Go-getters and receptive reticents—Merchants who have the instinct, but need support

by Sunil Bhat, Amit Joshi, Priya Garg, Kritika Shukla and Shreya Gupta

by Sunil Bhat, Amit Joshi, Priya Garg, Kritika Shukla and Shreya Gupta Mar 18, 2019

Mar 18, 2019 4 min

4 min

This is the second blog in the series on “Digitizing merchant payments in India”. The first blog discusses the potential of merchant ecosystem in India and the need to design distinct solutions for different merchants. In this blog, we will discuss two merchant personas: a) The go-getters and b) The receptive reticents.

This is the second blog in the series on “Digitizing merchant payments in India”. The first blog discusses the potential of the merchant ecosystem in India and the need to design distinct solutions for different merchants. In this blog, we will discuss two merchant personas: a) The go-getters and b) The receptive reticents.

MSC used its Market Insights for Innovations and Design (MI4ID) approach to understanding the barriers to adoption of digital payments by different merchant personas. MSC had also used the MI4ID approach in its cashless experiments in Kerala and Odisha to understand the digital traits and hindrances in the adoption of digital payments products among low-income people. In this blog, we will discuss two merchant personas: a) The go-getters and b) The receptive reticents.

MSC used its Market Insights for Innovations and Design (MI4ID) approach to understanding the barriers to adoption of digital payments by different merchant personas. MSC had also used the MI4ID approach in its cashless experiments in Kerala and Odisha to understand the digital traits and hindrances in the adoption of digital payments products among low-income people. In this blog, we will discuss two merchant personas: a) The go-getters and b) The receptive reticents.

The go-getters

Sanjay is a merchant who operates in the Green Park area of Delhi. He is a middle-aged man and owns a mid-size grocery store that has a high footfall. He is a graduate and clearly shows business acumen. He likes to experiment and is open to trying new payments channels—as long as he sees benefits in them. The heavy traffic of customers in his shop has made him keen to use digital payment services, which offer speed and convenience to customers. Sanjay is also ready to pay for the associated charges. In addition to cash, he accepts digital payments using wallets like MobiKwik and Paytm, as well as card-based payments through a point-of-sale (POS) machine.

Sanjay belongs to the genre of “go-getters” who believe in trying out new payments mechanisms. This segment is not afraid to experiment and shows a remarkable ability and willingness to try out new modes of accepting digital transactions (Behavioral trait: pragmatist). Even after falling prey to a vishing (voice phishing) fraud with one leading wallet provider, where he lost about INR 6,000 (USD 86), he continues using the same wallet because he accepts his mistake and takes the blame. In our interviews, he revealed that the demonetization announcement in November 2016 nudged him to explore the digital channels like Paytm.

What makes Sanjay a go-getter?

This segment of merchants is highly customer-centric and enthusiastic about various modes of digital payments. They play an important role in creating customer awareness and convincing them to pay digitally.

Hence, they have the potential to become “brand ambassadors” of various digital payments channels or products.

