We developed Mi4iD—our proprietary, multidisciplinary thinking process. Mi4iD blends behavioral science, rigorous research, and human-centered design, through which we solve complex challenges in social and economic development.

We use Mi4iD to keep empathy at the core of our research as we uncover why people do what they do, build solutions that drive change, and test them in the real world. Our teams cocreate with clients to prototype user-centric products and services that are desirable, feasible, and scalable.

The UN Capital Development Fund (UNCDF) commissioned this study by MSC under the 10X Program. In partnership with the Mastercard Foundation, the UNCDF implements the program with Outbox Uganda, Women in Technology Uganda (WITU), and Refactory Academy. The assessment examines digitalization of MSMEs and device financing in Uganda, with a focus on youth and women entrepreneurs, including refugees and persons with disabilities. It highlights key challenges, such as affordability, digital literacy, and access to financing. The study provides actionable recommendations to enhance digital adoption, strengthen access to finance, and support sustainable growth in Uganda’s MSME sector.

The Ministry of National Development Planning (BAPPENAS) has officially launched a national report titled “Accelerating the Blue Economy in Indonesia” on August 6, 2025 in Jakarta. It is part of a larger strategy to enhance food security and promote sustainable development. The report is set against the context of a global crisis and the escalating impacts of climate change. Several partners, which include MSC (MicroSave Consulting), have contributed to the Blue Food Assessment through qualitative field research.

MSC participated in the launch event held in Jakarta as a technical partner. During the event, MSC emphasized the need to understand the conditions and priorities of small scale fisheries and aquaculture (SSFA). The SSFA community has long sustained the backbone of Indonesia’s aquatic food sector, but remains significantly under-supported.

“Gender dynamics play a pivotal role in how communities access natural resources,” said Grace Retnowati, Executive Director of MSC Southeast Asia. “When women’s contributions are overlooked, their ability to claim rights and benefit from resources is diminished. Add to that the territorial tensions between large and small-scale fishers, and we see how equity and sustainability must go hand in hand.”

The report adopted a qualitative approach and examined the four key provinces of East Java, East Nusa Tenggara, South Sulawesi, and Maluku. This approach engaged with more than 140 community stakeholders, local governments, and the private sector. Although SSFA actors account for 85% of the national fisheries sector, they still face many challenges. These include limited access to finance, inadequate post-harvest technology, high food loss rates, and constant pressure from climate change and environmental degradation.

The Ministry of National Development Planning (Bappenas), Rachmat Pambudy emphasized the strategic role of fisheries in national development. “Fish is our most efficient source of protein, rich in omega-3 and essential for nutrition,” he said. “It has long supported the livelihoods of coastal communities. As we pursue the Vision of Indonesia Emas 2045, the ocean must be safeguarded as a vital source of life and prosperity.”

He noted that Blue Food development will be prioritized over the next five years, in line with Asta Cita and Indonesia’s identity as the world’s largest archipelagic nation.

The report outlines a set of concrete recommendations. These include how to integrate aquatic foods into social protection schemes and promote nutrition literacy through behavior change communication. It also highlights how to apply eco-friendly technology innovations and expand social protection for small-scale fishers and aquaculture farmers.

The blue economy can potentially increase marine sector’s contribution to GDP by up to 15% by 2045. This events marks how the government is committed to place the blue economy as a cornerstone of Indonesia’s long-term development.

Every morning, Ibu Rohana prepares her signature nasi uduk for a loyal community of customers. Even though she walks on a prosthetic leg due to her mobility impairment, she has built a successful nasi uduk business with the support of collateral-free loans and peer group networks. Her success results from the support of Koperasi Mitra Dhuafa (KOMIDA), one of Indonesia’s largest microfinance institutions. Rohana’s success story shows how financial services can do more than offer access, they can shift power and enable real economic agency for women with disabilities.

