We can categorize agents in India into either of four models—traditional agents, new-age agents, payments bank agents, or Gramin Dak Sevaks. These agents face particular challenges across their entire lifecycle, from setting up to reaching sustenance. This deck takes you through the journey of agents across each of these models and gives a bird’s eye view of the factors, such as economics, risks faced, and use-cases that impact this journey. The deck also outlines lessons from various pilots that MSC has conducted with its partners to address the challenges across their lifecycle.

Blog

“How did the new pricing strategy increase the income for Eko agents?” – Lessons from a pilot with Eko India Financial Services

Eko, a FinTech platform with a large agent network, offers a subscription-based pricing model to its agents, which helps them earn commission in a tiered manner based on the volume and value of transactions at their outlets. Eko strives to offer value to its agents and thus plans to change the plans to meet the needs of its agents. With MSC’s support, Eko developed new plans and tweaked its incentive structure to suit agent-specific needs better.

This deck looks at the approach taken to develop new plans and assesses their feasibility and their impact on the earnings of different categories of agents.

Do young entrepreneurs need new skills in a rapidly evolving digital world?

COVID-19 has led to lockdowns and restrictions on social engagements, resulting in increased usage of digital technology and tools across the globe. Today, we cannot talk about the entrepreneurship ecosystem without first looking at the challenges entrepreneurs encounter due to these restrictions.

Digital skills will be essential for 50-55% of jobs in Kenya, 35-45% in Cote d’Ivoire, Nigeria, and Rwanda, and 20-25% in Mozambique by 2030. Foundation digital skills will garner about 70% of the demand, while non-ICT, intermediate-level digital skills will account for 23% of the demand.

Importance of digital skills in youth entrepreneurship

Youth entrepreneurs are vital to a country’s social and economic development. According to the African Development Bank, 10-12 million youth enter the workforce each year, but only 3 million secure wage-earning jobs. As a result, fostering entrepreneurship among young people is essential.

Kutzhanova et al. (2009) examined four main dimensions of skill for entrepreneurs:

- Technical skills needed to create the business’s product or service;

- Managerial skills essential to the day-to-day management and administration of an enterprise;

- Entrepreneurial skills to recognize economic opportunities and act effectively on them;

- Personal maturity skills include self-awareness, accountability, emotional skills, and creative skills.

Since the onset of COVID-19, the tone of entrepreneurship has changed. As technology expands to become an integral part of our everyday lives, young entrepreneurs need to build their digital skills.

