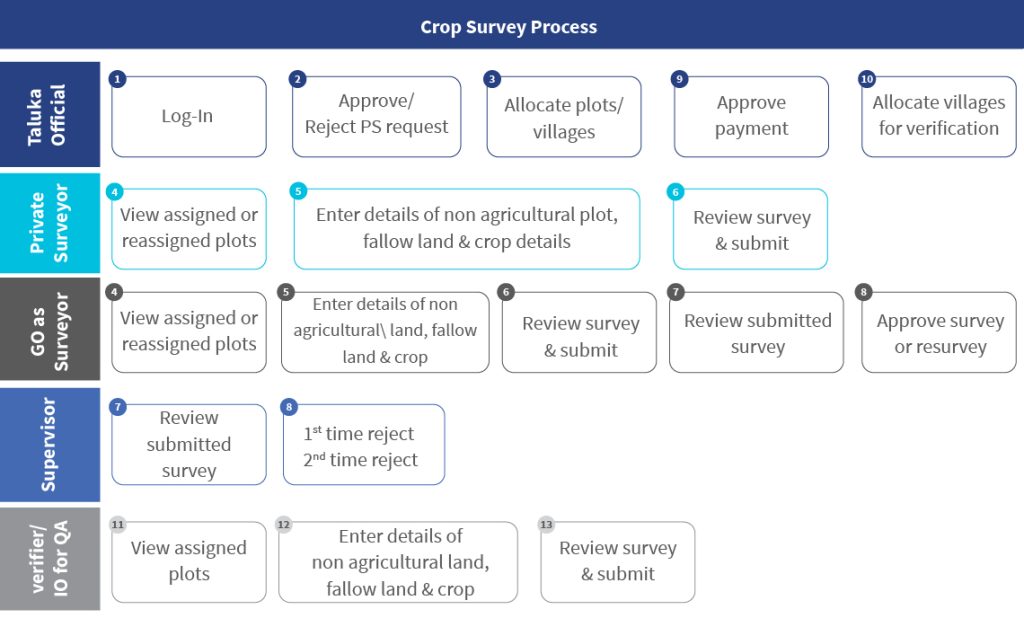

The DCS is a time-bound exercise, usually completed within 45 days of initiation. Surveyors collect and verify data in multiple stages, and supervisors review samples for quality assurance. Inspection officers also conduct mandatory checks on at least 20% of villages each season to ensure accuracy and consistency. This process ensures accuracy and consistency in the data collected. The central government or state governments will also appoint an inspection officer for quality assurance (QA). The inspection officers must perform QA checks on a minimum of 20% of the villages in each taluka every season. This layered review ensures data accuracy and consistency. This process ensures accuracy and consistency in the data collected. The central government or state governments will also appoint an inspection officer for quality assurance (QA). The inspection officers must perform QA checks on a minimum of 20% of the villages in each taluka every season. This layered review ensures data accuracy and consistency.

Despite its potential, the crop sown registry and the DCS implementation face multiple challenges that require careful planning and coordination. Some of the significant challenges are highlighted below:

- Pan-India availability of digitized and geo-referenced maps:

The biggest challenge in the creation of a crop sown registry is inconsistent geo-referencing across states. Some have precise data at the plot level, while others only map at the village level, which affects accuracy. If major shifts in geo-referencing remain unaddressed, data will be recorded against incorrect plots. Standardized nationwide geo-referencing is crucial to track crops, yields, and trends effectively.

- Complexity of land ownership issues:

One of the major issues with the digital crop survey is land ownership. There are situations where the land is in the name of a family member. Yet, the legal heir carries out cultivation. The subdivision may not reflect as a single plot on the map. Additionally, land possession often differs from the official owner listed in the record of rights. These land issues must be kept aside for crop recording. The government conducts surveys against the plot instead of the owner’s name, so in the owner’s name column, it appears like “owner of plot no. 10.”

- Complexities in crop taxonomy:

Diverse crop varieties across regions present a significant challenge due to the presence of numerous sub-varieties and hybrids. Accurate documentation requires detailed data collection, agronomic expertise, and efficient processes. Streamlined data entry, proper training, and validation are essential for accuracy.

- Integration of states with the existing DCS apps:

The integration of the DCS apps by states with existing digital survey systems, such as the MP Kisan app in Madhya Pradesh, the e-Pik Pahani in Maharashtra, or the Bele Darshak in Karnataka, poses a significant challenge. These states already have well-established and mature DCS applications, each with its unique platform, database schema, and architecture. The seamless integration of these diverse systems into a unified registry requires careful consideration and a clear migration strategy.