Anchored in the UN Convention on the Rights of Persons with Disabilities (UNCRPD), the rights-based model of disability recognises that access to financial services is not a matter of charity. It is a fundamental human right. This model obligates financial institutions and regulators to move beyond goodwill to fulfil their legal duties as duty-bearers responsible for ensuring the full and equal economic participation of persons with disabilities. This framing is particularly relevant when we examine financial inclusion in Asia, where persons with disabilities, and women in particular, remain largely invisible within formal financial systems. Their exclusion goes beyond limited access; it reflects deeper structural barriers that deny them control over economic resources, decision-making power, and opportunities for enterprise leadership. For financial inclusion to be truly transformative, it must be understood not simply as expanding access, but as a mechanism for redistributing power.

As per WHO estimates, around 690 million people in Asia and the Pacific, or nearly one in six, live with disabilities, where financial exclusion remains widespread. Fewer than 20% of PWDs in low‑ and middle‑income countries, including across the Asia‑Pacific, have access to formal financial services. In countries, such as Thailand and Indonesia, people with disabilities face poverty rates 5–6% higher than the national average. Amid such challenges, financial services could play a key role in improving economic security. However, women with disabilities experience added exclusion shaped by gender discrimination, caregiving responsibilities, limited income opportunities, and persistent social stigma. In the case of rapidly digitalizing economies like Indonesia, financial products and platforms are rarely designed to address these intersecting barriers.

Even when Indonesia had significantly expanded financial access, visible gaps persist. Only 24.3% of persons with disabilities over the age of 15 have a bank account, compared to 47% of those without disabilities. Only 1.1% access digital financial services (DFS), far below the national average of 8.1%. The gender gap is sharper still. Only 42.1% of women with disabilities use DFS, compared to 60 % of men with disabilities. Such data reflects more than inequality. They reveal a financial system that was never designed with PWDs at its core.

Even when OJK issued Regulation No. 76/POJK.07/2016 that mandated PwD accessibility in financial services, its implementation has remained limited. Most financial service providers (FSPs) have focused on physical access, such as installation of ramps or wheelchair-friendly ATMs. Yet more profound and systemic constraints are overlooked. These include inaccessible digital platforms, limited staff capacity, and rigid onboarding procedures that create friction for users with disabilities.

MSC’s field experience highlights how inclusive financial services can be transformative when financial services move from transaction to transformation, from access to agency. Our recent research examined barriers and opportunities for improving financial access for women with disabilities. The findings underscored how responsive product design can facilitate meaningful financial participation. Rohana’s success is a perfect example from our field experience. At 45, she finances her children’s education, renovates her home, and manages a small shop.

Her inspiring story proves financial tools can be designed to uphold rights, not merely compensate for needs through accessible and relevant services. Achieving this requires confronting the full intersectionality of exclusion. When financial services consider the needs of PWD, it can open the gates to opportunities and build resilience for a group long overlooked by the formal financial sector. But Rohana’s success remains the exception. Making such inclusion the norm requires a shift from reactive accommodations to systemic, rights-based design.

Most financial institutions, including MFIs, still lack active engagement with women with disabilities as a target segment. High healthcare and personal assistance costs are hardly covered by insurance, which adds to the financial pressure. Only 14.2% of PWDs in Indonesia have accessed formal credit. Women with disabilities get excluded based on perceived risk, unstable income, or a lack of collateral. These criteria disproportionately give a disadvantage to those who are already on the margins.

At such a juncture, women with disabilities, faced with limited alternatives, often turn to informal sources such as digital loans, “buy now, pay later” services, or community-based credit. These may offer temporary ease of access but face risk. Most DFS platforms are inaccessible and lack features, such as screen-reader compatibility, audio navigation, or simplified e-KYC processes. This leads to a misunderstanding of terms and conditions, which results in over-indebtedness or exploitation by predatory lenders.

This marks the digital divide in action, and it continues to widen for women with disabilities in the financial sector.