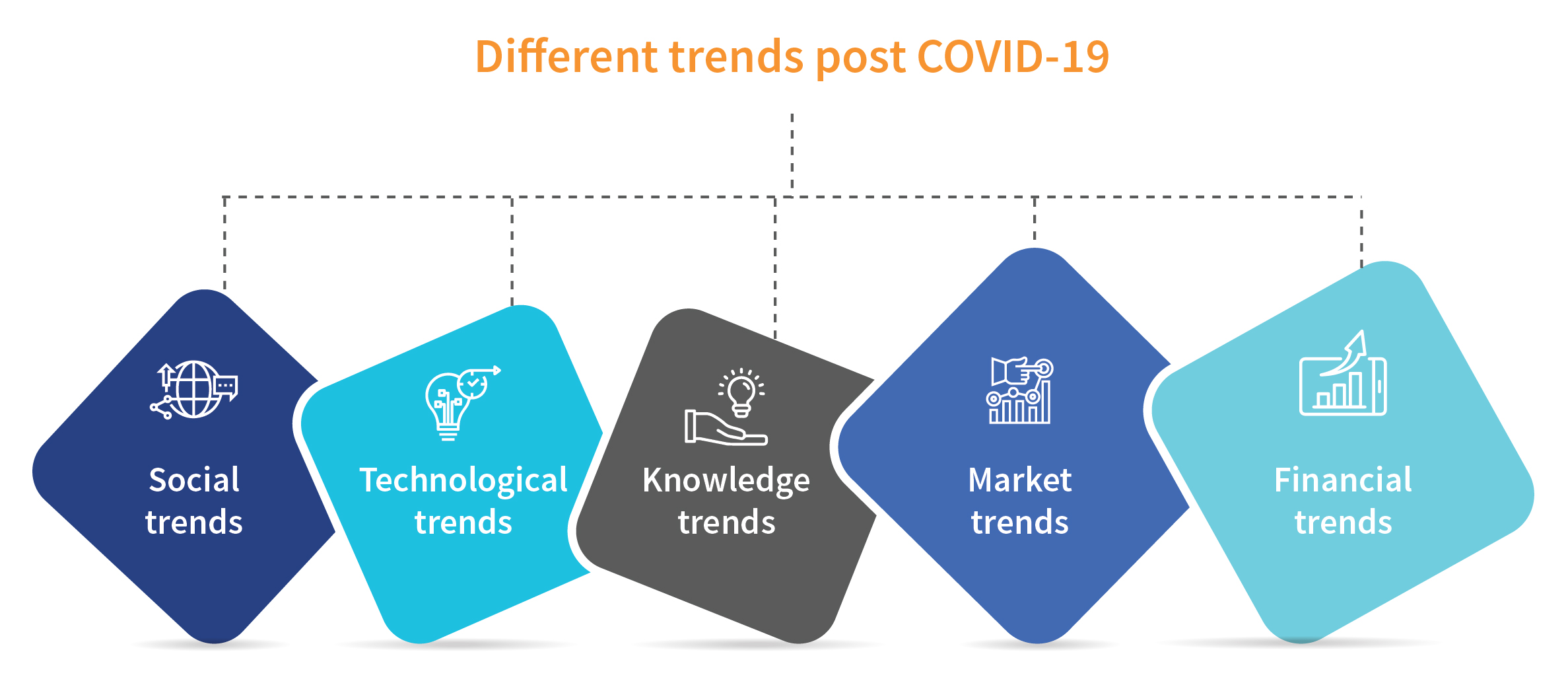

After the outbreak of COVID-19, we have witnessed different trends:

Figure 1 showing different trends observed after COVID-19 outbreak

- Social trends: Post COVID-19, the way people interact in society changed. DataReportal highlights that 4.7 billion people worldwide now use the internet, while 4.1 billion people have social media accounts. The user bases registered a growth of 7.4% and 12.3%, respectively, in 10 months from 2019 (as of October, 2020).

- Technological trends: Dependence on technology has increased, and COVID-19 has altered how we live and work. These changes have led to an explosion of new technologies and innovation, forcing businesses to adapt or disappear rapidly.

- Knowledge trends: Online delivery is often the preferred channel for education and training due to lockdowns.

- Market trends: E-commerce has revolutionized the way customers interact in the market. Some countries have achieved 7% growth in this sector, where the average growth rate is usually around 1%.

- Financial trends: A higher uptake of digital financial services (DFS) has eased access to financial products. A World Bank policy report finds that at least 58 developing countries have used digital payments for COVID-19 relief.

With these changing trends, young entrepreneurs must learn new skills to remain relevant.

Digital skills and their applications

According to UNESCO, digital skills are abilities to use digital devices, communication applications, and networks to access and manage information. This means knowing digital skills and the ability to apply those skills in the digital world. Hence, young entrepreneurs need to learn digital skills and integrate them into their enterprise.

