Over the past decade, Indonesia has made significant progress in the effort for financial inclusion. The 2025 national survey on financial literacy and inclusion (SNLIK), released on 2 May 2025 by the Financial Services Authority (OJK) and the Central Statistics Agency (BPS), revealed that national financial inclusion had reached 80.51%. However, only 66.46% of the population manages to use financial services effectively. This 14.05% gap indicates a fundamental challenge in the financial inclusion efforts. Additionally, access to financial services has also not kept pace with the increased literacy or the ability to use them meaningfully.

In 2023, MSC conducted the study “Women in the digital economy: Improving job access for informal women workers in the digital economy” in collaboration with the Ministry of Women’s Empowerment and Child Protection (KPPPA). The study revealed that 90% of informal women workers who use digital platforms had financial accounts. However, most lacked the knowledge to manage their finances effectively, safely, and efficiently.

This financial gap deepens the vulnerability of informal women workers in the economic system. Most of these women work over 40 hours a week in paid employment and an additional 20 hours per week in unpaid care work, which includes taking care of the household and children.

These are double burdens that have contributed to the persistent gender gap in labor force participation over the past decade. BPS data from 2024 reveals that the labor force participation rate (LFPR) in Indonesia for men is 84.66%, while for women, it is only 56.42%. This 28.24% gap shows that financial literacy is linked to gender issues and domestic roles.

Why is financial inclusion beyond having a bank account?

Financial inclusion is often defined as simply having a financial account. In practice, the essence of financial inclusion lies in how financial services can be effectively used to help individuals manage their finances, reduce risks, and support life goals.

MSC’s study highlights that increasing access to financial services will not be impactful unless adequate public awareness is provided to manage these financial tools. Therefore, financial literacy must be positioned as a core component in every financial inclusion initiative and program.

In the informal sector, where many women work, access to social protection, information, and financial education is often limited. This is why improving women’s financial literacy is not merely a choice; it has become necessary.

Strategic recommendations: from study to real action

MSC’s comprehensive framework on the financial services space, or the gender centrality framework, addresses women’s financial literacy challenges. It was designed to ensure that financial services are accessible, relevant, user-friendly, and sustainable for women. Such an approach places local context, women’s dual roles, and household decision-making dynamics at the heart of financial solution design.

The Small Firm Diaries research conducted by MSC in Indonesia concludes three strategic recommendations to elevate women’s financial literacy as a national priority:

Integrate financial literacy into every financial inclusion program, not as an add-on but as a foundational element.

Apply a gender-sensitive and local context-based approach that considers women’s socio-economic realities and the specific barriers they face.

Introduce sustained multi-stakeholder collaboration that includes public and private sectors, civil society organizations, and local communities.

At the 2025 Indonesia International Financial Inclusion Summit (IFIS), the government set a target of 91% financial inclusion by the end of 2025 and 98% by 2045. However, achieving this goal is insufficient if efforts are only focused on numbers. The accurate measure of success lies in whether every individual, including informal women workers, can understand, choose, and use financial services to meet their life needs.

Empowering women to use financial services is not just a metric—it is the foundation of a fair, inclusive, and sustainable financial system. As the digital economy expands, leaving women behind is not an option. It must be a shared responsibility.

This article was first published on the Kumparan platform on 5th June 2025.

Vulnerable people worldwide rely on social protection systems as vital lifelines. These systems include social assistance, insurance, and labor market reforms. They were traditionally built to address and manage chronic yet predictable risks, such as poverty and unemployment. Today’s world, however, presents more complex and unpredictable challenges—from climate hazards (e.g., shocks such as floods, cyclones, etc., and stresses- such as changing precipitation, rising temperatures, etc.) to other disasters, e.g., pandemics, armed conflicts, or financial crises. Such events endanger people’s lives and livelihoods while also deepening structural inequalities and persistent poverty.

As climate hazards and disasters become more frequent and severe, traditional social protection systems struggle to keep up. Adaptive Social Protection (ASP) has emerged as a response to this and intends to help vulnerable households build resilience. ASP examines and identifies strategies for ex-ante preparedness, ex-durante response, and ex-post recovery.

