MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

In this podcast, Pauline Katunyo, a Housing Finance Expert at MSC, and Doreen Njau of MSC discuss Kenya's affordable housing crisis. This crisis has led to a deficit of more than 2 million units and primarily impacted the LMI households. They explore key barriers, such as high construction costs and limited financing options, and highlight innovative solutions, such as rent-to-own programs, incremental housing loans, and the role of microfinance institutions.

In our earlier blog, we looked at the digital revolution that has been brewing in India that continues to reshape the way microenterprises (MEs) function in today’s connected age. In this part, we dive deeper into the impact of digital platform adoption for MEs, variations within subtypes of MEs, and the way ahead for these small businesses.

The adoption of digital platforms has a nuanced but significant impact on MEs’ finances. Platformed MEs report a marginally higher income of INR 60,997 (USD 725) compared to INR 60,750 (USD 722) for unplatformed MEs. However, platformed MEs also face slightly higher expenses, with costs at INR 33,071 (USD 393) compared to INR 31,409 (USD 373) for their unplatformed counterparts. This increase is likely due to additional platform fees, logistics, marketing expenses, and increased inventory costs associated with digital platform use.

The impact of digital platform adoption also varies across different types of entrepreneurs. Male-owned MEs tend to incur higher business expenses, which could point to differences in the scale or type of businesses they operate. This suggests that platform adoption does not affect all MEs uniformly, as demographic factors like gender may play a role in shaping business outcomes. Despite higher expenses, frequent engagement with digital platforms tends to yield higher income, implying that MEs that invest more in the digital space can eventually realize greater financial gains. Thus, while digital platform use comes with added costs, the potential for long-term financial rewards remains strong for businesses that leverage these platforms effectively.

These observations underscore the importance of understanding the diverse ways digital platforms impact different groups of entrepreneurs. Gender-based differences in platform usage call for targeted interventions to ensure equitable access to the advantages of digital adoption. Furthermore, geographical differences emerge, as rural MEs tend to show better profit margins than urban businesses, while urban entrepreneurs express higher confidence in income stability. Together, these factors create a complex landscape of platform usage, requiring nuanced approaches to fully harness digital platforms’ potential for all entrepreneurs.

This financial impact extends beyond income and expenses, influencing how platformed and unplatformed MEs manage their financial operations. Our research shows that 79.7% of platformed and 81.2% of unplatformed MEs keep their personal and business finances separate. This demonstrates a fundamental level of financial discipline. However, the tools they use to track their operations vary significantly. Platformed MEs are more likely to use mobile money or bank statements and spreadsheets, while unplatformed MEs rely on memory and traditional bookkeeping methods. This suggests that digital platforms encourage the adoption of more modern, tech-driven management practices.

Interestingly, unplatformed MEs are more likely to reinvest their surplus funds into their business. This could indicate a difference in growth strategies or investment priorities between the two groups. Despite these differences, both platformed and unplatformed MEs embrace digital tools. A substantial 83.8% of unplatformed MEs use digital wallets for business transactions, which highlights the pervasive influence of digital financial services. As MEs adopt these new capabilities, they unlock opportunities to streamline operations, make data-informed decisions, and improve business outcomes. The digital transformation of ME business management is well underway, and many embrace these tools with the mindset that they will be well-positioned for success in the future.

Digital platforms contribute significantly to MEs’ resilience and growth potential. These platforms provide access to wider markets, streamline operations, and enhance financial flexibility, and, thus, empower MEs. Specifically, platformed MEs have access to a more diverse range of credit sources, which enhances their financial resilience. Our research shows that 39.5% of platformed MEs have borrowed money, with higher rates in urban areas. This diversification of credit options can help MEs weather economic storms and maintain financial stability.

Digital platforms are emerging as powerful tools to help MEs achieve several key business objectives:

Expanded customer reach;

Increased revenue streams;

Improved operational efficiency;

Enhanced access to financial resources, and;

Greater business resilience.

However, it is not just about access to these resources but also how effectively MEs use them. The strategic use of digital platforms and the financial opportunities they provide can significantly impact an ME’s ability to grow, innovate, and withstand market fluctuations.