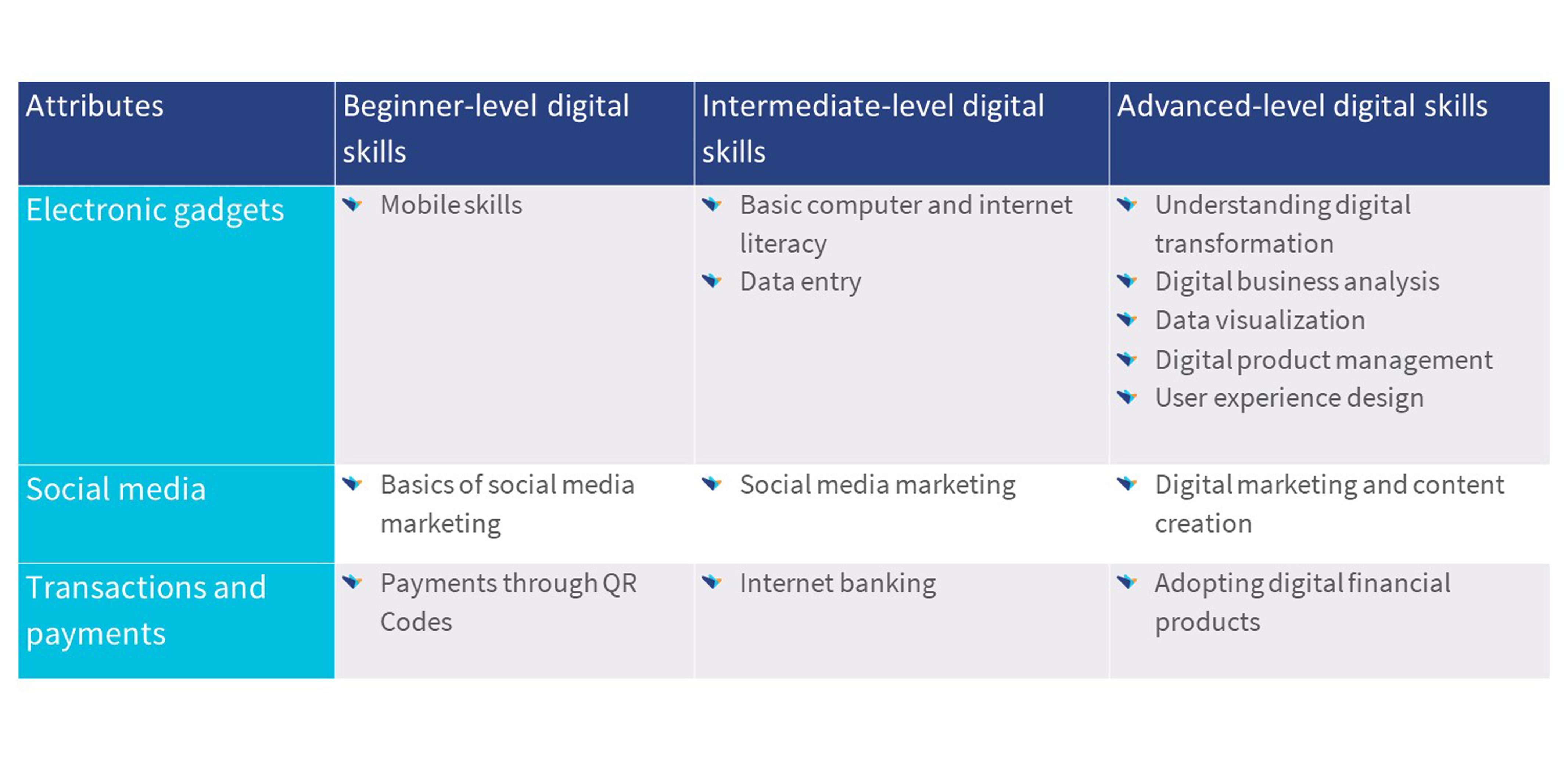

A recent ILO study suggests new technologies in enterprises enhance how well they can increase productivity, create employment, reduce poverty, and promote local development. We classify digital skill tools into beginner-, intermediate-, and advanced-level digital skills (see Table 1).

Table 1: Need for different digital skills for young entrepreneurs at various stages of evolution

