Give us Some Credit! Meet the Digital Borrowers in Kenya

by Zeituna Mustafa, Mercy Wachira and William Nanjero

by Zeituna Mustafa, Mercy Wachira and William Nanjero Aug 22, 2017

Aug 22, 2017 6 min

6 min

In this blog, we analyse how Kenyans use digital credit and suggest ways to adapt existing products to better serve these customers.

It is 3 am in Nairobi. The city, known for its vibrant nightlife, is wide awake. Entertainment spots in the bustling capital of Kenya overflow as the night goes on. The streets are a sea of activity, filled with pleasure-seekers. Interestingly, it is between 3 am and 5 am that a third of all the digital loans from providers are taken. Could this be just a coincidence?

MicroSave conducted a qualitative study in Nairobi and Meru to understand the perceptions and motivations of low-income Kenyans to use digital credit. Using our customer-centric Market Insights for Innovation and Design (MI4ID) approach, we identified three profiles of digital borrowers: Repayer (Muthoni), Juggler (Makena) and Defaulter (Nyachae). In this blog, we analyse their use of digital credit and suggest ways to adapt existing products to better serve these customers.

Muthoni, 35, is a trader at Gikomba market. She buys fresh vegetables from Wakulima market at 3 am. She finances this purchase through digital credit. She has a choice pool of seventeen providers, and no longer uses informal lenders, who would charge her 10% interest per day. Her credit limit is $200, achieved through on-time repayment and disciplined saving.

Muthoni, 35, is a trader at Gikomba market. She buys fresh vegetables from Wakulima market at 3 am. She finances this purchase through digital credit. She has a choice pool of seventeen providers, and no longer uses informal lenders, who would charge her 10% interest per day. Her credit limit is $200, achieved through on-time repayment and disciplined saving.

Muthoni is a “Repayer”. Repayers are the premium customers for digital credit providers. They rarely default and can take multiple loans in a month. To reward this customer segment, providers could enable access to shorter or longer term loans, multiple/concurrent loans and increase credit limits. As is the case with Branch, other providers could also implement loyalty programmes that reduce interest rates and facilitation fees based on the size of loans taken, as well as on-time repayment. This would create ‘stickiness’ and reduce customer churn, as they tend to graduate to products with cheaper variable costs.

Makena, 37, runs a grocery shop in Igoji town. She is married and has four children. At any given month, she services over three digital loans in addition to traditional loans. Currently, she uses M-Shwari for emergencies and to boost her business, KCB M-Pesa for ease of consumption and Equitel to pay school fees. Occasionally, she uses Airtel Kopa Cash for sports-betting. She also has an $8,000 land loan from Cicido SACCO and another one from Equity Bank, which was used to restock her shop after it was looted. She usually repays late, but right before being negatively listed to ensure she can borrow again. ‘I prioritise [repaying] the Sacco loan as opposed to digital loans due to the huge penalties on default imposed by the Sacco. In some cases, they take your personal assets.’

Makena, 37, runs a grocery shop in Igoji town. She is married and has four children. At any given month, she services over three digital loans in addition to traditional loans. Currently, she uses M-Shwari for emergencies and to boost her business, KCB M-Pesa for ease of consumption and Equitel to pay school fees. Occasionally, she uses Airtel Kopa Cash for sports-betting. She also has an $8,000 land loan from Cicido SACCO and another one from Equity Bank, which was used to restock her shop after it was looted. She usually repays late, but right before being negatively listed to ensure she can borrow again. ‘I prioritise [repaying] the Sacco loan as opposed to digital loans due to the huge penalties on default imposed by the Sacco. In some cases, they take your personal assets.’

Makena belongs to the “Juggler” segment of digital borrowers, who face capital scarcity leading to the use and “animation” of different credit instruments to meet various financial needs. In this context, we recommend that providers cater to such customers by offering more flexible repayment periods and options to borrow in tandem and pay in instalments. The providers should also have clear incentives for on-time repayment (such as simultaneous access to multiple loans).