Platformed MEs are more likely to borrow for business than their unplatformed counterparts. This suggests that digital platforms encourage MEs to invest in their businesses, which lays the foundation for future growth. Platformed MEs are also more willing to switch lenders for better terms than unplatformed MEs. This flexibility allows MEs to adapt to changing economic conditions and benefit from more favorable financing options when they arise.

These platforms provide access to a broader range of financial tools and business investments to empower MEs to build stronger. In a rapidly changing economic landscape, digital platforms’ role in supporting MEs’ resilience and growth cannot be overstated. As more entrepreneurs embrace these tools, we can expect a new generation of MEs to be better equipped to navigate challenges and seize opportunities in the digital age.

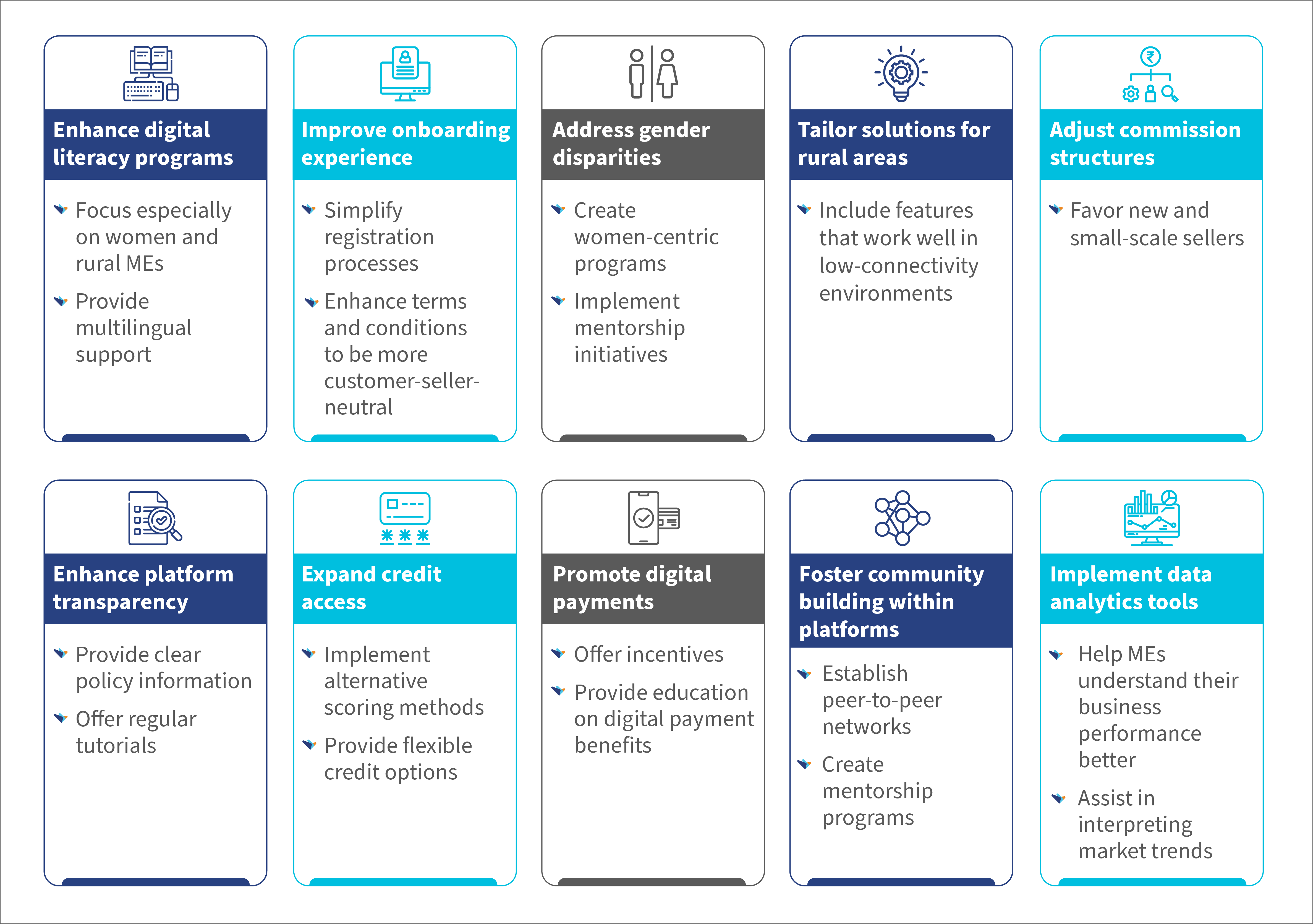

We propose several recommendations to empower microenterprises (MEs) further and increase the positive impact of digital platforms:

Digital platforms are indeed revolutionizing small businesses in India. They offer unprecedented opportunities for growth, resilience, and financial inclusion. However, the journey is far from complete. Significant disparities persist, particularly in terms of gender and rural-urban divides. Digital platforms’ potential to transform microentrepreneurs’ lives is immense. However, all stakeholders, including platform providers, policymakers, financial institutions, and support organizations, must make concerted efforts to realize this potential.

We can address the challenges and implement targeted support mechanisms to create a more inclusive digital ecosystem that empowers all microentrepreneurs, regardless of their location, gender, or digital proficiency. Microentrepreneurs can use digital platforms’ true potential if stakeholders employ mechanisms for MEs’ growth as the digital ecosystem grows.

*We have assumed a conversion rate of USD 1 = INR 84.08, as of October 2024

A digital revolution has been silently reshaping the landscape of microenterprises in India. Microentrepreneurs and India’s grassroots innovators have been delving into the digital arena with smartphones and a newfound enthusiasm for growth. This revolution does not just encompass a change in their manner of operation; instead, it involves a complete transformation of their business horizons.

Picture Meera, a small-town sari seller who showcases her vibrant collection to customers nationwide through digital platforms. Or think of Rajesh, whose local spice blend finds its way into kitchens hundreds of miles away. These are the faces of India’s digital microenterprise boom.