If we are to achieve institutional transformation toward a disability-inclusive financial system, Indonesia will need more than improvements in physical infrastructure. It demands products, platforms, and services that are designed to mirror the diverse lived experiences of users. Universal design principles must integrate across digital interfaces, credit products, and customer support systems. For example, individuals with visual impairments may require voice-guided interfaces or in-person assistance, while those with hearing impairments benefit from captioned content or sign language interpretation. Financial services cannot follow a one-size-fits-all model if they intend to serve everyone equitably.

Crucially, true inclusion also demands co-design, not just consultation. In line with Article 4(3) of the UNCRPD, financial service providers must meaningfully engage with organisations of persons with disabilities (OPDs) as partners in design, testing, and implementation of financial products. Inclusion must begin with listening to the people and be supported by reliable data. Regulators can play a key role by requiring the collection and reporting of disability-disaggregated data through ESG or social performance frameworks. Without data, financial exclusion will remain invisible and unaddressed.

Indonesia has made vital strides in its attempts to broaden access to financial services, but women with disabilities remain at the margins. If stakeholders are bridging this gap, they will need more than inclusive slogans. Regulators, FSPs, and policymakers must take intentional, institutionalised action.

Visibility is only the first step. Women with disabilities must be seen not as fringe beneficiaries, but as full participants in the financial system. Yet true inclusion goes beyond visibility as it requires a shift in power, voice, and agency within financial systems. Too often, women with disabilities are dismissed as unprofitable or high-risk. Yet their lived experience, resilience, and entrepreneurial capacity tell a different story. One of the potential, not pity.

Financial systems are more than mechanisms of transaction. They are instruments of agency, dignity, and independence. If Indonesia and the wider region are serious about inclusive finance, they must demonstrate what rights-based, power-shifting financial inclusion looks like. Not symbolic access, but structural transformation. Not passive service uptake, but active economic leadership. Women like Ibu Rohana reflect the possibilities that emerge when financial systems are built not just for those at the intersections of gender, disability, and economic exclusion, but with them.

This article was first published on Magdalene.co platform on August 1st, 2025

This report shines a spotlight on sneaky interface tricks that quietly push users- especially those with limited income- into costly decisions they didn’t intend to make. By exposing five common manipulative design tactics like guilt-tripping and hiding fees, the report calls for ethical design and collaboration among regulators, providers, and policymakers. The goal? Creating digital financial services that users genuinely trust and feel confident using, making finance fairer and more inclusive for all.

On the dark monsoon night of 16th August 2018, several rivers in Kerala burst through embankments and reservoir gates, sending vast amounts of muddy water churning into low-lying villages. By dawn, at least 445 people were dead, nearly a million forced from their homes, and entire communities lay submerged under a churning, brown sea.

Critically, no sirens or SMS alerts warned residents of the rising waters. Although India had 275 flood-forecasting stations, none covered the specific rivers that flooded—a gap previously identified by experts. Post-flood reviews concluded that an end-to-end early warning system (EWS) could have provided the necessary warning for evacuation and mitigated this disaster.

