“Cookie-cutter” solutions for merchants will not work

by Sunil Bhat, Amit Joshi, Priya Garg, Kritika Shukla and Shreya Gupta

by Sunil Bhat, Amit Joshi, Priya Garg, Kritika Shukla and Shreya Gupta Mar 18, 2019

Mar 18, 2019 5 min

5 min

This series of blogs highlight that providers cannot promote merchant payments through standard “cookie-cutter” solutions. What works for one category of merchants may not work for the other category. We need to look at merchants as distinct personas to decipher their characteristics and explore ways to change their behavior.

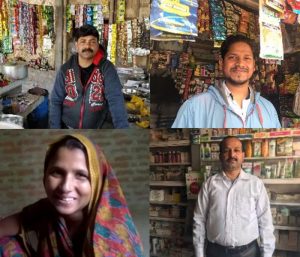

Sanjay, Deepak, Pushpa, and Shailendra are merchants in different parts of India who sell goods from their own shops. They interact and transact with a variety of customers on a regular basis. To a varying degree, all four share a few common traits. They feel that digital payments are good for them. All of them have experienced banking and used financial services at different levels. They show a willingness and capacity to become offline merchants and join the digital bandwagon.

Sanjay, Deepak, Pushpa, and Shailendra are merchants in different parts of India who sell goods from their own shops. They interact and transact with a variety of customers on a regular basis. To a varying degree, all four share a few common traits. They feel that digital payments are good for them. All of them have experienced banking and used financial services at different levels. They show a willingness and capacity to become offline merchants and join the digital bandwagon.

What is it that makes them different from each other?

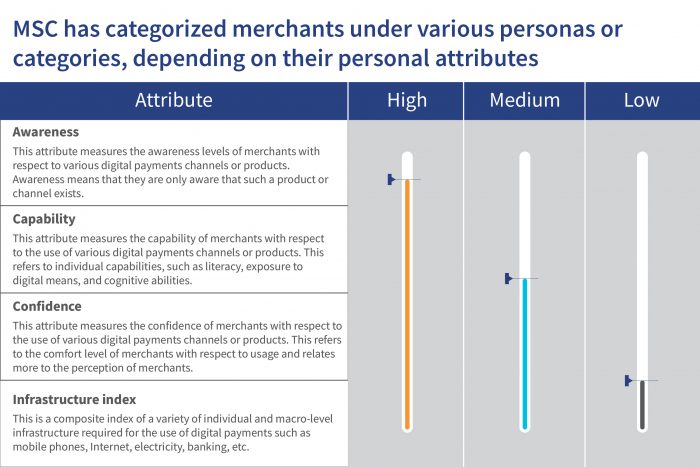

When it comes to accepting digital payments, each of these merchants sells different types of products, have different financial lives, and exhibit different levels of motivation. They meet different types of customers—some who are “pro-digital payments” and others who do not understand or wish to understand the role or benefit of paying digitally. We have used the following four parameters to segment merchants into distinct personas.

Merchants like Sanjay and Deepak are positive about digital payments and continue to pursue their customers to pay digitally, whereas Pushpa and Shailendra seem less enthusiastic. All four of them need different types of nudges and forms of support to accept digital payments. They exhibit different belief systems and goals to make choices while accepting payments.

The retail payment landscape in India

The retail payment space in India is proving to be a battleground for digital service providers (DSPs), both for the incumbents like banks and challengers like FinTechs. A BCG-Google study estimates that the digital payments market is set to grow to USD 500 billion by 2020. This includes person-to-person (P2P), person-to-merchant (P2M), merchant-to-merchant (M2M), and person-to-government (P2G) payments. Meanwhile, a recent Credit Suisse study estimates that the digital payments market will grow to USD 1 trillion by 2023. The report says that currently in India, cash transactions account for approximately 90% in terms of volume and 70% in terms of the value of total transactions. With a high affinity to cash, India offers a huge opportunity for payments players.