These challenges must be addressed to ensure reliable data for policymaking, effective resource allocation, and targeted support programs for farmers.

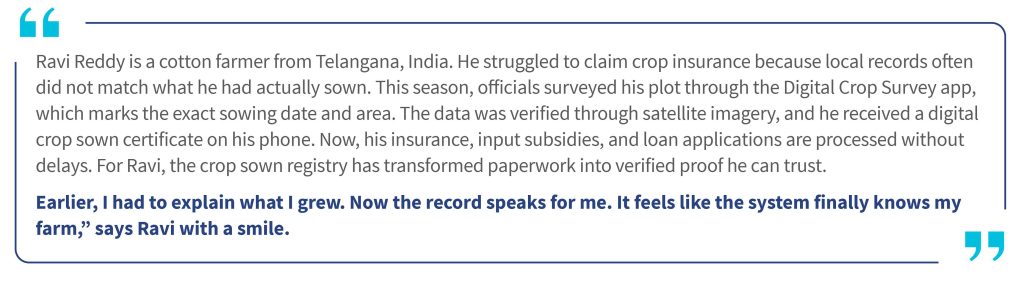

Overall, the DCS app provides farmers with digitally verified crop sown certificates, which serve as proof to avail services, such as credit, insurance, etc. These certificates also allow farmers to sell their harvest in advance at competitive procurement rates. Furthermore, the crop sown registry enables governments to estimate the market supply of various crops. This data supports decisions related to export and import as well as the allocation of food grain for industrial purposes, such as ethanol production. From a broader perspective, the system creates a win-win situation.

Over time, decisions that previously relied on estimates will be based on verified data. The crop sown registry will become a single source of truth for what India grows each season. Data consolidation and stakeholder alignment across the country pose significant challenges. Yet, the benefits of clear crop records justify the effort.