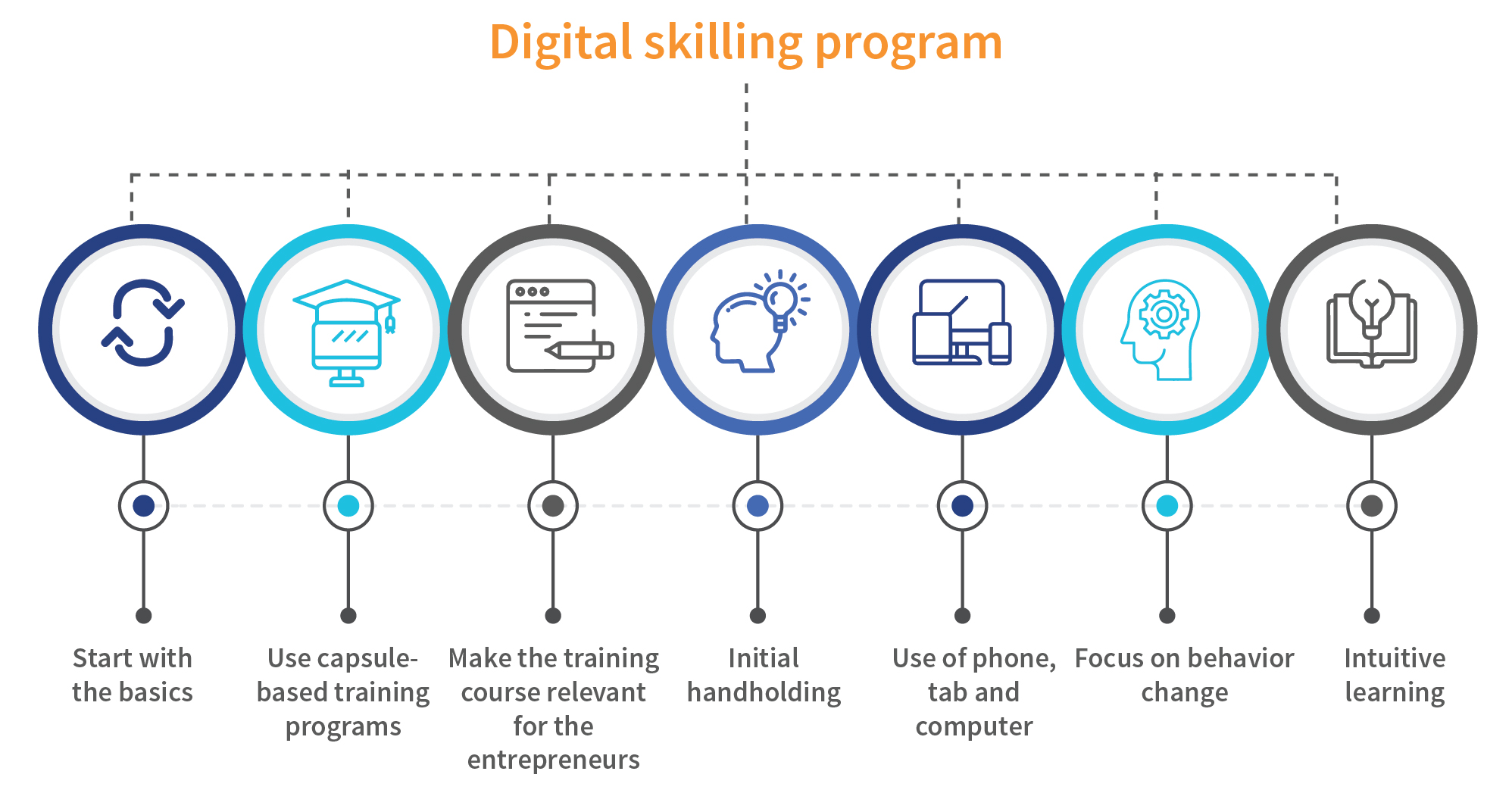

Critical lessons from MSC’s 15 years of experience in making digital skills training more effective

- Start with the basics: Start the training with the basics of digital skills and gradually move to intermediate and advanced skills based on the need of the enterprise

- Use capsule-based training programs: Starting or running an enterprise is time-consuming, so it is vital to understand that we divide a training module into tiny capsules to ensure better use of the entrepreneurs’ time. MSC through its training arm, the Helix Institute at MSC has developed a course in collaboration with the Mastercard Foundation, “Getting started in entrepreneurship.” We deliver this course in a self-paced mode on our learning management system (LMS).

- Make the training course relevant to the entrepreneurs: Use visualization tools to make the entrepreneurs understand the relevance of the digital skill training for their enterprise; use relevant and impactful images and local language to guide users through the interactive activities

- Deliver intuitive learning: Include elements of gamification and fun in interactive learning; gamify progression across modules, so the learners are motivated along the process; incentivize learners for certification, and mentorship opportunities

- Focus on behavior change: Anchor the design on the desired behavior and the pathway to move from the current behavior to entrepreneurial behavior.