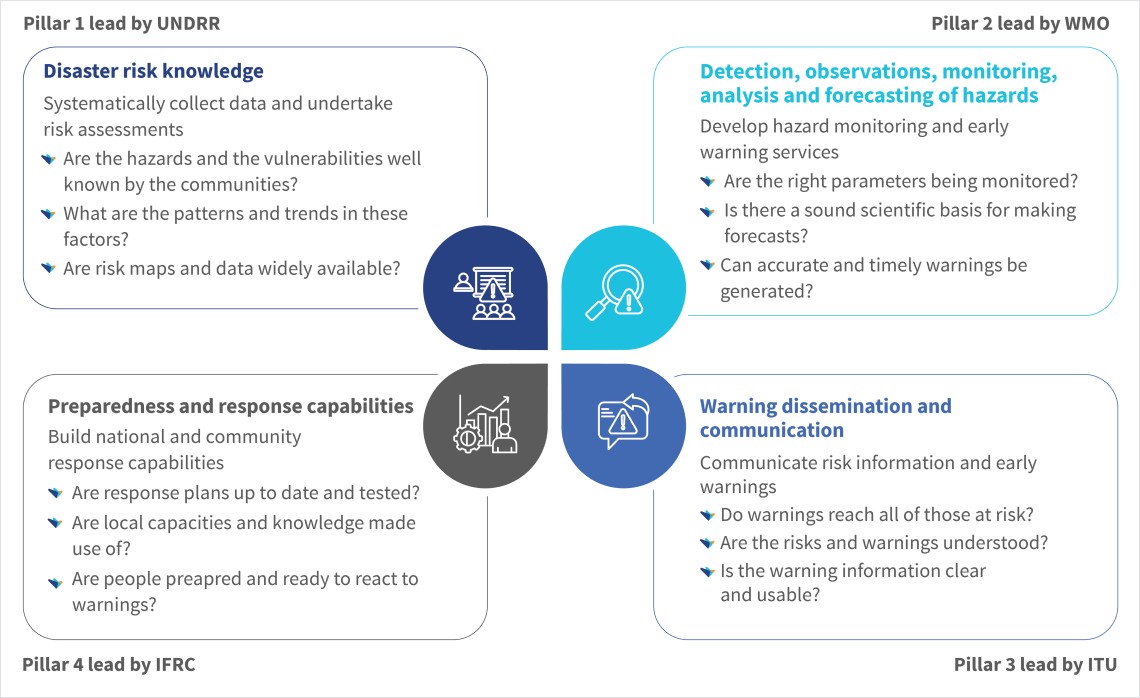

The tragedy in Kerala tragedy highlights a global truth: Climate change has intensified extreme weather events, while their frequency has surged fivefold over the past 50 years. This has made EWS more critical than ever. These systems convert forecasts into clear, actionable alerts to give authorities and the public vital time to prepare and act.

The World Meteorological Organization (WMO) defines EWS as a coordinated framework that transforms hazard information into effective action through four interconnected pillars:

Studies show that effective EWS can achieve substantial results. It can avert USD 3 to 16 billion in annual economic losses, reduce disaster fatalities by eight times, and cut economic damages by 30% with just a 24-hour notice. Yet, half the world’s countries lack an adequate EWS. This leaves a third of the global population unprotected.

To combat this, the United Nations launched the Early Warnings for All initiative to achieve near-universal EWS coverage by 2027. Yet, the success of these systems hinges on careful design, strategic deployment, and operational efficiency. In this context, the , partnered with MSC to undertake a case study on India’s recently established public warning system, SACHET. It can serve as a valuable model for other countries that seek to enhance their public alerting capabilities.

India’s alerting challenges

Historically, warnings relied on slow channels, such as radio, TV, and newspapers. In India, these challenges were compounded by outdated SMS lists that missed travelers and migrant workers. Alerts often went to entire districts, creating alert fatigue, and were rarely in local languages. Furthermore, multiple agencies sent uncoordinated alerts manually, meaning citizens received too little warning, too late.

Today, mobile networks reach more than 95% of the global population, which makes phones vital to modern early warning systems. Countries have started to adopt location-based SMS and cell broadcast to send geofenced alerts in seconds. Following this trend, India too saw a need for a unified, mobile-first system to replace its legacy channels.

The entry of SACHET

The National Disaster Management Authority (NDMA) and the Centre for Development of Telematics (C-DOT) developed SACHET (“to be alert” in Hindi) to meet India’s disaster alerting needs. Launched nationwide in August 2021, it serves as the country’s first unified digital platform for issuing disaster warnings, also known as a public warning system.