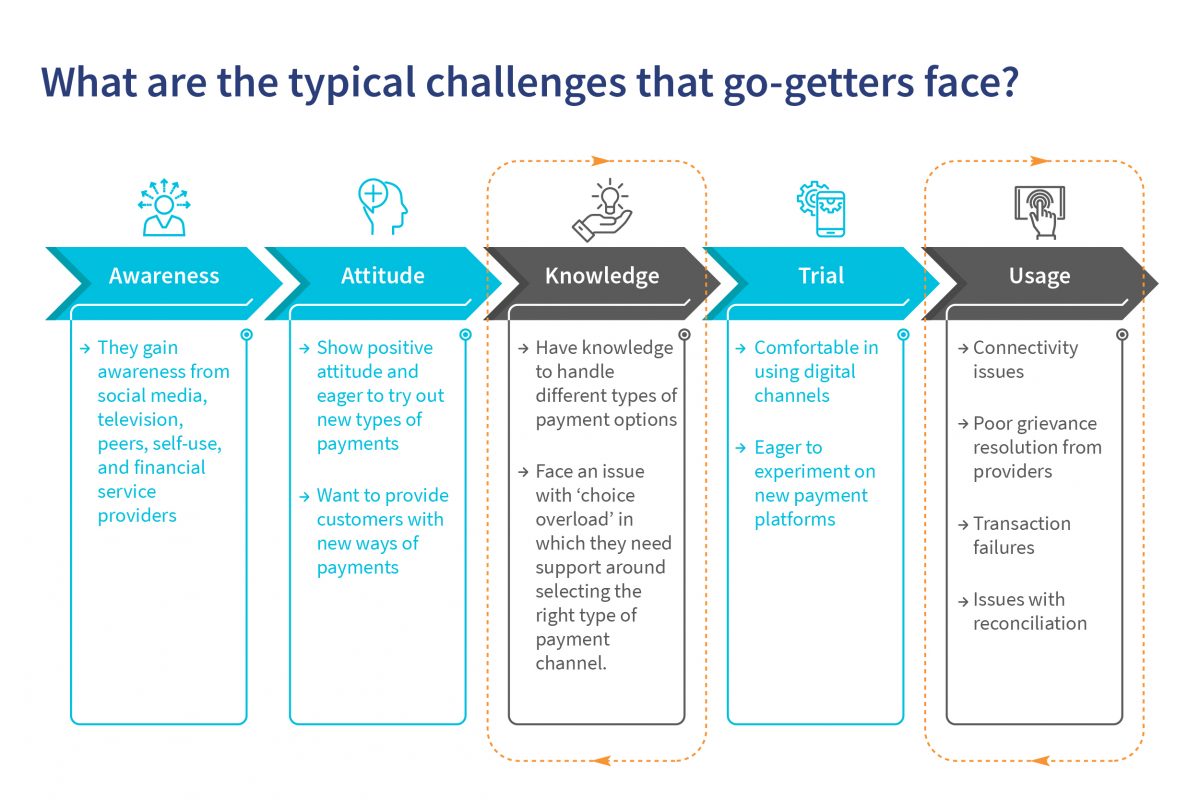

What are the typical challenges that go-getters face?

Connectivity issues mar the customer and merchant experience alike. While our team was interacting with Sanjay, he tried accepting a customer payment on POS. The transaction failed five times before being successful on the sixth attempt!

How do we keep go-getters interested in digital payments?

Merchants like Sanjay are the “poster boys” of merchant ecosystems who hold great promise. Supporting them is important for the overall proliferation of digital payments in the country. Hence, acquirers or providers need to create and provide appropriate solutions to them. The diagram below illustrates some ways in which providers can support this category of merchants.

The receptive reticents

Deepak Das, a 40-year-old semi-literate man, runs a grocery store built on his plot at Bhojerhat on the outskirts of Kolkata. He has been managing his shop for 10 years. On average, 30-40 customers visit his outlet each day. He often visits Kolkata with his family for shopping during the festive season. At Big Bazaar in Kolkata, he has seen customers making large-value payments using POS machine or Paytm. However, Deepak himself has never used any digital payments channel for payments. He was not aware that digital channels can be used for small-value payments as well. He feels that using digital channels to make or accept payments is a complex process.

What makes him a receptive reticent?

What makes him a receptive reticent?

The receptive reticent, despite being interested, does not use digital modes of making payments owing to their low levels of literacy or understanding. They are highly dependent on others for handholding and support to comprehend, trust, and use the digital payment modes. They display an accommodative attitude when the customer demands to pay digitally.

The receptive reticents like Deepak accept the payment through a digitally-enabled merchant nearby and later settles it in cash with that merchant. This category of merchants needs to conduct multiple digital payments transactions under a reliable person’s guidance before they can work on their own. In India, urban cultures have been influencing rural areas at an increasing pace. In such a scenario, people like Deepak feels that the day is not too far when people in villages will embrace cashless payments.