- Provide initial handholding: Users initially need guidance but can quickly start taking the lessons forward. Hence, an initial handholding is vital to building a foundation for the skill training and confidence in it.

- Use a phone, tablet, or computer: The training needs to be delivered using a phone, tablet, or computer to maximize the adoption of these digital skills.

Figure 2 showing different elements that can make digital skills training effective

Figure 2 showing different elements that can make digital skills training effective

Our approach to delivering a digital skilling program

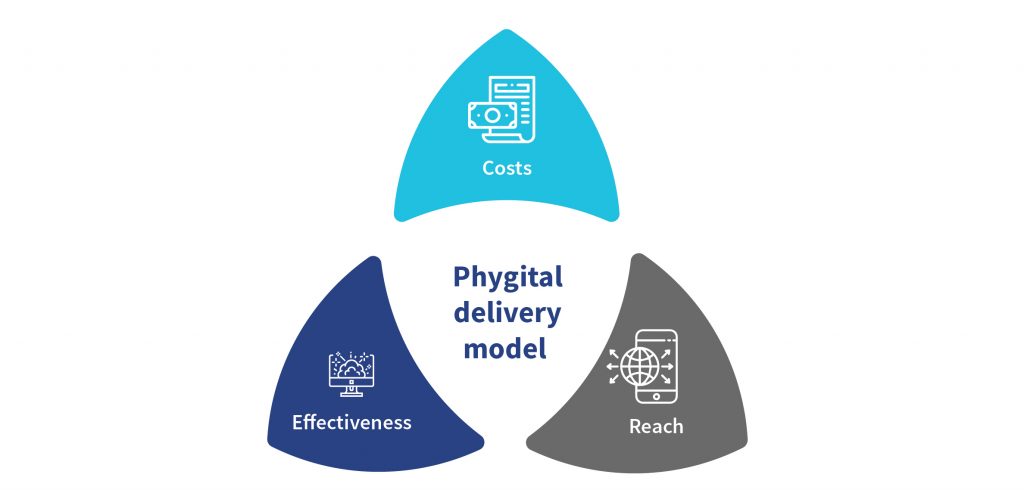

A critical step needed to foster digital skills among young entrepreneurs is to deliver the program effectively. Digital skilling programs can be delivered through different channels.

- Online skilling program: Online skilling programs use digital means to enhance the learners’ skills and capacities. This mode of delivery provides high value for money and is scalable; however, it offers limited interpersonal relationships. The effectiveness of online course delivery depends on the learner’s motivation level and appropriate course design and delivery tools.

- In-person skilling program: In-person skilling programs score high on effectiveness; however, the costs are comparatively high and not immensely scalable.

- Phygital model: Our approach is to design and deliver digital skilling programs that balance reach with effectiveness and cost of delivery. The phygital (physical+digital) skilling program combines in-person training to onboard people to digital means of learning. Our financial literacy program for refugees and the host community for UNCDF in Tanzania combined phygital approaches. The program covered mobile money and formal financial services, savings groups, and managing money. We suggest using a phygital model of delivery for such skilling programs to empower young entrepreneurs for sustainable learning.

Figure 3: Phygital delivery model

Young entrepreneurs must be supported to reduce digital skills gaps

Emerging economies require digitally savvy young entrepreneurs to build robust digital economies. By enhancing the digital skills of young entrepreneurs to transform their new and existing enterprises, we contribute to their increased productivity and employment opportunities. Government and funding agencies have an essential role in reducing the digital skill gaps among young entrepreneurs by introducing digital skill-building courses.

MSC worked with institutions like Expresso to improve the incubation approach in providing training and support to aspiring young entrepreneurs, allowing them to develop innovative solutions. In this partnership, we performed activities like mentor connect, The Hub for Digital Finance, coaching sessions, boot camps for startups and young people, and identification of customer segmentation. This program benefited almost 200 young people in Senegal. For more details on our work with young people, click here.

Banking Correspondent (BC) Agent incentives – Eko India financial services

The business correspondent (BC) network in India has become indispensable for last-mile financial service delivery across urban and rural centers. Incentives provided through agent network manager (ANM) platforms are a critical factor that motivate these BC agents to provide quality services at their outlets. The incentives provided to these agents need to be transparent, regular, and reasonable to ensure good business at agent outlets.