The need for a holistic ASP ecosystem

ASP is a comprehensive strategy that combines social protection, disaster risk reduction, and climate change adaptation. However, despite ongoing progress, some gaps remain:

Coverage and reach: Urban vulnerability remains underrepresented in the literature on ASP. The focus on rural communities leaves gaps in addressing the specific risks urban populations face, especially those residing in informal settlements.

Identification and access: In countries, the effective functioning of ASP is hampered by the lack of social registries or targeting issues due to outdated data, exclusion errors, and lack of interoperability. For example, the national social registry in the Philippines was not updated for four years during COVID-19, which made it unreliable for the rapid expansion of social protection programs.

Climate adaptation: Most countries lack climate-focused social protection and rely on emergency support. The ILO reports that more than 90% of people in the 20 most climate-vulnerable countries lack any form of social protection. For example, when severe floods hit Cambodia in 2022 and people were still coping with the effects of the COVID-19 pandemic, the government had to rapidly extend cash transfers to address both types of shocks—pandemics and floods. Further, coverage of anticipatory cash transfers worldwide is limited, as it covers only 13 million people, with an approximate allocation of USD 200 million.

Financial stability: For underdeveloped countries, where government spending is already constrained and borrowing from capital markets is very costly, budgetary reallocations for climate-induced shocks and stresses come at a cost. As highlighted by the ILO, little guidance is available on innovative financing mechanisms or successful examples of blended funding streams that developing countries can use to create such systems.

Considering these gaps, MSC follows an ecosystem-based approach to ASP that aims to assist governments in building robust, responsive, and inclusive social protection systems. This blog explores the rationale, methodology, and practical applications of MSC’s ecosystem approach to ASP. It draws from our experience across Asia and Africa and offers a roadmap for governments seeking resilience and equity in the face of new challenges.

