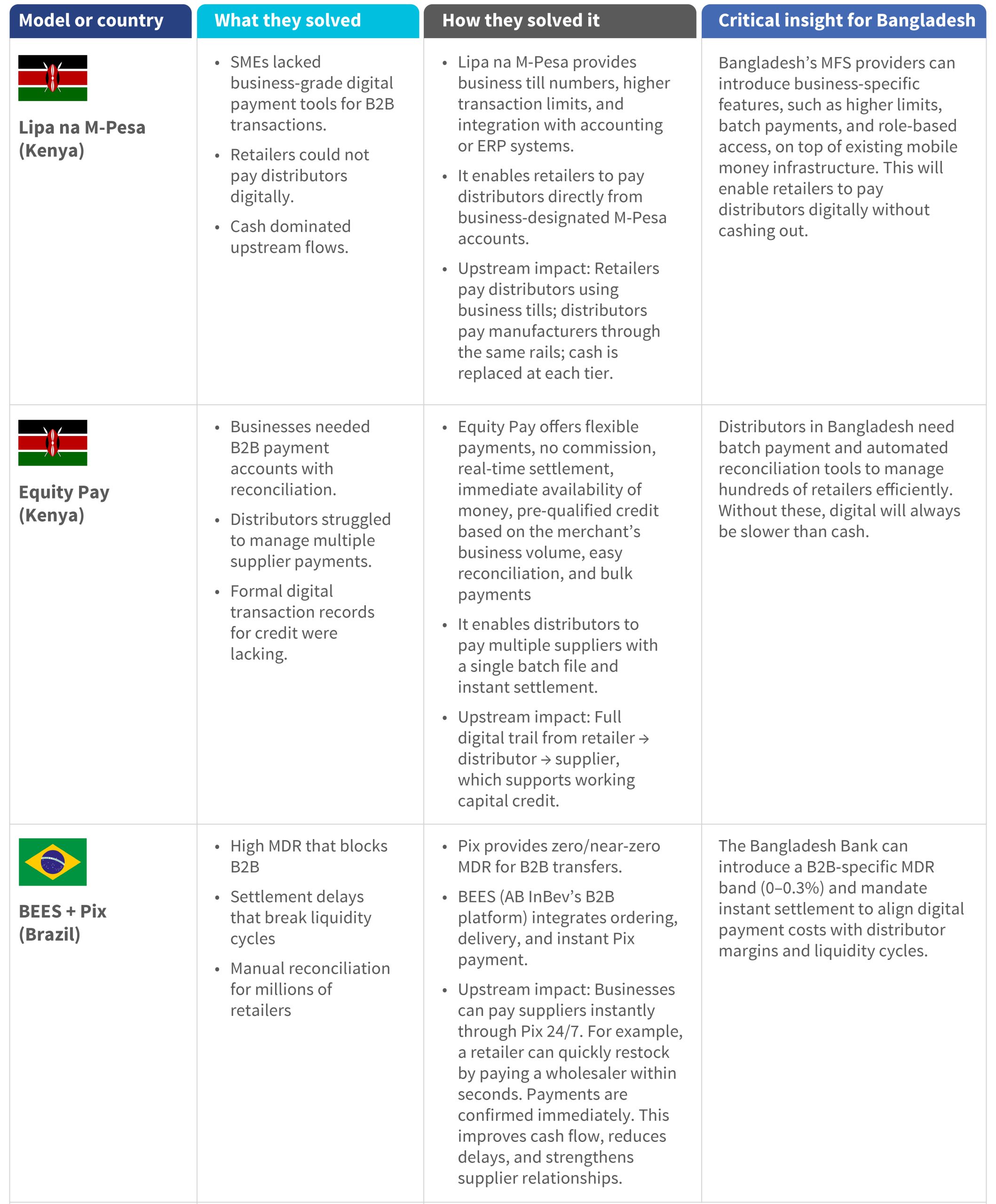

Rwanda’s digital money efforts have reached 85.3% of Rwandans, or 7 million people. The difficult question is whether it works for them, and the case of two Rwandans makes that clear. The first is a salaried civil servant in Kigali who pays her electricity bill, her children’s school fees, and her health insurance entirely through her phone. She never visits a single counter. The second is a young woman who sells vegetables at a weekly market in the Southern Province. She has heard of mobile money and even lives within walking distance of an agent. Yet, she does not own a mobile phone, lacks a regular income, and has never made a digital transaction in her life.

Both women are Rwandan adults. Yet, only one of them is counted among the 85.3% of Rwandan adults who are now digitally financially included, based on the AFR FinScope 2024 Digital Financial Services Thematic Report. This figure places Rwanda among the highest-included countries in sub-Saharan Africa, a remarkable leap from just 46% in 2016. However, behind it lies a more complex story about who digital financial services truly reach and how they do so.