Eko is a leading FinTech platform that saw low motivation among its agents and identified incentives to be one of the major factors for this.

This video takes you through the journey of Eko’s agents and the role of incentives in their overall business. It looks at Eko’s strategy to improve the incentive structure for its agents with MSC’s support. It captures the impact of changes in Eko’s incentive plans on different agents associated with the platform.

Role of technology in scaling up the BC Sakhi network in Uttar Pradesh: A lesson for other states

BC Sakhis have emerged as a convenient last-mile interface of banks, especially for cash-in and cash-out transactions. However, many rural adults in the country lack access to basic financial services either through banks, BC agents, or other modes. The situation in Uttar Pradesh was no different. Many rural areas in the state lacked access to financial services.

To improve the access to financial services in the state, the state government of Uttar Pradesh launched its “One Gram Panchayat – One BC Sakhi” initiative in 2020.

Mobilizing rural women as potential business correspondent (BC) candidates in the state was a mammoth and complicated exercise, given the sheer number of BCs, currently at around 58,000. The case study charts how UPSRLM utilized technology to address the challenge of setting up a large-scale BC Sakhi network and operationalizing it in the state while managing associated risks.

Job losses, business closure — Covid hit female entrepreneurs. Here’s how to support them

Godavari Chandrasekhar, 31, used to run a small vehicle repair shop with an annual income of just Rs 1-2 lakh. She gradually started offering diversified services and scaled up her business to a vehicle servicing centre, which now earns her more than Rs 6 lakh annually.

Godavari has transitioned from being a necessity entrepreneur to an opportunity entrepreneur. However, this is not true for millions of women entrepreneurs in India, many of whom remain stagnating in micro and small survivalist enterprises.

Increasing economic opportunities for women is the key to accomplishing the vision for development set forth in the United Nations Sustainable Development Goals (UN SDGs).

Women constitute 13.3 per cent (8 million) of the total 58.5 million entrepreneurs in India, 82 per cent of them in micro-units run as sole proprietorships.

Studies suggest that 10 to 30 per cent of the enterprises registered as ‘women owned’ are not actually owned, controlled, or run by women. The pandemic has further worsened the situation and put women entrepreneurs at higher risk of business closure. Recent research by Microsave highlights that as many as 82 per cent of women-owned micro, small or medium enterprises (MSMEs) reported a decrease in their income, as compared to 72 per cent of male-owned enterprises. They face greater restrictions, decreasing demand, rising costs of inputs, inability to access markets, and an increased burden of care work at home, among other factors that severely affect their income. The story is no different for the startup sector. Funding for women-founded and co-founded startups in India fell by 24 per cent due to the impact of Covid-19.

Need for initiatives

Why is it urgent to create, sustain and help more women to run growth-oriented profitable businesses?

During the Covid-19 pandemic, women faced more job losses and closure of their businesses than men. This was coupled with the automation of routine jobs, which means that economic opportunities for women may continue to shrink. Furthermore, the increased burden of care work also means women have less time for work outside the home that earns them an income. In the absence of a suitable ecosystem promoting women’s entrepreneurship, there is a risk of women’s labour force participation declining further.

Entrepreneurial ecosystems are much like biological environments where different important elements — regulatory, cultural, and economics, in this case — interact with each other to form an optimal environment for talented individuals and innovative organisations to create value if they are appropriately combined and supported. The caveat here is optimal integration and support. Such an integrated system to promote opportunity-oriented entrepreneurship among women in high-value and high-growth sectors is an urgent need.

Numerous studies and our field observations suggest that lack of relevant financial products and enterprise development services along with gender specific barriers discourage women from pursuing entrepreneurship.

Yet, not all is lost. Innovative initiatives to promote women’s entrepreneurship, driven by private and public sector partnerships like Niti Aayog’s Women Entrepreneurship Platform (WEP), offer promise. The WEP acts as a single window for women entrepreneurs to obtain information about government schemes, marketing assistance, funding, and compliance support for their businesses. Another important initiative has been government-led market linkage support for artisans and self-help group-based women entrepreneurs. The annual ‘Saras Aajeevika Mela’ (fair) and events like ‘Hunar Haat’ enable a direct consumer connect for women from all corners of the country. These fairs attract huge footfalls and provide markets and visibility to women entrepreneurs.