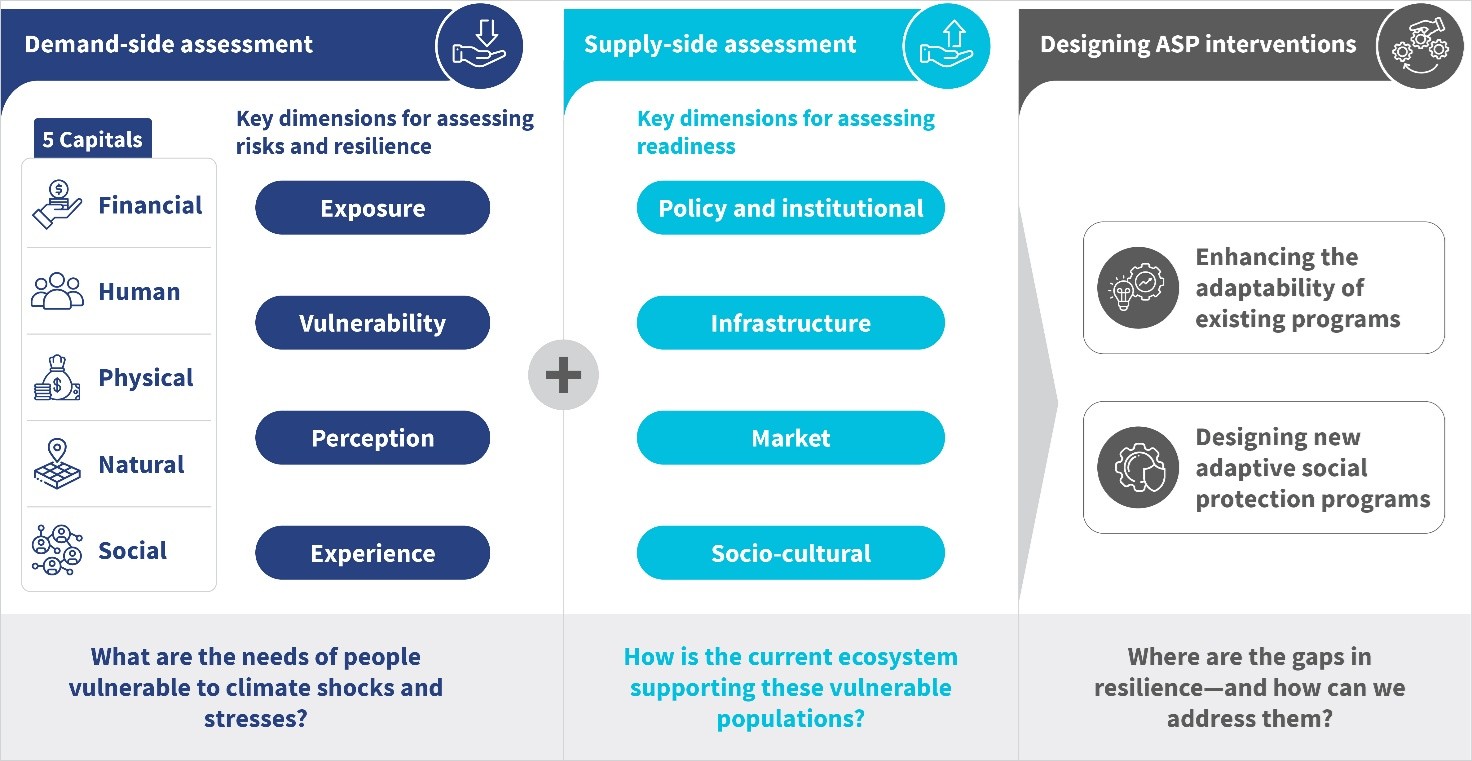

The approach stands out for its holistic, evidence-based methodology. It comprehensively evaluates demand and supply aspects to help address climate hazards and disasters. The objective is to enable individuals, households, and communities to anticipate, absorb, and recover from hazards and disasters.

Demand-side analysis

On the demand side, the approach evaluates the sustainability and overall well-being of individuals, households, and communities using the five capitals approach (human, social, natural, physical, and financial). Further, it systematically examines the following four key dimensions.

Exposure: Identifies the degree to which populations, infrastructure, and ecosystems are located in hazard-prone areas and the factors that hinder their ability to prepare, respond, and recover. It measures who or what is at risk and the extent of their exposure to potential shocks.

Vulnerability: Understands the factors that hinder an individual or community’s ability to prepare for, respond to, and recover from climate hazards and disasters.

Perception: Examines citizens’ perceptions of their susceptibility and preparedness and their understanding of the government’s efforts and capacity to respond to shocks, providing insights into factors like trust and awareness.

Experience: Reviews how vulnerable populations interact with social protection programs and government disaster response programs; it focuses on accessibility, adequacy, and timeliness of services received, and highlights successes and areas for improvement in service delivery

The demand-side analysis combines these four dimensions with the five capitals approach. It offers a complete picture of the capacity of individuals, households, and communities to prepare for, cope with, and adapt to hazards and disasters.

Supply-side analysis

A comprehensive supply-side analysis systematically maps and evaluates the policies and institutional structures, infrastructure, market mechanisms, and sociocultural factors. These factors underpin a country’s capacity to support vulnerable populations and ensure inclusive, adaptive, and resilient disaster management. These four pillars are essential to understand and strengthen a nation’s disaster resilience.

Policy and institutional readiness: This element assesses the strength and responsiveness of a country’s policies and institutions in disaster preparedness and response. It examines whether vulnerable groups are identified and protected by law and included in disaster plans and support measures. It also reviews digital public infrastructure within government systems to ensure the smooth flow of resources, information, and government-to-person (G2P) transactions during emergencies.

Infrastructure readiness: This element evaluates the resilience of a country’s infrastructure, including the digital infrastructure, to prepare for and respond to climate hazards and other disasters. Key areas include water, sanitation, and hygiene (WASH) facilities, transportation and logistics networks, financial services, and telecommunications systems, all critical for effective disaster management. Additionally, with the increasing threat of epidemics and pandemics, the resilience of healthcare infrastructure is crucial to operate effectively during crises.

Market readiness: This element looks at how market and economic systems support disaster resilience. Access to finance, agricultural productivity, and climate adaptability across agriculture and food systems are essential to ensure food security. It evaluates the capacity of industries to withstand climate hazards and other disasters to ensure resilience measures are integrated across sectors to support sustainable recovery. For example, India’s market and infrastructure readiness allowed the delivery of free food to ~800 million people during the COVID-19 pandemic.