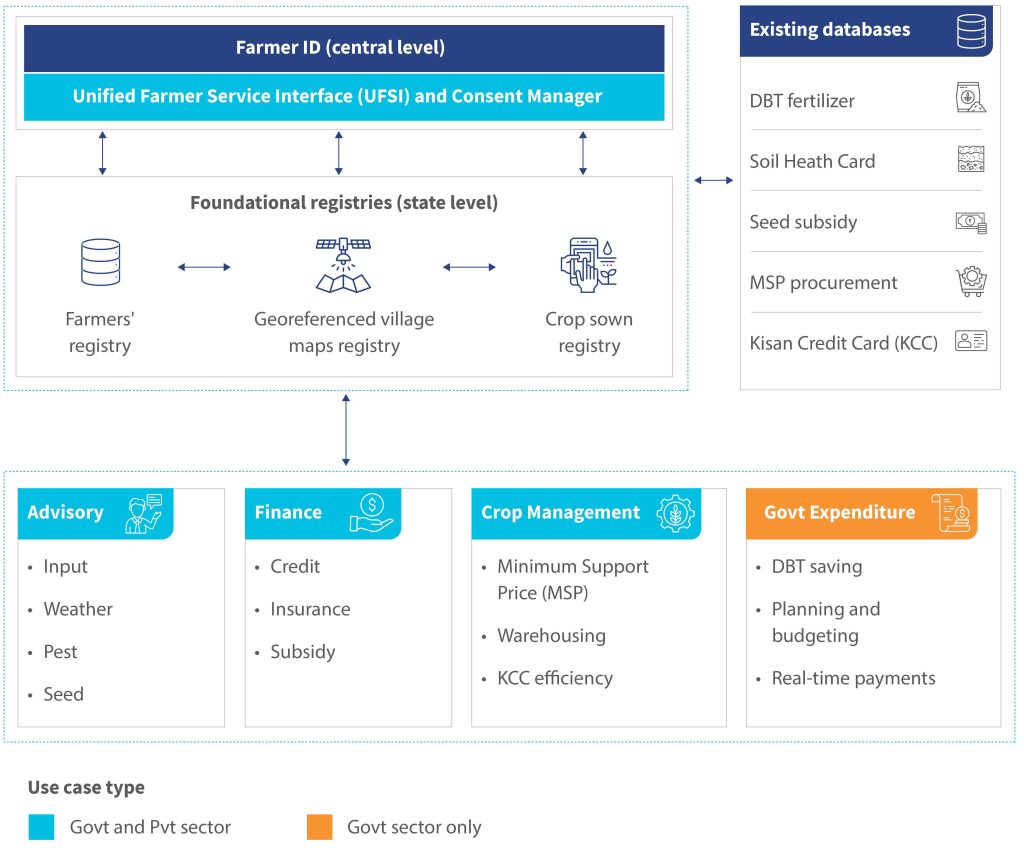

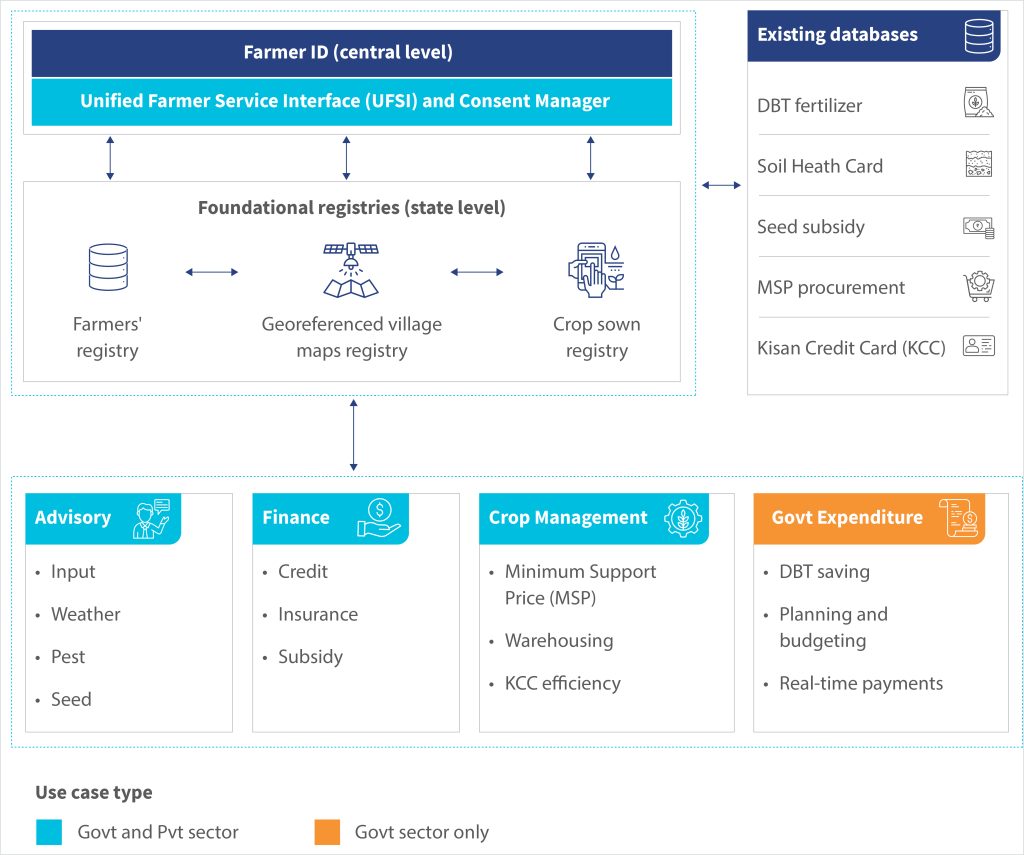

Together, the three foundational registries form the core of AgriStack. These registries interconnect to create a unified, reliable view of farmers, their land, and what they grow. When combined, they enable better planning, timely advisories, efficient delivery of benefits, and more transparent agricultural programs. The illustration below shows how these registries connect with existing databases and support a range of use cases across advisory, finance, crop management, and government expenditure.

Building blocks of AgriStack – Farm (Geo-referenced village maps) registry

As discussed in the previous blog, the state farmer registry will help identify all the farmers and the agricultural land parcels they own. Textual data on landownership is fetched digitally from the revenue records. This blog addresses the second question: Where are these agricultural land parcels located? The blog further explores the creation of a geo-referenced village map registry in India, and highlights the need to identify land locations and boundaries accurately.

Land has always been central to governance and taxation in India. The Mughals introduced early reforms, while the British later formalized systems, such as Zamindari, detailed land surveys, and revenue maps. At independence, India inherited these structures along with a reliance on manual records maintained by local revenue officials. Although these practices laid the foundation for land ownership and taxation, they also left behind fragmented and inconsistent records that continue to impact land management today.