Digital platforms serve as catalysts for growth and resilience in an ever-changing economic landscape. They help increase revenues, provide a wider customer reach, and streamline operations. However, unfavorable policies for sellers and high commissions limit the broader adoption of these platforms. Hence, many microenterprises (MEs) stand on the sidelines, held back by various barriers. The divide between the digitally empowered and the unconnected is huge.

While this divide presents a challenge, it also brings forth an opportunity to bridge the digital gap and foster inclusive economic growth. We can achieve the following by addressing the barriers to platform adoption:

Empower more MEs with digital tools and market access

Stimulate local economies through an increase in the competitiveness of small businesses

Reduce economic disparities between urban and rural areas

Create a more diverse and resilient digital marketplace

Drive innovation in platform design and policies to better serve MEs’ needs

A wide array of digital platforms have been transforming the way MEs reach and serve their customers. These include e-commerce powerhouses, such as Amazon and Flipkart, and social media storefronts of Instagram, WhatsApp, and Facebook. These platforms can aid financial inclusion, enhance access to credit, and enable interaction with other MEs. This digital revolution means much more than convenience for MEs. It can unlock new possibilities, such as the ability to reach customers in far-flung cities and manage finances with a few taps on a smartphone.

Our study intended to understand MEs’ status on digital platforms, the consequences of their exclusion from digital platforms, and the type of support they needed to make digital platforms more accessible and effective. We surveyed 460 microentrepreneurs across India, with a careful balance to represent the diversity of the country’s microbusiness landscape. The sample included an almost equal gender distribution among platformed and unplatformed MEs, with about 73% in retail trade and 27% in social selling. We ensured equal representation from urban and rural or peri-urban areas, which allowed us to gain comprehensive insights into MEs’ varied experiences across different demographics and regions.

Our research paints a fascinating picture of the digital adoption landscape. Age and gender play surprising roles. The digital platform users tend to be younger, with a noticeable tilt toward male entrepreneurs. Education emerges as a vital factor—most digital platform adopters have at least a secondary education. Most platform users easily navigate the Internet, which showcases a growing digital savviness among India’s small business owners.