Sociocultural readiness: the socio-cultural dynamics that influence a society’s resilience to disasters, focusing on inclusivity across race, caste, gender, and ability. It assesses how social diversity is acknowledged and supported in disaster planning, ensuring equitable protections and resources for all groups. This pillar also evaluates the trust between communities and the government and the availability of mental health and cultural support systems to aid in preparedness and recovery. Additionally, it highlights the value of indigenous knowledge, recognizing traditional practices and wisdom that can enhance disaster response and resilience strategies through locally-led adaptation.

The supply-side analysis enables governments to systematically identify gaps and bottlenecks. It pinpoints institutional, infrastructural, and market weaknesses that hinder effective disaster response. By addressing these bottlenecks, governments can strengthen the ecosystem and ensure that social protection systems are robust, inclusive, and responsive to emerging climate and disaster risks.

The design of suitable APS interventions

The demand- and supply-side analyses help us identify the gaps that affect vulnerable groups when they seek to cope with shocks and recover from them. Governments can address these gaps in one of these two ways:

They can adapt existing programs for climate-induced shocks and stresses by expanding cash or in-kind support temporarily during shocks. The governments can use horizontal (coverage expansion) or vertical (benefit increase) mechanisms. Programs can use early warnings, such as rainfall, flood forecasts, or heatwave alerts, which would allow the government to take early actions, such as food or cash disbursement, before a disaster hits. Programs can also add climate vulnerability criteria to existing eligibility rules while creating beneficiary registries.

They can design a new adaptive social protection program specifically designed to address climate-related risks, such as climate-linked cash transfers or adaptive public works that respond predictively to climate triggers. Programs can adjust benefits based on the severity and type of hazard, such as drought-indexed agricultural insurance, conditional cash transfers tied to livelihood diversification, or employment schemes focused on ecosystem restoration.

The path ahead

With this approach, we attempt to provide a flexible and forward-looking framework for governments and stakeholders to address the growing climate hazards and other disasters. This ensures that social protection programs are more inclusive and effective, and can evolve in response to emerging risks. Ultimately, the ASP approach empowers stakeholders to build adaptive, resilient, and equitable systems that protect the most vulnerable people, support their sustainable recovery, and nurture long-term resilience in an increasingly uncertain world.

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

In this podcast, Albert Bundi and Emma Odera from MSC discuss how to expand access to formal finance for young farmers in Kenya. Their conversation highlights young agripreneurs' real struggles and the innovative solutions that can reshape the future of youth agrifinance in Kenya.

MSC’s Community Toolkit for Locally-Led Adaptation offers stakeholders a structured, participatory process to assess climate risks and cocreate adaptation plans with local communities. It combines local knowledge with scientific data to map hazards, evaluate vulnerability, identify and prioritize adaptation options, and develop actionable, costed plans. We have designed the toolkit for local governments, civil society, and financial institutions. It builds grassroots ownership, strengthens institutions, and supports inclusive, climate-resilient development at the community level.

MSC’s IFSP adaptation toolkit equips inclusive financial service providers so they can assess climate risks within their MSME portfolios and design tailored, climate-responsive financial products. It also empowers MSMEs to use participatory tools and supply chain mapping to identify exposure and vulnerability and develop adaptation strategies. The toolkit enhances portfolio risk management, supports product innovation, and enables financial service providers to help drive MSME adaptation and long-term sustainability. Through the toolkit, MSMEs can also cocreate solutions to build their resilience.

A complex web of issues hinders women’s access to credit in Bangladesh. Among the most significant hurdles women entrepreneurs encounter are bureaucratic red tape and complex documentation requirements. Collateral requirements by formal institutions are another significant barrier. In a society where women rarely own assets, such as land or property due to gendered inheritance practices, these prerequisites further marginalize women in the credit system. Additionally, lengthy and bureaucratic loan procedures deter women, particularly those with limited literacy or exposure to formal banking systems. As a result, women entrepreneurs are forced to seek informal credit, despite the risks and higher interest rates.

Women’s barriers to credit access are not limited to structural challenges. They are also rooted in sociocultural norms. Patriarchal traditions often limit women’s mobility, decision-making power, and financial independence. This leaves them reliant on male family members for financial transactions. Even when women legally own businesses, they frequently require male co-signers for loans, which further perpetuates their dependency. Furthermore, gender bias within financial institutions paints women entrepreneurs as high-risk borrowers, which discourages them from designing tailored financial products for these women.