After India’s independence, state revenue departments manually maintained land titles through local revenue officers called Patwaris. These revenue officers were responsible for managing all land rights tasks at the village level. They regularly updated the revenue records and cadastral maps after every change or “mutation”. Despite the manual maintenance of these records, the digitization of maps and records began only with the launch of the National Land Records Modernization Programme (NILRMP) in 2008.

Through the years, the Government of India has undertaken multiple initiatives to address the challenges in land records. These initiatives include Strengthening of Revenue Administration and Updating Land Records (SRA and ULR) in 1987-88, Computerization of Land Records (CLR) in 1988-89, and the National Land Record Modernization Program (NLRMP) in 2008. The most recent is the Digital India Land Records Modernization Programme (DILRMP), under which every land parcel is assigned a unique land parcel identification number (ULPIN).

The creation of a farm (geo-referenced village map) registry is essential to spatially identify and verify each land parcel boundary with geographic coordinates. This registry also supports digital crop surveys, precision advisory services, and evidence-based planning and research. For instance, in a digital crop survey, accuracy depends on the link between every land parcel in a village and its precise location on the map.This link ensures that surveyors record crop details for each plot through direct visits, rather than complete the entire survey from a single location that may even lie outside the village.

A geo-referenced village map registry enhances agricultural planning and service delivery when it links precise land boundaries with farmer and crop data. The combination of cadastral information with satellite imagery and ground truthing through GPS or drone-based surveys creates regularly updated, high-resolution spatial layers. This connection makes advisories more relevant, manages resources more efficiently, and delivers benefits to the right farmers. Key advantages include:

- Improved agricultural advisories and farm management: Integration of geo-referenced maps with geographic information system (GIS), crop registry, and weather data enables real-time, location-specific agricultural advisories. This helps farmers increase yields and resilience and supports crop monitoring, early disease detection, and resource optimization.

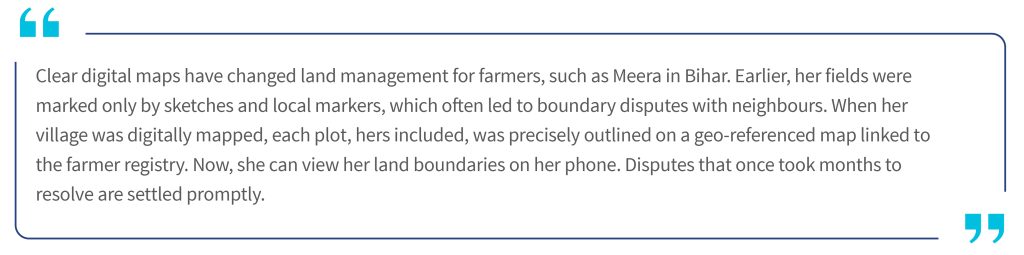

- Reliable land ownership information and effective land management: When digital maps are linked to the farmer registry, every land mutation or subdivision can be reflected spatially in near real time. This improves targeting, reduces disputes, and enhances transparency in land administration and the delivery of benefits.

- Data-driven policy choices and market linkages: Geo-referenced maps and integrated land–crop data support better agricultural policies, crop diversification, and precision resource planning. They also strengthen market linkages that help farmers access nearby markets, track real-time prices, and reduce dependence on intermediaries, which ultimately improves profitability.