Microentrepreneurs are highly resourceful in finding ways to learn about these platforms. Most MEs rely on their research to understand digital platforms. The grapevine effect is real—friends and family often spark microentrepreneurs’ initial interest in digital platforms. However, a confidence gap persists—male entrepreneurs generally feel more self-assured when they navigate digital platforms independently. This tapestry of factors offers crucial insights for those who seek to bridge the digital divide and empower India’s microentrepreneurs in the digital age.

MEs’ journey on digital platforms is as diverse as the businesses themselves. Many MEs independently take their first digital steps and navigate the sign-up process. This self-reliant approach is seen across rural and urban areas, which shows the growing digital confidence among Indian entrepreneurs. Peer support plays a crucial role, especially for women entrepreneurs. In rural and peri-urban areas, friends and family often step in to help MEs get started on digital platforms. This highlights how social networks can help drive digital adoption.

Urban areas present a slightly different picture. Here, platform agents often play a key role to onboard MEs. They help people who are less comfortable with technology.

Retail sellers are drawn to platforms that offer competitive pricing and easy comparison tools. They seek ways to keep costs low and stay competitive in a crowded market. Social sellers, on the other hand, value user-friendly interfaces, powerful marketing tools, and responsive customer support. These features help them build their brand and maintain customer relationships effectively.

Despite the benefits, digital platforms are not without their challenges. High commission rates and unfavorable return policies are major pain points for many MEs. These issues, combined with complex platform interfaces and occasional technical glitches, can lead to frustration and, in some cases, compel MEs to leave the platform.

Yet digital platforms are evolving beyond marketplaces. They have emerged as crucial financial hubs for MEs. The adoption of digital wallets and payment apps has skyrocketed among platformed and unplatformed MEs. It has revolutionized how small businesses handle transactions. UPI, in particular, has gained significant traction among platformed MEs for business transactions. It offers previously unimaginable speed and convenience.

While digital payments are on the rise, cash still reigns supreme among unplatformed MEs. This dual reality highlights the ongoing digital transition in India’s microenterprise landscape. Credit access through digital platforms has been reshaping financial inclusion for MEs. Buy now, pay later (BNPL) programs have become a game-changer. They have allowed entrepreneurs to manage cash flow more effectively and invest in inventory without immediate capital. However, this financial revolution does not reach everyone equally. A stark gender divide exists in credit usage—male entrepreneurs more readily tap into these digital credit lines. This disparity raises important questions about financial access and literacy among women entrepreneurs in the digital age.

In the next part of this two-part blog series, we will look at the impact of digital platforms on MEs, the differences between MEs who are on platforms and those who have not adopted platforms, and ways to increase digital platform adoption for MEs. Read the next part here.

Microentrepreneurs are the lifeblood of India’s economy. They drive a significant portion of the nation’s growth from the ground up. These small-scale business owners often work in the informal sector and contribute immensely to employment and the GDP. However, despite their importance, many struggle with limited access to credit, market linkages, and digital tools that could help scale their businesses.

The impact of digital platforms has been profound for those who have embraced it. Yet, for most of those who remain unplatformed, the digital divide continues to widen and threatens to leave them further behind in an increasingly digital world.

These microentrepreneurs need a concerted effort to bring them into the digital fold. The effort must go beyond access to technology and create an ecosystem that supports their growth. This could be an ecosystem with simplified onboarding processes and training programs that build digital literacy. These efforts should also recognize the unique challenges women and rural entrepreneurs face, as they often face additional barriers to success.

Key insights from our research on Micro-entrepreneurs in India

MSC’s research with Busara has uncovered key insights into how digital platforms reshape the landscape for India’s micro-entrepreneurs. With more than 63 million MSMEs in India, understanding this shift is vital to drive inclusive growth.