Nyachae, 26, is a savvy entrepreneur who runs an African fashion attire business in Nairobi. In 2015 he took a $5 M-Shwari loan to test the product but has not repaid it. He claims that reminder SMSs from the provider cannot scare him: “I delete the reminder messages. They don’t know me so they can’t find me”. Something about borrowing digitally feels less serious to the defaulter. Nyachae postponed the repayment until he was negatively listed with the Credit Reference Bureau (CRB). He would now have to pay $22 as clearance fees on top of his outstanding $5 loan to pass a credit check. Nyachae is currently servicing a $700 loan from the church SACCO. Recently, he managed to get a $20 loan from a provider despite being negatively listed.

Nyachae is a “Defaulter”. To better serve this segment, providers could include a personal dimension in the digital collection process. This could be done, for instance, through follow-up calls or through agent engagement in the case of larger loans. In addition, providers should better understand the defaulters’ intentions for borrowing as well as motivations and abilities for loan repayment. CRB regulations should accommodate the realities of digital credit, for example, by having different tiers of clearance fees that are commensurate with the loan amounts.

While interacting with Muthoni, Makena and Nyachae, we came upon a number of insights. These are enumerated below:

- Borrowers only had a limited understanding of the terms and conditions. This was because these were presented in legal jargon and accessing them through a weblink created real technological, cost-related, and psychological barriers. There is, therefore, a need for salient and simple terms and conditions presented before a customer accepts the loan (that is, through pop-up messages for STK, or inbuilt messages for mobile apps). It would also be ideal to separate the interest rate from the principal. This will limit confusion and enhance understanding of the repayment amount.

- There is clearly an element of gaming the system to influence loan limits. In this regard, providers can use interactive SMS to understand the context of customers’ loan uptake. Is it taken in an emergency? Is the loan availed as a trial without consideration for long-term implications? Or is the borrower trying to “game the system”? Engaging customers before they take the loan can reduce uninformed borrowing and delinquency. It can help avoid a situation like Nyachae’s unrepaid $5 loan.

- Reminders messages sent at different times of the day do not elicit repayment behaviour (Nyachae and Makena ignore messages sent in the morning). Providers should instead customise repayment reminder messages and incentives in terms of the customer segment and ensure that the reminders are goal based, so customers may see the value of timely repayment. Including a personalised touch, such as follow-up calls, can also drive repayment. This has been seen in the case of providers like KCB M-Pesa that uses a dedicated call centre to follow up with loan defaulters, Tala, which uses a collection agent, and Nimble Kenya, which also call to follow up with defaulters.

- Ultimately, to encourage timely repayment from customers like Makena and Nyachae, there is need to use behavioural levers to drive repayment. These could include the following:

- Priming ‘good borrower’ identities during the loan application stage. (‘Only prompt repayers take this loan, do you wish to proceed?’);

- Framing loan default as having serious consequences (‘You will not be able to borrow in future if negatively listed on the CRB’);

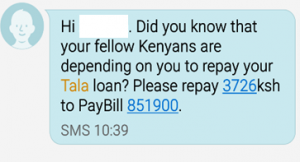

- Using social proof to elicit on-time repayment (see the adjoining Tala chat screen).

There is a clear demand for digital credit. A growing range of providers experimenting with approaches to respond to this demand bodes well for the future. However, to serve the wide range of borrowers better, providers should design products that leverage both rigorous data analyses as well as demand-side customer-centric research to understand the wide range of behaviours, contextual challenges and client experiences. Over time, they should incorporate learning within the product to educate customers on personal savings goals, and make these accessible to customers before and/or after disbursement.

Regulators also have an important role to play and should make it mandatory for all providers (including app-based lenders located outside the country) to use Credit Reference Bureaus to share data on digital borrowers. Regulators should set minimum standards for customer recourse channels and coordination by partners to address issues/complaints raised by customers and drive long-term usage and customer loyalty.

Digital credit is still a nascent industry with much scope for learning. Understanding the needs, aspirations, perceptions, and behaviour of customers should allow providers to design products and ‘lend smarter’, rather than depend on the risk premium-inflated interest rates to secure their business case.

Leave comments