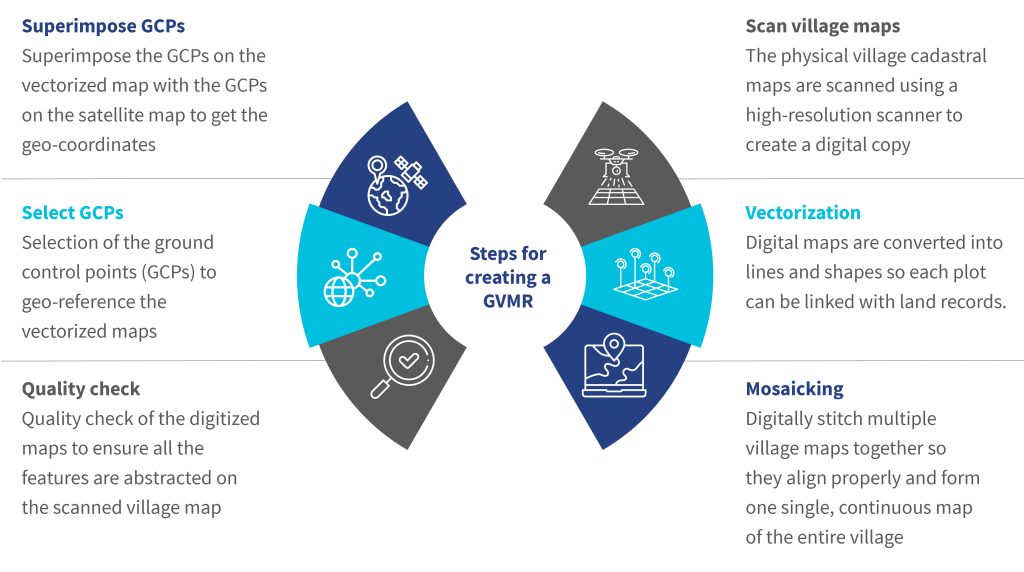

Creation of such a registry requires a series of technical and administrative steps. The ideal method is to capture fresh ground control points and physically map every individual land parcel that uses differential GPS or drone imagery. However, this is not always feasible due to costs, geographic terrain, data maturity constraints, and limited technical capacity. In such cases, states digitize the present cadastral maps and georeference them through satellite imagery. The process to digitize and georeference a village cadastral map can be broadly divided into six key steps, as outlined below:

Despite substantial government efforts, gaps persist in efforts to achieve complete digitization, integrate cadastral maps with ownership records, and update real-time geo-referenced data. It is crucial to bridge the following gaps to enhance data accuracy, interoperability, and service delivery to farmers:

- Inaccurate physical maps: Many physical land records are old and not regularly updated. The government often fails to accurately reflect the actual situation on the ground due to delays in map revisions.

- Errors in manual maintenance of maps: During manual updates of land records and maps, human errors can occur. These errors result in incorrect information being displayed on the maps about the land parcel. For example, during mutation, manual updates to maps can result in errors, such as misplaced plot boundaries or incorrectly entered survey numbers.

- Inconsistent land records: There are mismatches between the revenue records, field maps, and actual possession. These mismatches and land ownership disputes complicate land parcel ownership definition and the finalization of the digital village maps.

- Errors in scanning and vectorization: Old paper maps may be damaged, faded, or poorly aligned, which can introduce distortions during the scanning process and compromise the precision of boundary markings. Additionally, low-resolution scans produce blurry lines and illegible text, which makes precise geographic information difficult to extract during the vectorization process.

- Missing reference points in cadastral maps: Physical cadastral maps are difficult to match with actual locations since many rely on reference points. These include roads, trees, or landmarks that may have changed or vanished over time.

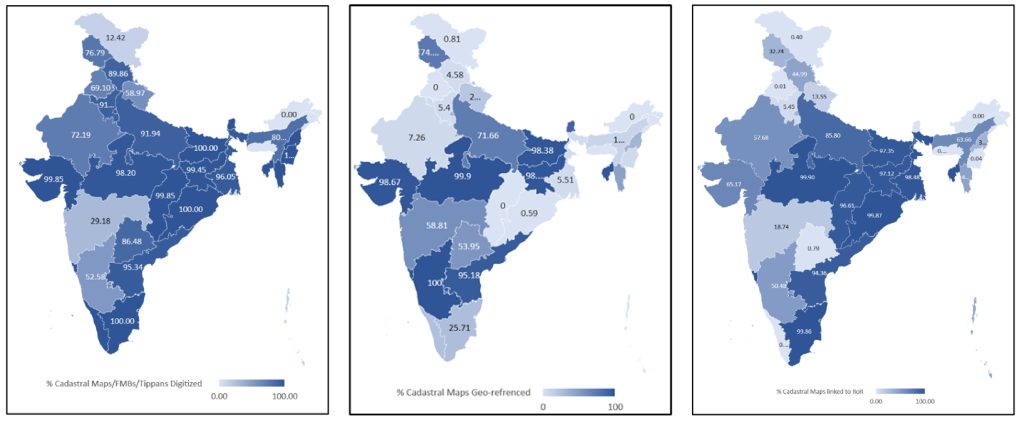

States across India have focused on efforts to digitize and geo-reference village cadastral maps through consistent mapping standards to address these challenges. This ensures spatial accuracy and interoperability across platforms. Some states have obtained high-resolution Cartosat-2 satellite images, while others have procured WorldView-2 satellite images for georeferencing.

Several states have also used drone-based mapping to capture fine-scale ground details where satellite imagery is insufficient. At the same time, a few states also conduct a special survey and settlement process to accurately depict on-ground situations and geo-reference plots. As of now, more than a dozen states have completed the digitization of all village cadastral maps and are at various stages of geo-referencing.