The survey revealed a dynamic but challenging demographic profile. Most micro-entrepreneurs are between 25 and 45 years old, which indicates a young and driven workforce. However, a significant gender disparity exists with men’s dominance over the sector. Geographically, the split between urban and rural entrepreneurs is almost even, yet rural microentrepreneurs face more hurdles, especially in access to digital tools and infrastructure.

Awareness of digital platforms among microentrepreneurs is primarily spread through word-of-mouth, and many learn about them from peers or community networks. Despite this, the onboarding process remains complex. While some microentrepreneurs manage to register independently, a substantial number rely on peer support or agents. This highlights a critical area for digital platforms to simplify and streamline their processes.

Sustained usage of digital platforms is closely tied to digital literacy. Our findings also show that 38% of MEs who use these platforms report better business outcomes, such as increased income and expanded customer reach. However, those with lower digital skills often struggle to maintain active engagement, which limits their growth. This is especially true in rural areas, where digital literacy rates are lower and reliance on traditional methods remains strong.

The impact of digital platforms has been transformative. Many microenterprises have seen significant income boosts—some as much as 30%—with access to new markets and streamlined operations. However, this growth often comes with higher expenses, such as platform fees and logistics costs. Despite these added expenses, the overall business confidence among digital platform users has increased, with many microenterprises feeling more resilient and optimistic about the future.

Unlocking growth: How can India’s micro-entrepreneurs thrive in the digital economy?

Digital platforms are transforming industries. However, the road to success is not straightforward for many of India’s microentrepreneurs. Our latest research with Busara highlights the significant challenges they face on digital platforms, which include high platform fees, complex onboarding processes, and limited digital literacy. This is especially true for women and rural entrepreneurs who face unique struggles, such as smaller social networks and subsistence-driven priorities.

So, how can we help them?

Simplification is key. Many entrepreneurs are held back by complex digital onboarding systems. In such a case, streamlined processes and intuitive interfaces could make a world of difference for them. We have also seen the power of peer mentorship and targeted training in the field, which boost digital literacy and help entrepreneurs build confidence and stay engaged.

We must develop credit solutions that meet their needs and help them scale their businesses to level the playing field. More importantly, women-led networks and community-driven support can break down the barriers that hinder several women’s access to digital opportunities.

India’s digital economy is full of promise. However, that potential will only be realized when all microentrepreneurs have the support they need to thrive, regardless of gender or geography.

Empowering microentrepreneurs: Key takeaways and next steps

We conducted a survey with Busara to gain a deeper understanding of the unique challenges and opportunities microentrepreneurs face in India, especially as they adapt to the rapidly evolving digital landscape. This research is vital to identifying effective strategies to support these entrepreneurs.

The findings reveal a dual reality. Despite the immense potential of digital platforms, many microentrepreneurs still grapple with limited digital literacy and inadequate access to financial resources. The gender disparity and the rural-urban divide further exacerbate these challenges and hinder the ability of many entrepreneurs to fully benefit from digital tools. Despite these barriers, those micro-entrepreneurs who have successfully integrated digital platforms into their operations report marked improvements in income generation and market reach. However, the complexity and time-intensive nature of the onboarding process has emerged as significant pain points, which deter wider adoption.

The development and implementation of tailored programs that improve digital literacy are vital to addressing these issues and enhancing engagement with digital platforms. The onboarding process must also be simplified to make these platforms more accessible. Additionally, the expansion of financial access through customized and innovative credit solutions can empower more microentrepreneurs to harness the benefits of digital tools.

The future of India’s microentrepreneurs is filled with promise, with significant potential for growth and resilience. We can open new pathways for these entrepreneurs to succeed if we address the challenges highlighted in our research and enhance digital platform engagement. This will ensure they continue to be a vital force that drives the nation’s economic progress.

Lenders perceive women borrowers as riskier and costlier to serve, and many women themselves are not credit-ready

India has almost eliminated the gender gap in access to bank accounts with the Pradhan Mantri Jan Dhan Yojana (PMJDY). More women have access to bank accounts, and more women are saving in these accounts. Women’s accounts hold 20% of all deposits by amount. In the era of shrinking bank deposits, women savers are holding up the bankers. Per capita, savings by women in bank accounts are approximately 3% higher than men, with an average bank deposit of INR 42,503 by women[1]. Women have been good suppliers of savings to banks; however, they remain severely unserved and underserved when it comes to credit.