More recently, UN Women has enabled State Bank of India (SBI) to launch a Women Livelihood Bond scheme. This scheme is designed as an innovative financial instrument to drive social impact. It gives the private sector the opportunity to invest in women-led enterprises, while allowing SBI to raise low-cost funding. This unique scheme will not only increase women’s access to institutional credit but will also provide support to scale their businesses, consequently spurring rural economies and job creation. Amazon’s timely launch of a store exclusively for women-owned businesses in association with UN Women is a wonderful opportunity, especially in the aftermath of the pandemic where businesses are turning to technology to access markets. As suppliers and customers move online, a conducive atmosphere is being created for women entrepreneurs to negotiate prices, market their products, and reach consumers anywhere in the world.

Ways to enable women-led startups

We suggest six key enablers that would encourage more women to take the road to entrepreneurship:

The first is family support. Social norms and the level of family support can influence and shape women’s decisions, such as the location of the businesses, feasibility of work travel, time spent on business activities, and networking. A recent paper shows how policies meant to encourage female entrepreneurs to migrate to higher-return enterprise sectors should aim to effect change in gender norms at home.

The second enabler is facilitating women’s access to markets and networks. Women’s limited mobility, along with a greater burden of unpaid care work, means that women are not well integrated into formal and informal networks. They do not have access to markets, with low or no representation in local business associations. Better access to market information is a well-documented benefit of mobile phones. However, the digital divide impedes access to e-markets. As per the National Family Health Survey 5 (NFHS 5), less than 3 out of 10 women in rural India, and 4 out of 10 women in urban India have ever used the Internet.

Third, we must make more women leaders in business visible to create role models for young girls, and encourage mentorship wherein successful business leaders contribute back to society by mentoring potential and early stage entrepreneurs. This will create a pipeline of future women entrepreneurs.

Fourth, education in business skills and technology can be a great enabler. Deliberate efforts are required to improve women’s participation in industry-aligned skilling programmes at all levels, across low, medium, and high-skill industrial sectors, preparing women for entrepreneurship opportunities in future-oriented industries.

Fifth, access to capital, or sufficient capital, is a necessary precondition for any enterprise’s creation and expansion. While all entrepreneurs navigate complex challenges and competitive markets, women entrepreneurs face specific regulatory and social hurdles that limit equal access to the assets, credit, and capital required to establish and grow their businesses. UN Women recently ran a survey of 105 women entrepreneurs to understand the impact of Covid-19 on women-owned businesses. The survey found that 70 per cent of women-led enterprises have no history of taking formal loans. Appropriate and relevant products, easing access to long-term and affordable capital for different segments of women entrepreneurs is crucial.

Sixth, it is important to have a supportive public and private sector. The cultures and practices of public and private sector institutions and businesses have a significant impact on women’s economic opportunities. Public and private sector entities have the levers of control to sway the ecosystem in favour of women entrepreneurs when they desire to do so. For example, the government has steadily increased the share of public procurement from women-owned businesses from zero in 2017 to 0.55 per cent in 2020-21. Before Covid-19, only 17 per cent of women entrepreneurs reported awareness about government schemes. It is important to address this information asymmetry and increase convergence among different government programmes for women. It is also important to provide incentives and recognition to industries sourcing from women entrepreneurs, as well as certifying women-owned enterprises. Private sector entities can better integrate women in their supply chains, invest in promising women-led start-ups, and support the creation of an affordable, quality universal child-care system for the country.

Public and private sector players must work on these ecosystem enablers to create future business leaders.

Women business leaders will help achieve the Sustainable Development Goals through their energy and innovation. Women business leaders with a seat at the decision making table can contribute to solving humanity’s toughest challenges like climate change, poverty and disease. We need one hundred per cent of our business talent to kick start the global economy, post the pandemic. This will depend on our ability to unlock the choked pipeline of women’s talent.

The Print first published this article on 19th March, 2021.