Policy implementation gaps also hinder efforts to improve women’s access to credit. For example, while the Bangladesh Bank mandatorily allocates 15% of credit portfolios to women entrepreneurs, weak enforcement has rendered it largely ineffective. Similarly, credit guarantee programs designed to facilitate collateral-free loans remain underutilized due to their poor implementation and low awareness among beneficiaries.

Although Bangladesh’s financial landscape is riddled with these problems, they are not insurmountable. Innovations in gender-intelligent banking have emerged as a potential way to break down these barriers. These include financial products and services designed specifically to meet women entrepreneurs’ needs. For example, Mutual Trust Bank (MTB) provides a small-ticket savings product combined with a secured overdraft facility so that women can access short-term, low-cost credit based on their savings history. This approach encourages consistent saving habits and reduces reliance on collateral.

Another key development is the digitization of financial services. Bank Asia’s digital loan application system reduced the need for physical branch visits and simplified documentation requirements. This initiative minimizes opportunity costs and makes credit more accessible, particularly for women in remote areas.

Gender-disaggregated data can also play a critical role to make financial products and services more inclusive. Banks can use the customers’ data to create gender-intelligent strategies to better understand and address women entrepreneurs’ needs. Such strategies can help create more inclusive financial products, services, and delivery channels that can ultimately promote their financial independence and nurture sustainable business growth.

Gender-intelligent banking is not about offering more products but rather about transforming the financial ecosystem from within to be more inclusive. An increase in women’s representation in leadership roles can play a critical role to shape policies better aligned with their needs.

The problem of women’s unequal access to credit is not unique to Bangladesh. As per the International Finance Corporation (IFC), globally, women-owned businesses face an enormous financing gap of about USD 1.5 trillion in the formal SME sector. This disparity highlights a substantial untapped market for banks to expand their SME loan portfolios by investing in women entrepreneurs. The global context makes the condition in Bangladesh even more significant. Bangladesh can witness tremendous economic growth through gender-intelligent banking practices, tailored financial products, digitized services, and capacity-building programs. At the same time, financial institutions can address sociocultural and institutional biases and policy gaps to work toward the global goal of gender equity and financial inclusion.

Bangladesh is at a pivotal moment where investments in gender-intelligent banking can contribute to sustainable economic growth, reduce gender disparities, and create a more inclusive financial ecosystem. As the country stands at the cusp of a major transformation, its present situation is a call for stakeholders across the globe to create an environment where women-led enterprises flourish and build a more prosperous and fairer society.

The Reserve Bank of India (RBI) has introduced new credit reporting guidelines aimed at improving the accuracy and timeliness of borrower information shared with credit bureaus. The Credit Information Reporting Directions, 2025, released this year, are designed to address issues in India’s credit assessment system. One of the key changes is the move to bi-monthly credit data updates. Lenders are now required to report borrower information twice a month—by the 7th and the 22nd. This reduces the lag in tracking repayments and helps curb overleveraging.

“Frequent updates reduce blind spots in credit data and ensure more informed lending,” said Shubha Bhanu, Lead, BFSI at MSC (MicroSave Consulting).

Previously, monthly reporting led to delays of up to 40 days, often leaving credit institutions with outdated borrower profiles. The revised timelines are expected to help lenders detect risks earlier and make better decisions.

Another major change is the standardisation of credit scores across all credit information companies (CICs). Scores will now follow a uniform range of 300 to 900, making it easier for both lenders and borrowers to interpret creditworthiness. The guidelines also streamline credit reports by linking borrower records to government-issued IDs such as PAN, passport, or voter ID. A single, consolidated report will now reflect all open and closed loans, defaults, legal actions, and coborrower or guarantor roles.

“These measures help eliminate fragmented data and provide a clearer picture of a borrower’s total liabilities,” Bhanu added.

Additionally, CICs can now share credit data with non-specified users—entities not traditionally allowed access—provided they secure borrower consent. This expansion in data sharing is balanced by strict privacy and security requirements. While the new norms may require significant tech and process upgrades for lenders, experts see them as a step toward a more transparent and responsible credit ecosystem.

This article was first published on CNBC TV 18 on 21st May 2025.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.