According to a 2020 study, women in India receive credit equivalent to only 27 percent of the deposits they contribute to the banking system, while men receive credit equal to 52 percent of their deposits.

IFC estimates an INR 1.37 trillion gap in the demand and supply of credit for women-led enterprises in India. Interestingly, this gender gap in credit persists despite women demonstrating lower credit risks across various loan categories. In 2022, 57% of women borrowers had a prime (credit score of nearly 700 and less risky) and above, compared to 51% of male borrowers, as per TU CIBIL.

If figures from CIBIL are any indication, only 65 million women are credit active in India as compared to 156 million men. This means financial providers serve barely 14% of 453 million credit-eligible women in India.

Limited to small value.

The curious case of system-wide credit allocation to women begins and ends with small ticket-size loans in India. Lending to women has become synonymous with microfinance lending under “weaker sections” and loans to individual women up to 1 lakh under PSL guidelines. The average ticket size of microfinance loans (with 98% female clientele) in 2023 stood at INR 43,200, per the Bharat Microfinance Report. As per RBI, which classifies loans under 2 lakhs as “small borrowal accounts,” women’s share of the total outstanding amount, even under this category, was only 35.5% compared to 58% for men. Women constitute 20% of India’s 63 million MSMEs; however, they constitute only 7% of outstanding credit to the MSMEs sector.

The poor supply of credit to women is due to multiple factors. Primary among them is biases that impact both the supply side (the lenders) and the demand side (the women borrowers). Lenders perceive women borrowers as riskier and costlier to serve, with limited data footprint, credit history, and less formal sector experience.

Many women borrowers (individual as well as women-led collectives) are not credit ready. This is because they lack the documents, guarantors, and collaterals required for accessing productive credit. They also lack the time and confidence to follow through the application process in many cases.

There is also a hidden segment that is credit-ready but credit-averse and decides not to borrow from formal lenders. This self-exclusion is due to various reasons, ranging from bad user experience, time-consuming processes, social norms that discourage debt from formal lenders, lack of support systems, fear of backlash on loan default, and lack of confidence in their ability to repay.

It is time that the sector invests in gender-intelligent banking and does not treat women as customer segments limited to priority sector lending, government schemes, and the microlending portfolio. Without access to adequate credit, women entrepreneurs struggle to tap into higher-value areas of even the sectors they dominate, and lenders find it difficult to graduate them beyond microloans. A vicious cycle that needs to be broken. Credit is an important tool to support women’s growing entrepreneurial aspirations across India. Research shows that closing that gap can add as much as US$6 trillion to global GDP. When offered with the right features, in the right context, and responsibly, it can help women and India realize their economic aspirations.

The Interim Budget announced on February 1 had a significant focus on growing the country’s economy. The Finance Minister highlighted her vision for growing the country’s economy at the recent Vibrant Gujarat Summit. She said “It is possible that we will be the third largest economy by 2027–28, and our GDP will cross USD 5 trillion by that time. By 2047, it is a conservative estimate that we will reach at least USD 30 trillion in terms of the economy.”

In pursuit of creating a $30 trillion economy, it is imperative to prioritize not only economic growth but also ensure that development is inclusive and sustainable. It is of utmost importance to create a world where people from all sections of society have access to high-quality, affordable, market-led financial, economic and social services in the digital age.

According to the UNDP Report titled “Making Our Future: New Directions for Human Development in Asia and the Pacific,” India has made significant progress in increasing per capita income from USD 442 to USD 2,389 from 2000 to 2022. However, poverty alleviation remains a major challenge.

Numerous individuals find themselves highly susceptible to changes in economic circumstances, often teetering on the brink of poverty, of which women, interstate migrants, and informal workers are at greater risk.