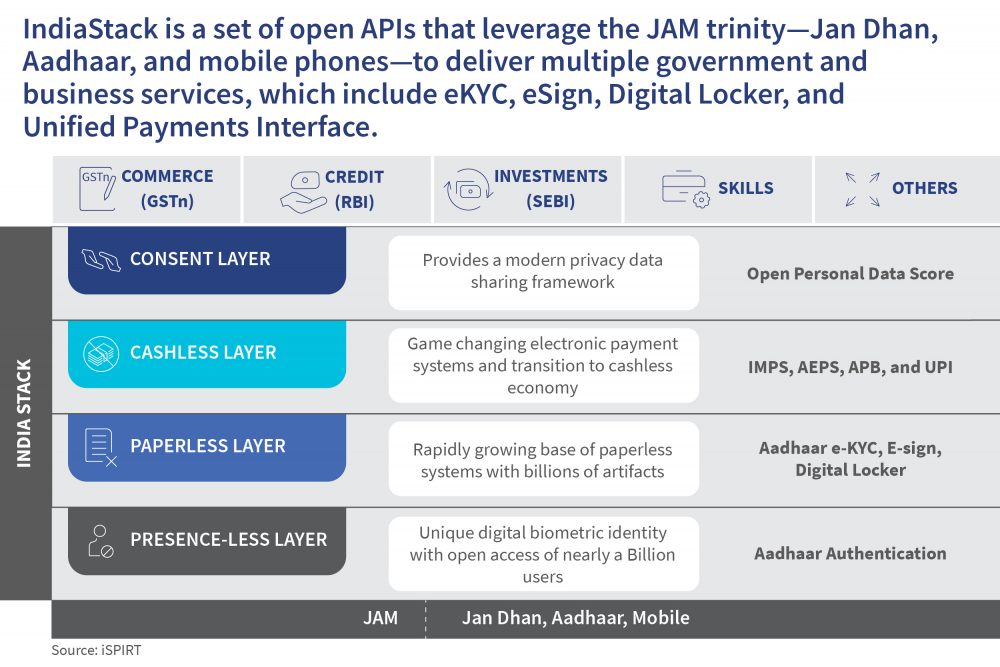

The Government of India launched its flagship “Digital India” program with a vision to transform India into a digitally-empowered society. It prioritized the use of digital payments by each market segment. The vision is to provide seamless digital payments to all citizens of India in a convenient, easy, affordable, quick, and secure manner. To achieve this, the government articulated “faceless, paperless, cashless” as part of Digital India and developed IndiaStack, a presence-less, paper-less, and cashless ecosystem for delivery of services.

IndiaStack is a set of open APIs that leverage the JAM trinity—Jan Dhan, Aadhaar, and mobile phones—to deliver multiple government and business services, which include eKYC, eSign, Digital Locker, and Unified Payments Interface.

The Indian government and the national regulator—the Reserve Bank of India (RBI)—have designed various incentives and policies on the supply side to promote digital payments. One such move was the rationalization of Merchant Discount Rates (MDR) by the RBI to promote debit card acceptance by a wider set of merchants, especially small merchants. As part of this move, the RBI allowed a temporary waiver of MDR for small-value transactions (up to INR 2,000) for two years on all debit card, Bharat Interface for Money (BHIM), Unified Payments Interface (UPI) and Aadhaar-Enabled Payment System (AePS) transactions.

The RBI also permitted cooperative banks, which are well entrenched in rural areas, to deploy their own or third-party point-of-sale (POS) terminals. Cooperative banks can now also install onsite or offsite ATM networks, issue either debit or credit cards or both—either on their own, through sponsor banks or through a co-branding arrangement with other banks.

On the demand side, the past decade has seen tremendous growth in the use of the Internet and mobile phones in India. With a population of 1.34 billion and close to 1.18 billion mobile phone subscribers , 446 million internet users, and 386 million smartphone users, India has all the ingredients in place to develop a vibrant merchant payments ecosystem. The BCG-Google report on digital payments estimates that the size of the person to business (P2B) digital payment market is about to grow to USD 224 billion by 2020. This means that more Sanjays, Deepaks, Pushpas, and Shailendras will join the digital ecosystem—of course, with a little help from service providers.

