Interoperability – A Regulatory Perspective

by William Nanjero, Jacqueline Jumah and Isaac Ondieki

by William Nanjero, Jacqueline Jumah and Isaac Ondieki Sep 4, 2017

Sep 4, 2017 5 min

5 min

The blog discusses the role, benefits and how countries around the world are adopting interoperability in digital finance.

Basis great inputs and discussions from Amrik Heyer, FSD Kenya, Stephen Mwaura former Head of Payments, Central Bank of Kenya, Uma Shankar Paliwal, Former Executive Director, RBI, Dennis Njau, Head of Channels, Kenya Commercial Bank, Gang Chai, Payment Policy Manager, Central Bank of Nigeria and Johnah Nzioki from Eclectics.

In a recent workshop organised by MicroSave’s The Helix Institute, leading DFS industry players including providers, regulators, aggregators, and technology providers, came together to deliberate on innovative ways to address the key challenges facing agent networks. They divided into three groups to look at the key issues in the context of: 1. policy and regulation; 2. strategy and market evolution; 3. operations.

The policy and regulation group noted that:

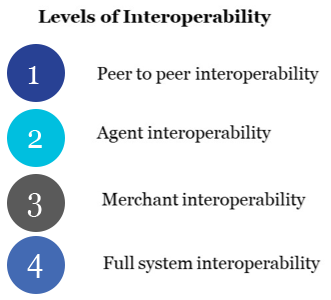

Countries around the world are at different stages of payment system evolution. There are different  levels of interoperability as defined by the Better Than Cash Alliance. From peer to peer interoperability, to agent interoperability, to merchant interoperability and full system interoperability. Peer to peer interoperability sees individual institutions connecting one on one through individual connections; agent interoperability, sees agents able to operate transactions between providers; merchant interoperability where merchants can accept payments form any provider; and full systems interoperability sees institutions, banks, mobile financial service operators or both connecting to a common platform or switch, thereby facilitating transactions.

levels of interoperability as defined by the Better Than Cash Alliance. From peer to peer interoperability, to agent interoperability, to merchant interoperability and full system interoperability. Peer to peer interoperability sees individual institutions connecting one on one through individual connections; agent interoperability, sees agents able to operate transactions between providers; merchant interoperability where merchants can accept payments form any provider; and full systems interoperability sees institutions, banks, mobile financial service operators or both connecting to a common platform or switch, thereby facilitating transactions.

Interoperability offers benefits for the wider ecosystem – these include: wider adoption; higher transaction volumes; and greater velocity of money in the ecosystem. From consumers’ perspective, interoperability means more convenient and efficient services. For regulators and policy makers this translates to reduction in expensive cash in circulation; expansion of the formal financial economy and a direct impact on advancing financial inclusion.

However, countries have different paths to interoperability, driven partly by the circumstances in their market and partly by regulatory philosophy. Some espouse competition on the basis of products and services provided by individual institutions, rather than on channels, which everyone needs to use. This view underpins the shared agent initiative in Uganda, for example. For others like the Better Than Cash Alliance, interoperability is a key aspect payment system evolution.

In the case of Rwanda a national policy on interoperability sought to: create a cash-lite society, encourage financial inclusion, and promote payment system efficiency. The goal for in interoperability was to: improve productive efficiency; increase the customer value proposition to use electronic payments; increase customer convenience; and increase efficiencies due to specialisation in payments. This policy dialogue preceded circulars mandating peer to peer interoperability and work on a national switch for real time micropayments.

Why the rush for interoperability? – especially when some regulators opine that digital financial services is in its infancy and there is a danger in being too prescriptive, whilst the industry is still learning. From a policy maker’s perspective, interoperability facilitates an efficient payment system, as it enables real time micro payments to be made and cleared between any account or any wallet. Subject to the application of Know Your Customer (KYC) requirements it facilitates visibility within financial transactions supporting national and international requirements for Anti Money Laundering (AML) and Combatting the Financing of Terrorism (CFT).

Practically, what difference can it make? In Kenya Safaricom provided widespread peer to peer interoperability with the M-PESA platform, thereby enabling transfers from bank accounts to wallets and in doing so, facilitating the widespread adoption of merchant payments. The Kenya Interbank Transaction Switch (KITS) operated by the Kenya Banker’s Association facilitates real time transfers of up to approximately $10,000, through participating bank accounts. In India through accounts linked to the digital national identity – the Aadhaar and the Unified Payments Interface (UPI) is providing access to financial services for millions through low cost agency operations operated by special purpose payment banks or small finance banks, besides traditional commercial banks. Interoperability combined with digitised information will enable Indians to shop for loans between multiple institutions.

Enabling interoperability is different from having a system which embraces interoperability. This is due to multiple challenges, one of which is pricing. For example, in Uganda it is possible to transfer funds between mobile money providers and to ‘cash out’ across networks. However, few chose to do this directly in part due to high cash-out fees on intra-network transactions.

There is a debate amongst policy makers and regulators on conceptual frameworks for interoperability – whether to use market- or state-based. In Kenya, the regulatory philosophy is for market based interoperability where the market defines the price and there can be multiple providers; hence the provision of services through KITS in addition to most players connecting directly to Safaricom’s M-PESA. In Nigeria, the government stepped in to create the Nigeria Interbank Switch (NIBSS), which it then mandated that institutions should connect to. This was a policy decision influenced by perceived inaction in the marketplace. In India, there are multiple solutions providing interoperability.

Price sensitivity is a factor in some markets. Market leaders often use pricing to stifle competition. Digital finance enables very low-cost transactions, but still in some markets pricing discourages wallet to bank and bank to wallet transactions. This makes it uneconomic, for example, to save small amounts to a bank account through a mobile provider’s wallet.

India shows elements of market and command philosophies; whilst there are several national payment mechanisms, the interchange fees on the switches are kept low to boost interoperability and market acceptance. Policy makers’ desire for a low-cost debit card, which any Indian could use at a fraction of the cost of EMV[1] compliant cards was a factor in the creation by the National Payments Corporation of India (NPCI), of the RuPay card.

From the perspective of financial institutions, market based mechanisms are often preferred especially by market leaders, who can use their market position to influence interchange fees. For a market leader, the commercials around interoperability are often key; they can be reluctant to share their network of agents for example with other institutions because: a) the interchange fee may not be sufficient to facilitate liquidity management and b) due to competitive positioning. Thus, for Kenya Commercial Bank, the fee structure of mVisa made it less attractive as a product for the bank.

A regulator, therefore, must contend with, and balance, policy imperatives for cheap and convenient access, with ensuring sufficient incentives for market based mechanisms to encourage the provision of the infrastructure on which interoperability relies. The challenge is to create an environment where different market players can play to their strengths and respond to the unique characteristics of the country they operate in, which can include widely disbursed populations such as in Tanzania or Zambia.

In the words of one regulator “Retail payments are dynamic – the regulator needs to provide space for this dynamism and for different actors to play a role, over time this will reduce costs”.

*Interoperability means a set of arrangements, procedures and standards that allow participants in different payment schemes to conduct and settle payments across systems while continuing to operate also in their own respective systems. Definition by CPSS

[1] EuroCard, MasterCard, Visa (EMV), a defacto standard in the payments industry

Leave comments