Here are some strategies and focus areas for inclusive and sustainable growth:

Focus on climate change and food security in India

As the world grapples with environmental issues, India must find sustainable solutions to mitigate the impact of climate change. It is of the utmost importance to create climate-resilient agri-food systems that not only tackle the problem of hunger but are also sustainable and aligned on the path to net zero.

Climate change will have adverse effects on not only crops but also on forestry, fisheries, and livestock. India has to formulate policies and take necessary action to ensure that agricultural technology innovations undergo testing and expansion, aiming to enhance productivity at reduced expenses.

Agri-Stack is one such initiative by the government that has the potential to revolutionize the agricultural sector in India forever. AgriStack will facilitate more convenient access to affordable credit, superior farm inputs, tailored and specific guidance, and enhanced access to markets, which will also foster more agri-tech innovations that will benefit smallholder farmers.

As India has committed to becoming net zero by 2070, several green initiatives were announced in the Interim Budget 2024. These initiatives include the phased mandatory blending of compressed biogas (CBG) with compressed natural gas (CNG) for transport and piped natural gas (PNG) for domestic purposes, the expansion of the electric vehicle ecosystem, and promoting climate-resilient activities for the Blue Economy.

Creating a more enabling ecosystem to nurture skills in India

The Finance Minister made a statement during the Budget 2024 that “Skill India Mission has trained 1.4 crore youth and upskilled and reskilled 54 lakh youth.”

As many as 13 million young people join the workforce every year in India. There is a critical need to create an enabling environment for harnessing and honing their managerial, technical, and entrepreneurial skills. This will not only help in fostering entrepreneurship but will also create a more talent-ready workforce to meet the growing global demands for products and services across the world.

Skill development is one of the cross-cutting sectors that has enormous potential for not only the youth of the country but also for the healthcare, MSME, manufacturing, and consumer-tech industries.

Capsule-based training programs using intuitive learning tools by leveraging the existing digital infrastructure can be a game changer.

Healthy urbanisation and formal sector employment in India

India finds itself poised at the threshold of a profound urbanization surge, due to which an emphasis has to be laid on the urban poor, vulnerable communities, and rural migrants.

As more people migrate to cities in search of better income and opportunities, we have to not only focus on biodiversity protection but also ensure that we foster more employment in the formal sector. India has effectively transitioned a significant portion of its workforce from the less productive agricultural sector; however, the majority of employment opportunities still predominantly exist within the informal economy.

According to findings from the National Sample Survey Organization (NSSO) and the Periodic Labor Force Survey (PLFS), spanning from 1999 to 2019, the data reveal that a substantial portion (16%) of the labour force that shifted away from agriculture found employment in the construction sector (11%).

India must have a long-term strategic vision that not only promotes sustainable infrastructure practices but also promotes gender equality to create more formal job opportunities and reduce reliance on the informal sector. Emphasis has to be on the manufacturing sector, with an emphasis on local production and expansion within India for more inclusive growth.

The Production-Linked Incentive Scheme and the Semicon India Programme are some of the initiatives that are contributing to the encouragement of global investments with a focus on MSMEs and small enterprises to drive economic growth.

Enhancing the overall delivery of healthcare services in India

One notable aspect of the budget is the emphasis placed by the government on preventing cervical cancer through vaccination and the introduction of the U-Win application designed to streamline and manage immunizations across the country.

The government has also taken a series of initiatives, like the Ayushmann Bharat Digital Mission, which aims to create a unified digital healthcare stack to promote digital health and improve healthcare outcomes.

However, there is an abject paucity of healthcare infrastructure; there are merely 1.4 beds per 1,000 people, 1 doctor per 1,445 people, and 1.7 nurses per 1,000 people.

There are issues in infrastructure which often cause difficulties in accessing healthcare services. Though there has been an increase in the total expenditure on health from ₹79,221 crores in 2023-24 to ₹90,171 crores in 2024-25, India has to make a long-term strategy to ensure that at least 6-7% of GDP is utilized in healthcare spending. Efforts have to be made to keep a tap on healthcare inflation.

The article was first published on the Economic Times website on 9th February 2024.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.