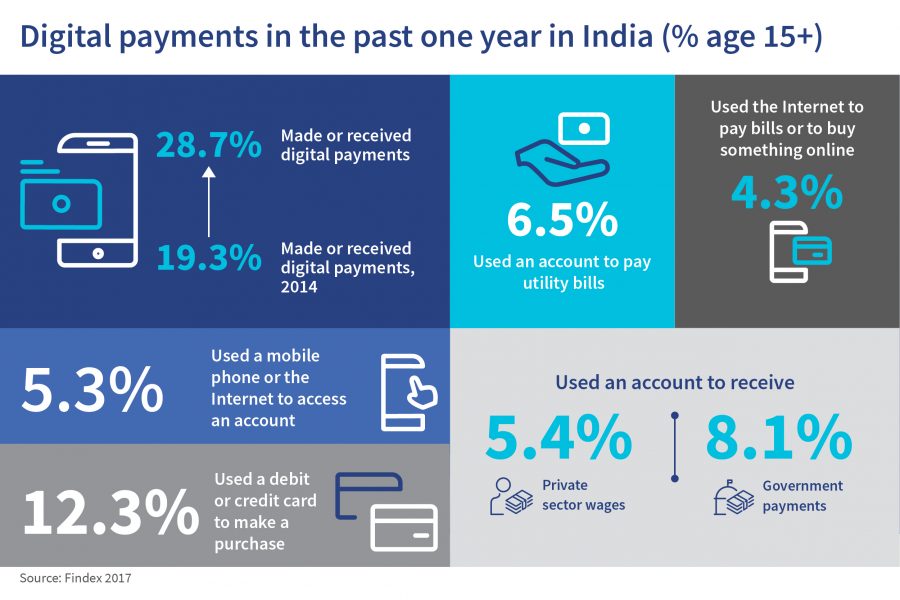

We can also look at the progress in the digital ecosystem in India based on the macroeconomic data from Findex 2017. The Little Data Book on Financial Inclusion 2018 highlights a commendable achievement on access to financial services. The flagship Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme has played a major role, resulting in the creation of bank accounts for close to 80% of the adults, including 76% of women.

Unfortunately, the same cannot be said for usage. The table shows the percentage of digital transactions conducted by adults in India in the calendar year 2017. This shows how much more must be done to ensure that people transact digitally.

This data shows that there is minimal activity on the side of merchant payments. Only around 6% of merchants in India use digital payments. This means that customers still use cash to make most of their bill payments, while merchants are also happy or content in accepting cash. This, in turn, implies that we need to support more such Sanjays and Deepaks as we motivate more Pushpas and Shailendras.

Considering the size of the economy, India shows an immense potential around merchant payments, which have a high probability to act as a hook for customers to start transacting digitally. MSC’s practical insights highlight that getting merchants to transact digitally is a key challenge. To probe this further, MSC conducted a research activity with merchants—those who accepted digital payments and those who did not—to gather behavioral insights into accepting payments digitally.

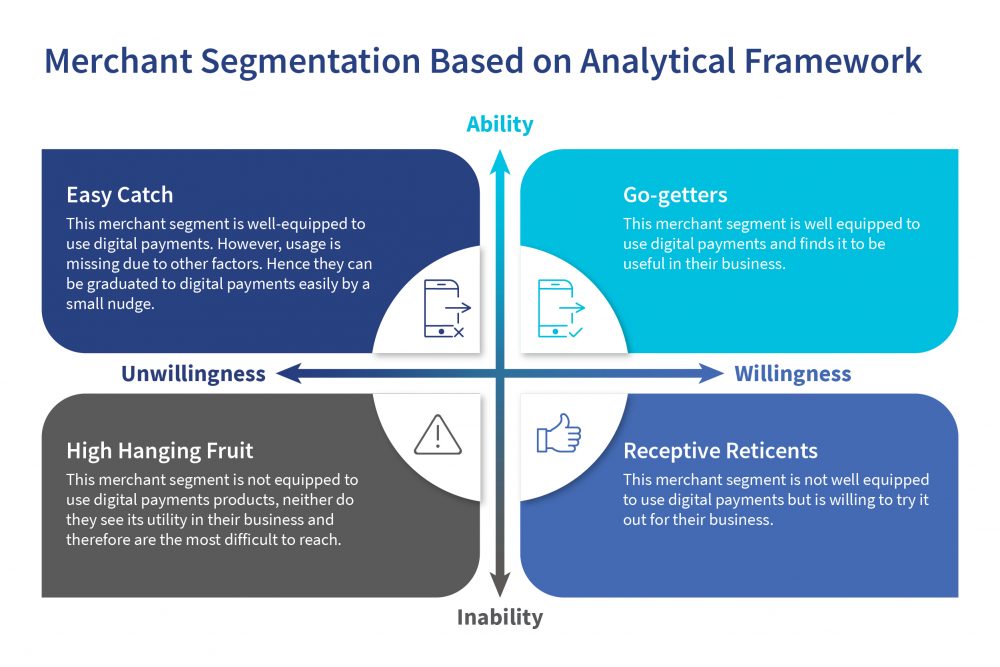

We came up with this series of blogs based on these insights. We have categorized merchants, as shown below, under various personas or categories, depending on their personal attributes, across the two dimensions of ability to accept digital payments and their willingness to do so. These categories are go-getters (Sanjays), receptive reticents (Deepaks), high-hanging fruits (Pushpas) and easy catches (Shailendras). Additionally, there is another category of merchants termed as “drop-outs”. Merchants in this last category have tried digital payments for their businesses at some point in time, but have gone back to cash in the absence of an appropriate value proposition and adequate support.

This series of blogs highlight that providers cannot promote merchant payments through standard “cookie-cutter” solutions. What works for one category of merchants may not work for the other category. We need to look at merchants as distinct personas to decipher their characteristics and explore ways to change their behavior.

Written by

Sunil Bhat

Partner

Amit Joshi

Senior Analyst

Kritika Shukla

Project Manager, RBIH

Leave comments