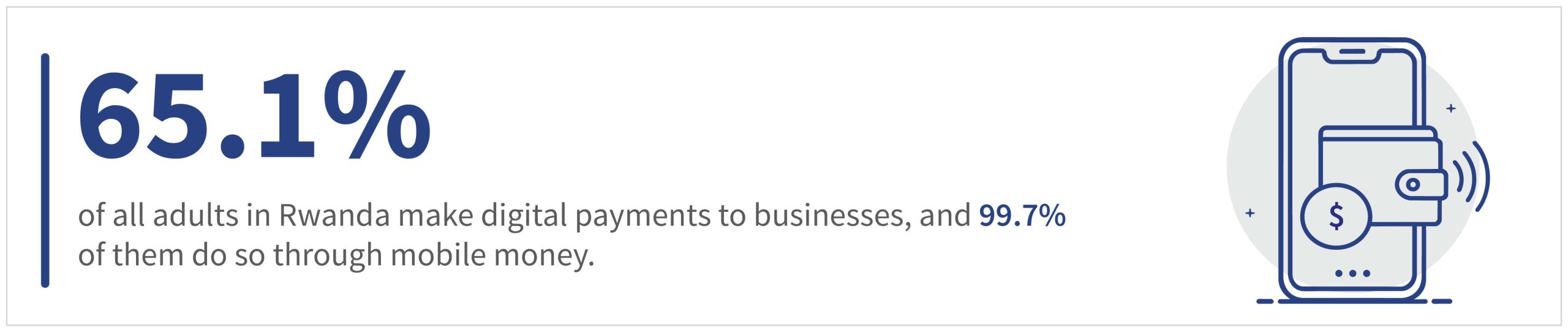

Rwanda’s digital financial inclusion story is one of mobile money. The AFR FinScope 2024 report shows that the vast majority of adults now have access to mobile money services, while banks serve just 1.5% of adults. These mobile money platforms, not bank branches, brought most Rwandans into the financial system. The mobile money services are delivered through basic phones and SIM cards, primarily through providers, such as MTN Rwanda and Airtel Rwanda.

People are drawn to mobile money platforms above all by the need to pay businesses, especially for medical expenses, utilities, and airtime, which top the list. Rwanda’s national digital payment platform is eKash. It enables instant, interoperable transfers across banks and mobile money networks, which makes these everyday transactions seamless.

Government and regulatory action have amplified this momentum. The National Bank of Rwanda’s Payment System Strategy and Law No. 061/2021 mandated interoperability across providers. The Twagiye Kashiresi digital literacy campaign boosted merchant payment volumes, while the COVID-19 period served as an accelerant. Estimates indicate that 9% of Rwandan adults became first-time mobile money users during this period, with an additional 13% who increased their usage.

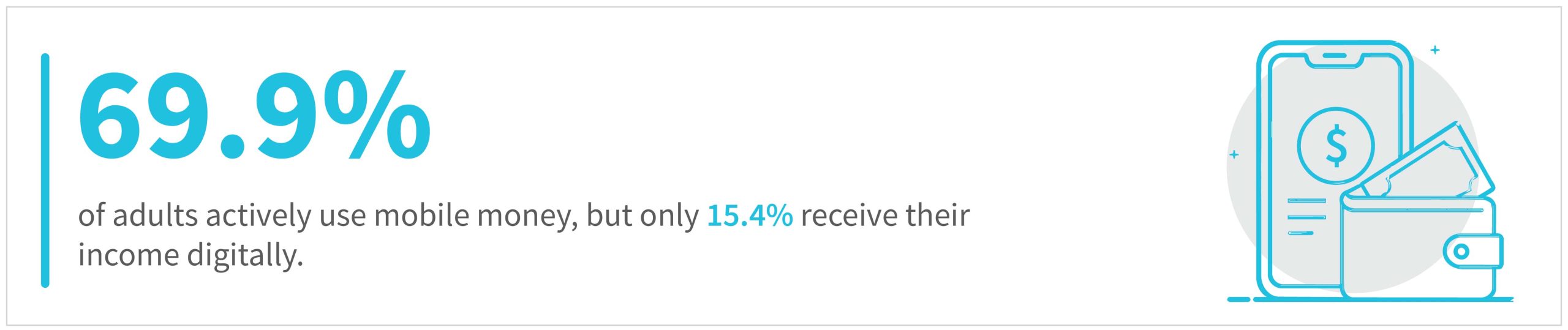

Yet, access is not the same as use, and use differs from transformation. Rwanda has built a remarkable platform, but the data shows that most people use it primarily for bill payments. The fuller potential of this platform includes digital wage receipts, safe savings, and loan repayment without a branch visit, which remain out of reach for most.

Only 15.4% of adults receive their income digitally. Most of those who do save formally keep their money in a mobile money account, yet informal channels still command a significant share of savings. For many people, especially those with low and unpredictable incomes, savings groups offer a more flexible, accessible, and trusted way to manage money. Village savings and loan associations (VSLAs) are groups that allow small, frequent contributions and quick access to funds when needed, and only 14% of borrowers repay loans digitally.

Rwandans use digital accounts for transactions, but not yet as tools for financial management. This is the access-usage gap, and it matters because the transformative potential of digital finance lies not in the payment itself, but in what the payment can unlock.