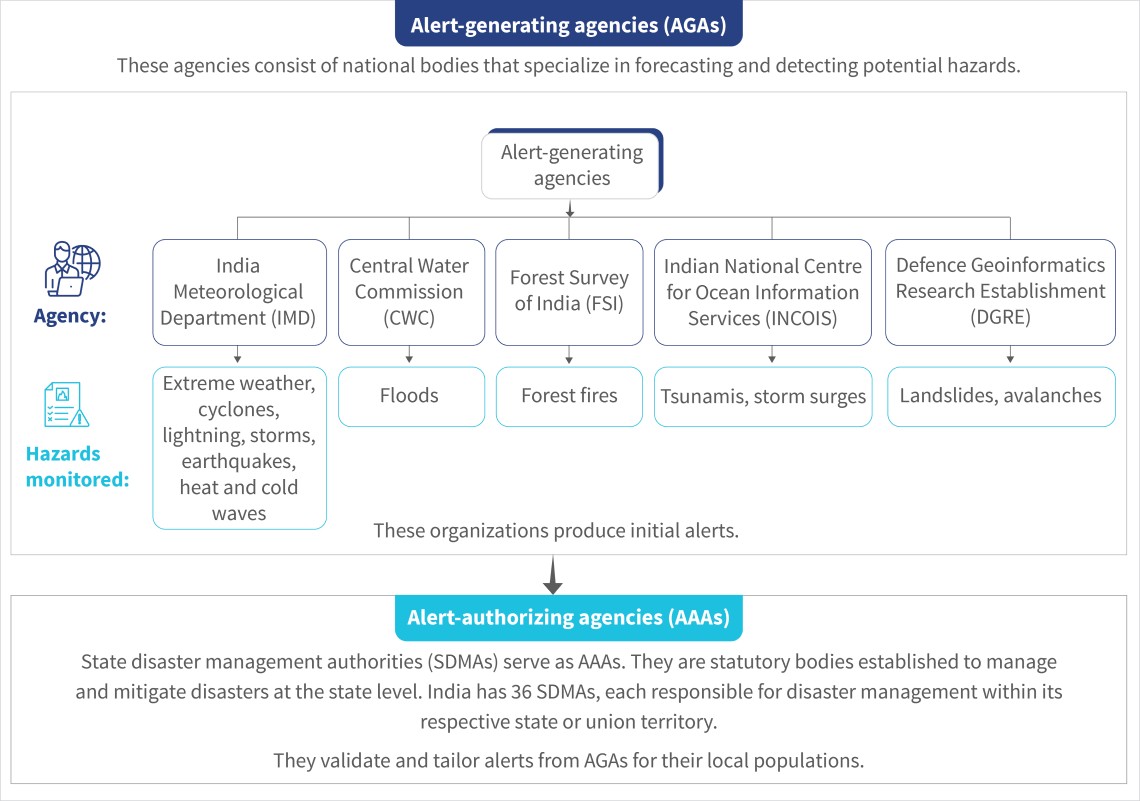

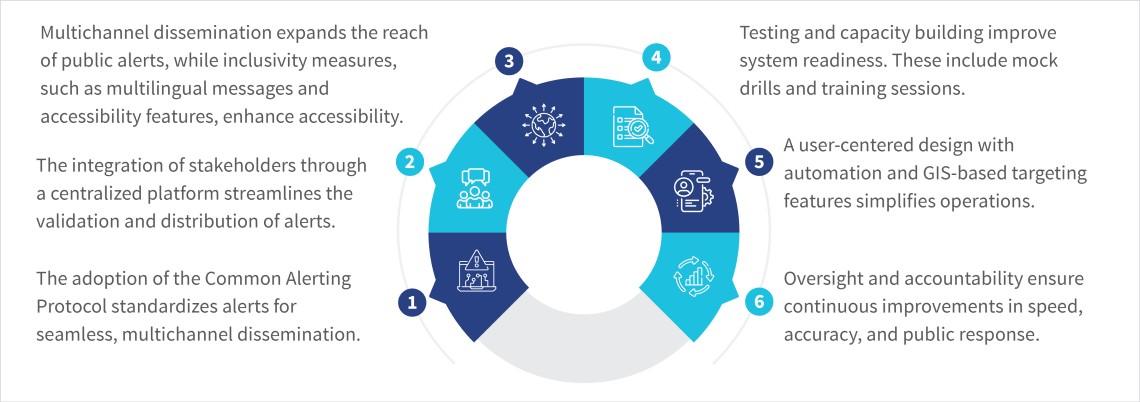

At its core, SACHET uses the Common Alerting Protocol (CAP)—an open, XML-based standard that gives every warning a consistent structure, so alerts from different agencies can be shared, understood, processed, and disseminated immediately. Crucially, SACHET brings together two key groups of stakeholders on one secure platform—alert-generating agencies (AGAs) and alert-authorizing agencies (AAAs). The following infographic describes how they work:

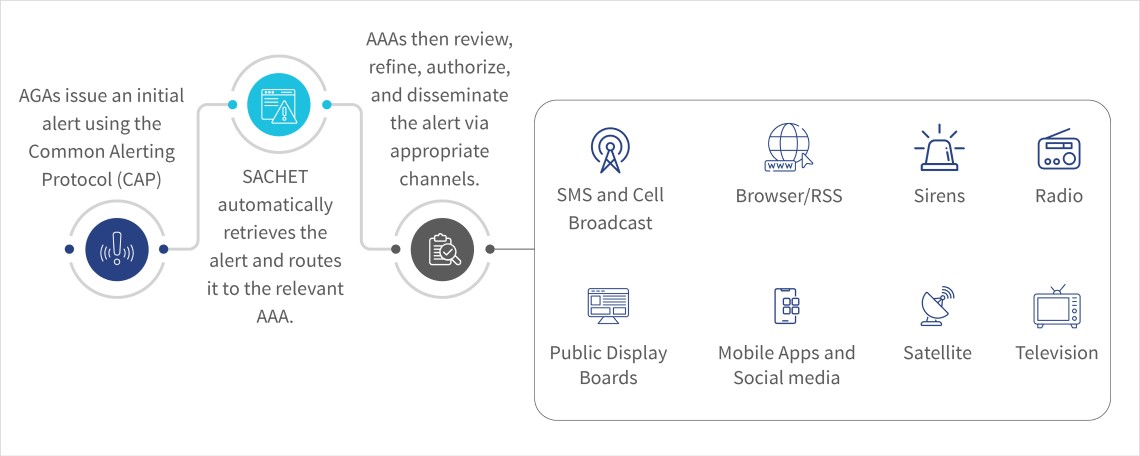

When an AGA triggers an alert, SACHET automatically routes it to the relevant SDMA or AAA. These officials then carefully review the message, translate it into local languages, and refine its content for clarity and effectiveness. They also use geographic information systems to define affected areas precisely by creating detailed “geofences” (see Figure 1 below). This meticulous approach ensures that warnings reach only those directly threatened and minimizes unnecessary panic and alert fatigue. The finalized warning is disseminated across all chosen media channels with a single click within a few minutes.