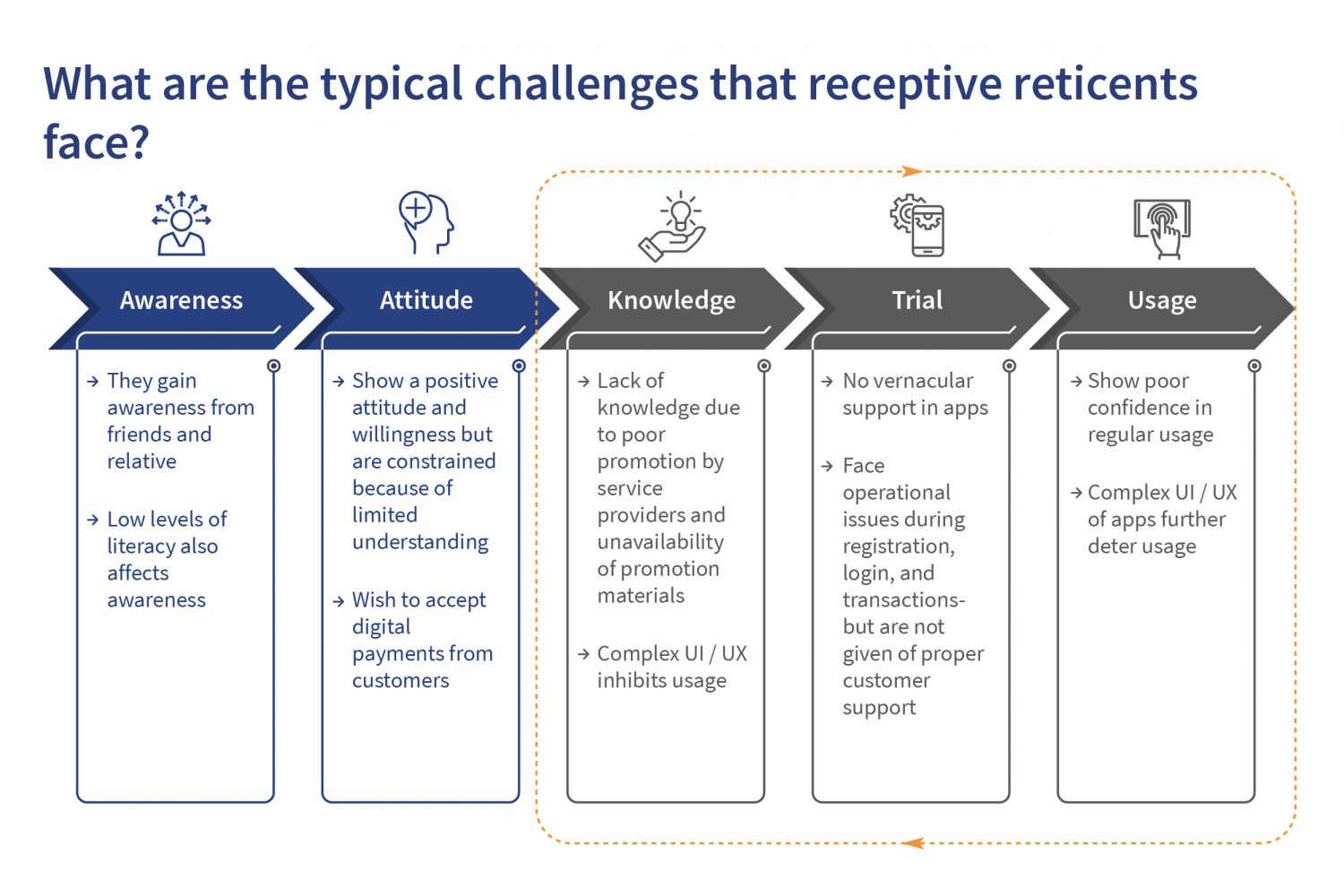

What are the typical challenges that receptive reticent face?