The integration of digitized maps with the farmer registry will provide a comprehensive profile of a farmer’s land, as the ownership data and the geo-referenced boundaries of the land parcel will be mapped to it. As part of these initiatives, Indian states have started to digitize and geo-reference village cadastral maps.

Once these digitized maps are integrated with the state farmer registry, each farmer’s landholding will have a unified spatial-textual identity. This identity combines ownership data from the revenue records with the exact digital boundaries captured through the cadastral maps. This unified record will enable instant verification of land ownership, reduce duplication, and support spatial analysis for planning and governance. Accurate, digital land maps are essential to improve farmer-focused services, such as region-specific crop insurance, customized weather updates, and location-based crop advisories.

The georeferenced village maps registry along with farmer registry and crop sown registries, forms the foundation of AgriStack. Together, these foundational registries integrate spatial, ownership, and crop data to create a unified view of Indian agriculture. Once combined, these registries will support a wide range of use cases across advisory, finance, crop management, and government expenditure, which benefits public and private sector stakeholders.

The illustration below shows how the three foundational registries interact within the AgriStack ecosystem to drive this transformation.

In the next blog of this series, we will discuss the crop sown registry in more detail.

Indian banks can unlock USD 688 bn opportunity through gender-intelligent banking: Report

New Delhi [India], November 21 (ANI): Indian banks could tap into a USD 688 billion untapped financial opportunity by adopting gender-intelligent design practices, according to a new report by MicroSave Consulting (MSC) and the National Institute of Bank Management (NIBM).

The publication comes at a critical juncture for India’s economy, as the continued underrepresentation of women across the financial ecosystem is estimated to cost the country USD 688 billion, impacting its ambition to become a USD 5 trillion economy.

While India has made strides in expanding access to financial services, active usage among women remains low, leaving one of the country’s largest untapped market segments

“Over the years, multiple actors have tried to mainstream gender into banking, but the results have been, at best, patchy. Gender-intelligent banking offers a systematic, operational approach to integrate gender within financial institutions; across business strategy, products and services, operations, and policy and governance,” said Akhand Jyoti Tiwari, Senior Partner, MSC.

“If tapped right, gender-intelligent banking alone can contribute 10 per cent of India’s USD 5 trillion economy goal,” said Dr Partha Ray, NIBM Director.

With female labour force participation rising sharply from 23.3 per cent to 41.7 per cent over the past six years, the report says there is an immediate business opportunity for banks and financial institutions. The whitepaper identifies four key areas of opportunity.

In deposits, women hold 1 billion bank accounts, yet nearly 497 million remain inactive, and activating these accounts could generate an incremental USD 253 billion in deposits, providing a critical boost amid rising credit growth.

In credit, women hold only 23 per cent of total outstanding retail credit (USD 212 billion compared to men’s USD 692 billion). With 110 million loan accounts unmet, this represents a USD 193.3 billion lending opportunity, with the average loan size for women at USD 1,712, compared to men at USD 2,825.

In investments, only 1.8 per cent of Indian women actively invest, leaving potential retail AUM growth from USD 235 billion to USD 477 billion, unlocking USD 242.3 billion.

In pensions, women account for 45 per cent of Atal Pension Yojana subscribers but accumulate USD 46,000-85,000 less than men due to career breaks and lower contributions, the report added. (ANI)

This was first published on ANI on Fri, Nov 21, 2025

Gender-intelligent banking: Branch counters to boardrooms

Women’s account ownership in India has grown exponentially through initiatives, such as the PMJDY. Yet, they remain significantly underserved in terms of usage, value of engagement, and access to higher-order financial services. Financial institutions must therefore recognize women as a diverse and strategically important customer segment with distinct financial behaviors, and not just as a social mandate.

This white paper, developed by MSC in collaboration with the National Institute of Bank Management (NIBM), presents a comprehensive and commercially grounded perspective on gender-intelligent banking. It offers evidence-driven insights to help institutions unleash long-term growth and strengthen business performance through a more informed and nuanced understanding of women customers.

Quantitative report – Impact on microentrepreneurs participating in digital platforms

Our new report is based on surveys with 400 microentrepreneurs, including both platformed digital users and unplatformed traditional businesses in urban and rural areas. The analysis reveals sharp contrasts in credit behavior, income patterns, and digital engagement. Gender and location strongly influence borrowing decisions, use of technology, and earnings. Yet, some findings are unexpected: Digital access does not always boost income, while women are often more independent in their use of technology. These patterns offer intriguing clues, which we explore in more detail in the full report.