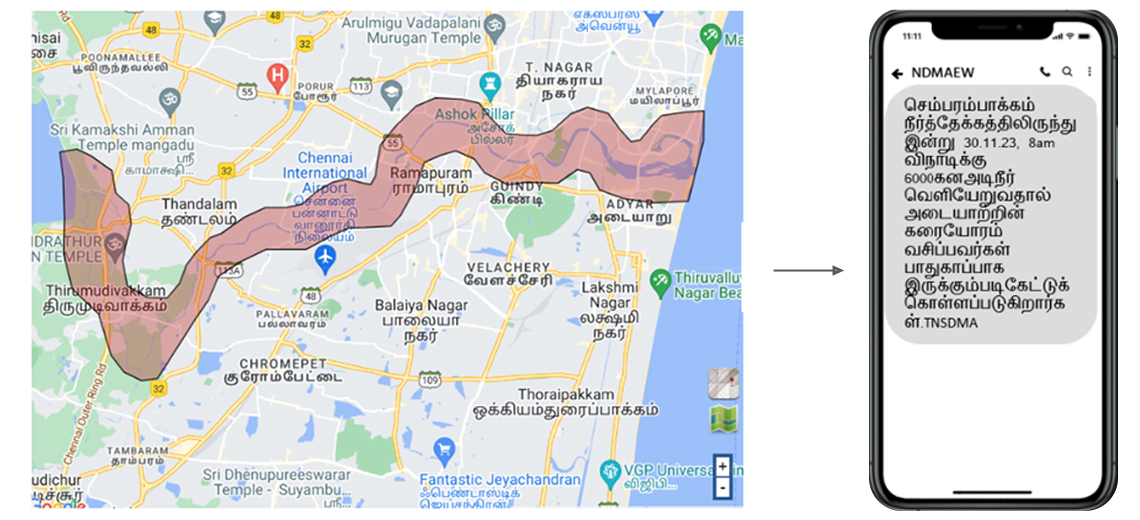

Figure 1: Example of a geotargeted flood alert SMS disseminated in the local language through SACHET

Mobile network operators form the backbone of SACHET. They enable the swift exchange of messages through India’s four largest operators: Airtel, Jio, Vodafone Idea, and BSNL. The system uses both location-based SMS (LB-SMS) and cell broadcast (CB) technologies to send quick, geotargeted messages to mobile phones. While they have different strengths and limitations, a system that intelligently combines both for the right context is most effective (See here for more on this).

Beyond mobile alerts, SACHET uses multiple communication channels, such as television crawls, radio broadcasts, railway station display boards, mobile apps, social media, browser RSS feeds, and satellite communication (See Figure 2 below). This comprehensive “many channels, one message” approach ensures universal coverage and guarantees that critical alerts reach everyone. It does not matter whether a person is online or offline, watching TV, or working in the fields. Some form of alert will reach them.

Figure 2: Overview of the alerting process and dissemination channels in SACHET

Since its launch, SACHET has issued more than 30,000 hazard-specific alerts through 44 billion LB-SMSs. Its streamlined workflows have helped deliver alerts in places without rapid channels and supported faster evacuations alongside more timely protective actions.

We have distilled six key considerations from our analysis of India’s SACHET public warning system to help countries design, deploy, and operate effective public warning platforms:

Beyond warnings: Triggering financial resilience

Timely alerts can save lives. However, they are not enough alone. Many vulnerable households struggle to take the necessary actions due to financial limitations. For example, a family cannot evacuate without money for transport, and a farmer cannot protect their livestock without cash in hand. True resilience means ensuring that people receive early warnings and have the financial means to respond effectively. Recent innovative financial mechanisms provide a means to bridge this critical gap:

1. Forecast-based financing (FbF): This refers to prearranged cash transfers that are automatically released when forecasts predict a hazard. It allows communities to prepare for the disaster, buy supplies, safeguard assets, or relocate before disaster hits.

2. Contingent lines of credit (CLOC): These refer to indexed loans that are made available to preapproved borrowers once disaster triggers, such as flood levels, are met. They offer fast relief without upfront costs.

3. Anticipatory loans: Similar to CLOCs, anticipatory loans are preapproved credit lines activated before a disaster, based on early warning forecasts. MSC will pilot this model with BURO Bangladesh and Atram.

Microfinance institutions are well-positioned to deliver these anticipatory loans at scale with their deep community networks and expanding digital capabilities. However, government support will be vital to make this ecosystem work. Governments can share accurate forecast data, offer partial credit guarantees to reduce lender risk, and enact favorable policies and regulations.

As climate threats intensify, countries must urgently modernize their EWS. SACHET provides a strong model for building an inclusive, tech-enabled public warning system. MSC seeks to pair these alerts with timely financial access, so vulnerable communities can act, adapt, and recover more quickly.