Receptive reticents start taking an interest in digital payments because people around them are interested in them (Behavioural trait: social proofing).However, due to information asymmetry, they do not have complete information on digital payment products and hence, are not able to graduate to the “usage” stage. This merchant category is most comfortable in the local language. The primary source of information for these merchants is word-of-mouth. This makes these merchants susceptible to biased information—which may or may not be correct and depends heavily on others’ experiences. Therefore, they can be dissuaded from adopting digital payments easily. Moreover, such receptive reticents are constrained by the multiple modalities and requirements of using different digital products. These present too much information, which is beyond their limited cognitive abilities. The diagram below illustrates some of the other challenges that this category of merchants faces.

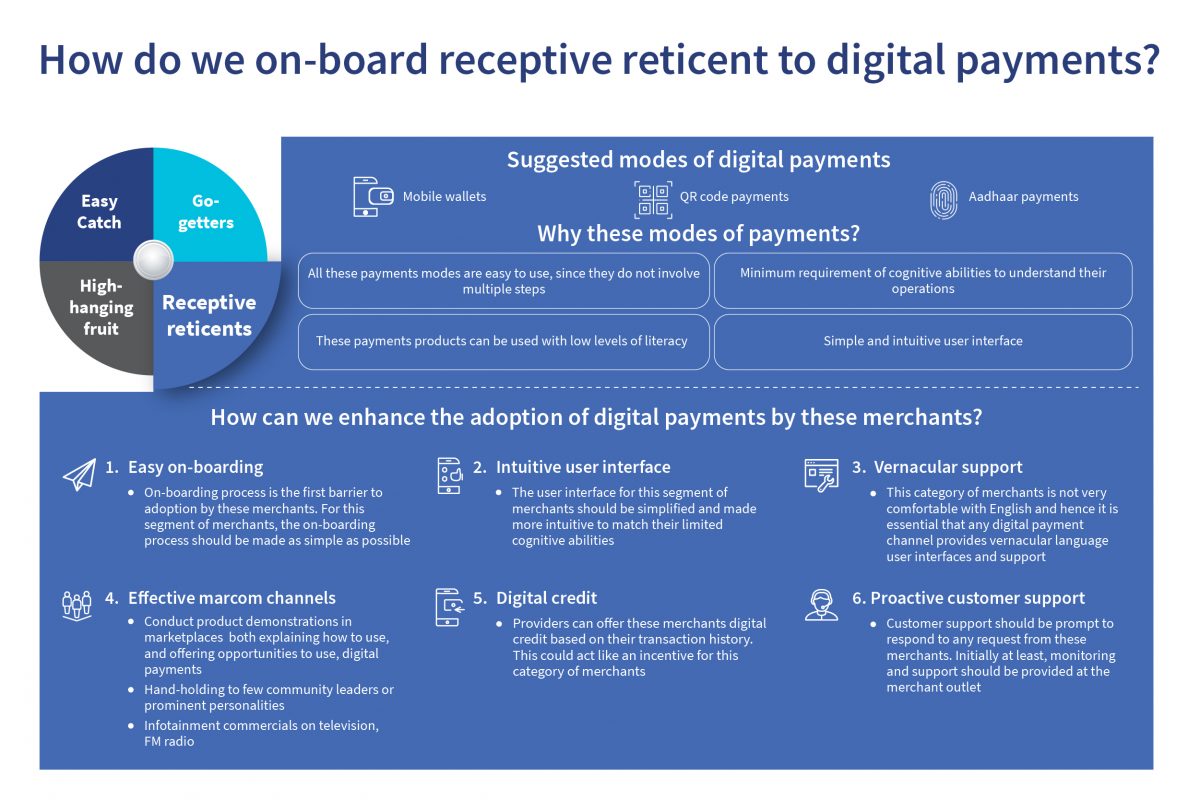

How do we on-board receptive reticent to digital payments?

Receptive reticents need hassle-free digital payments products both for the on-boarding process and to complete transactions successfully. They also need proactive support from providers (probably physical visits to merchant outlets) to train and resolve issues. The UI of the digital payment product should suit their limited cognitive abilities.

Written by

Sunil Bhat

Partner

Amit Joshi

Senior Analyst

Kritika Shukla

Project Manager, RBIH

Leave comments