The 1.2 million adults who remain entirely excluded have a clear profile. Rural residents comprise 84.7% of this group, and women account for 61.2%. Half of the excluded are young, and 80% have not progressed beyond primary school. Casual workers and street vendors account for nearly half of this group at 44.9%, and most earn irregular incomes with no steady relationship with any financial institution.

The primary barrier is simple and concrete, as 68% of non-mobile money users cite a lack of cell phone ownership as the main reason for not using mobile money. It is not the complexity of service, high fees, or distrust of the system. The network infrastructure around many of these people already exists, with 69.6% of excluded adults living within reach of a reliable Global System for Mobile Communications (GSM) signal. The infrastructure is largely in place, but most excluded adults do not own a device.

Beyond devices, attitude plays a role. Many excluded adults prefer to deal with people rather than machines and prefer cash payments. These attitudes are not irrational preferences, as they reflect trust, habit, and the social fabric of informal financial life, but they are also addressable. 65.3% of excluded adults live within 1 km of a mobile money agent, which means the last mile is shorter and more solvable than it seems.

Exclusion also has a gender dimension, as two out of every three excluded adults are women. The gender gap in digital financial inclusion is present across all age groups and widens with age, which reflects deeper structural constraints. Lower phone ownership, less control over household income, and reduced exposure to formal financial services all play a role.

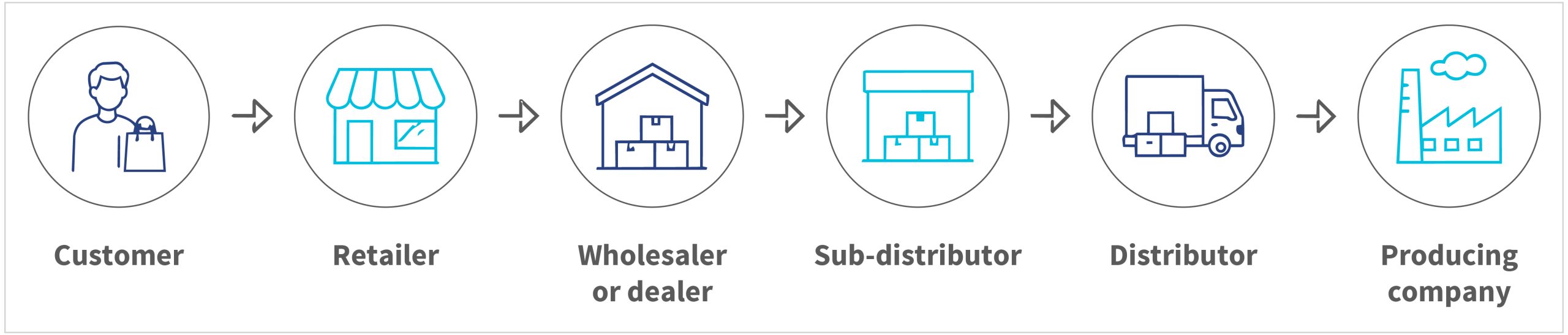

Kenya’s M-Pesa is the most-cited comparator for Rwanda. M-Pesa turned a payment tool into an economic lifeline in Kenya, with more than 34 million subscribers and 300,000 agent outlets. It enabled microloans, salary disbursement, and integration into government services. The lesson is that coverage and ecosystem depth determine how widely people use a platform.

India’s Aadhaar-enabled ecosystem offers a second model for Rwanda. India simplified the account-opening process and enabled direct benefit transfers at scale by linking biometric identity to financial access. Rwanda’s existing national ID infrastructure and eKash platform are natural foundations for a similar approach, particularly for the Umurenge SACCOs and cooperatives that remain only partially connected to the national payment switch.

Nigeria’s interoperability push shows how cross-platform connectivity expands trust and use among previously excluded populations. Rwanda’s eKash is already a move in this direction. Yet, full extension to savings and credit cooperative organizations (SACCOs) that serve rural communities remains an unfinished piece of the puzzle.

On the technology frontier, AI credit models can use mobile money transaction history to extend small loans to users without formal credit records. Rwanda’s planned CBDC pilots from 2026 offer an entry point to bring excluded populations into the digital system for the first time through transparent government-to-person payments. These tools shift the system from access to utility.

Rwanda’s digital financial inclusion journey has reached an inflection point. The groundwork is largely in place, with the mobile money built, agent networks expanded, and the near-universal access achieved in urban areas. The country should be proud of this next step that goes beyond technology to reach a point where digital financial services become genuinely useful and trusted. These services should reach the vegetable seller in the Southern Province, the rural woman without a phone, and the young casual worker who has never had a reason to go digital.

Affordable devices, liquid networks of well-trained agents in the most underserved zones, and products designed for irregular incomes rather than salaried employees alone must drive the next step. It means fee transparency, local-language interfaces, and patient community-level work to build digital confidence where cash remains the default.

The AFR FinScope 2024 report provides Rwanda’s policymakers, providers, and development partners with a precise map of where the gaps are and who carries them. Rwanda has solved access, and the next step will not be measured by the number of accounts opened, but by the lives changed.

This blog draws on findings from the AFR FinScope 2024 Digital Financial Services Thematic Report, published by Access to Finance Rwanda.